The global geopolitical and macroeconomic architecture has been fundamentally destabilized by the outbreak of the 2026 Iran War and the subsequent, highly effective closure of the Strait of Hormuz. Following the initiation of Operation Epic Fury by the United States and Operation Roaring Lion by Israel on February 28, 2026, the Islamic Republic of Iran suffered catastrophic degradation of its conventional military capabilities.1 The allied strike campaign systematically dismantled Iranian air defenses, targeted strategic command nodes, and eliminated an estimated 92 percent of the Islamic Revolutionary Guard Corps Navy (IRGCN) large blue-water vessels.1 Furthermore, the campaign successfully executed decapitation strikes against top echelon leadership, including Supreme Leader Ali Khamenei, Supreme National Security Council official Ali Larijani, and IRGCN Commander Alireza Tangsiri.1

Despite this overwhelming application of conventional force—which included the delivery of over 12,000 precision munitions against more than 15,000 targets across the Iranian homeland—Iran has successfully executed an Anti-Access/Area-Denial (A2/AD) strategy that has paralyzed the world’s most critical energy transit corridor.3 The resulting disruption has triggered the largest oil supply shock in global history, effectively trapping thousands of commercial vessels, sending Brent crude prices to historic peaks, and triggering a cascading crisis in global agricultural supply chains.1

This report provides an exhaustive, multi-domain analysis of the strategic paradox defining the 2026 conflict: how a severely degraded state actor retains the capacity to blockade a vital maritime chokepoint against the world’s premier naval powers. It further examines the weaponization of commercial maritime insurance, the establishment of the extortionary “Tehran Toll Booth” transit regime, the expansion of the conflict into the Bab al-Mandab strait, and evaluates five strategic scenarios available to the United States and its allies to restore freedom of navigation, ranked from the most likely to be effective to the least.

The Paradox of Power: Operation Epic Fury and the Illusion of Conventional Supremacy

The foundational premise that the destruction of Iran’s conventional military apparatus equates to the reopening of the Strait of Hormuz represents a fundamental miscalculation of Iranian asymmetric naval doctrine. Operation Epic Fury was designed with laser-focused objectives: to destroy Iranian offensive missiles, neutralize missile production facilities, and annihilate the Iranian Navy.7 While U.S. Central Command (CENTCOM) forces, utilizing B-2 stealth bombers, B-1 Lancers, and Tomahawk land-attack cruise missiles, successfully neutralized major naval facilities at Bandar Abbas, Chabahar, and Konarak, this conventional destruction did not translate into sea control.1

Iran’s ability to shut down the Strait of Hormuz indefinitely does not rest on capital ships, frigates, or symmetrical naval dominance. Instead, Tehran’s doctrine relies on a deliberate, decentralized, and highly survivable A2/AD posture.9 This strategy is explicitly designed to raise operational risks to commercial shipping to levels that civilian operators and marine insurance markets simply cannot tolerate, thereby forcing tanker rerouting and triggering global economic disruption.9

The United States Navy possesses unquestionable surface superiority, with a massive deployment of carrier strike groups, including the USS Abraham Lincoln and the USS Gerald R. Ford, operating in the region alongside an armada of AEGIS-equipped destroyers.10 However, established naval doctrine draws a sharp distinction between “sea denial”—the ability to destroy enemy vessels and prevent them from operating freely—and “sea control”—the ability to safeguard and guarantee continuous civilian transit through a highly contested zone.10 The U.S. military has successfully achieved total sea denial against the IRGCN’s conventional assets, but it remains structurally incapable of achieving sea control within the constricted, 21-mile-wide geography of the Strait of Hormuz.10

Iran’s ultimate strategic advantage in this theater relies on the ascendancy of “dumb mass” over “cutting-edge quality”.10 The IRGCN utilizes a low-cost, high-volume arsenal of coastal defense cruise missiles, unmanned aerial vehicles (UAVs), and fast-attack craft positioned along the jagged and mountainous Iranian littoral.9 Intercepting these asymmetric threats is economically and tactically unsustainable for advanced naval forces over a prolonged duration. The interceptor cells and anti-missile gun magazines aboard U.S. destroyers and allied frigates cost millions of dollars per engagement and deplete far more rapidly than Iran’s vast, dispersed stockpiles of expendable munitions.10 Consequently, the U.S. Navy can effectively win every tactical engagement against incoming Iranian fire while simultaneously losing the broader strategic campaign to keep the waterway open for unarmed merchant vessels.

The Architecture of Area Denial: Mines, Islands, and Electronic Warfare

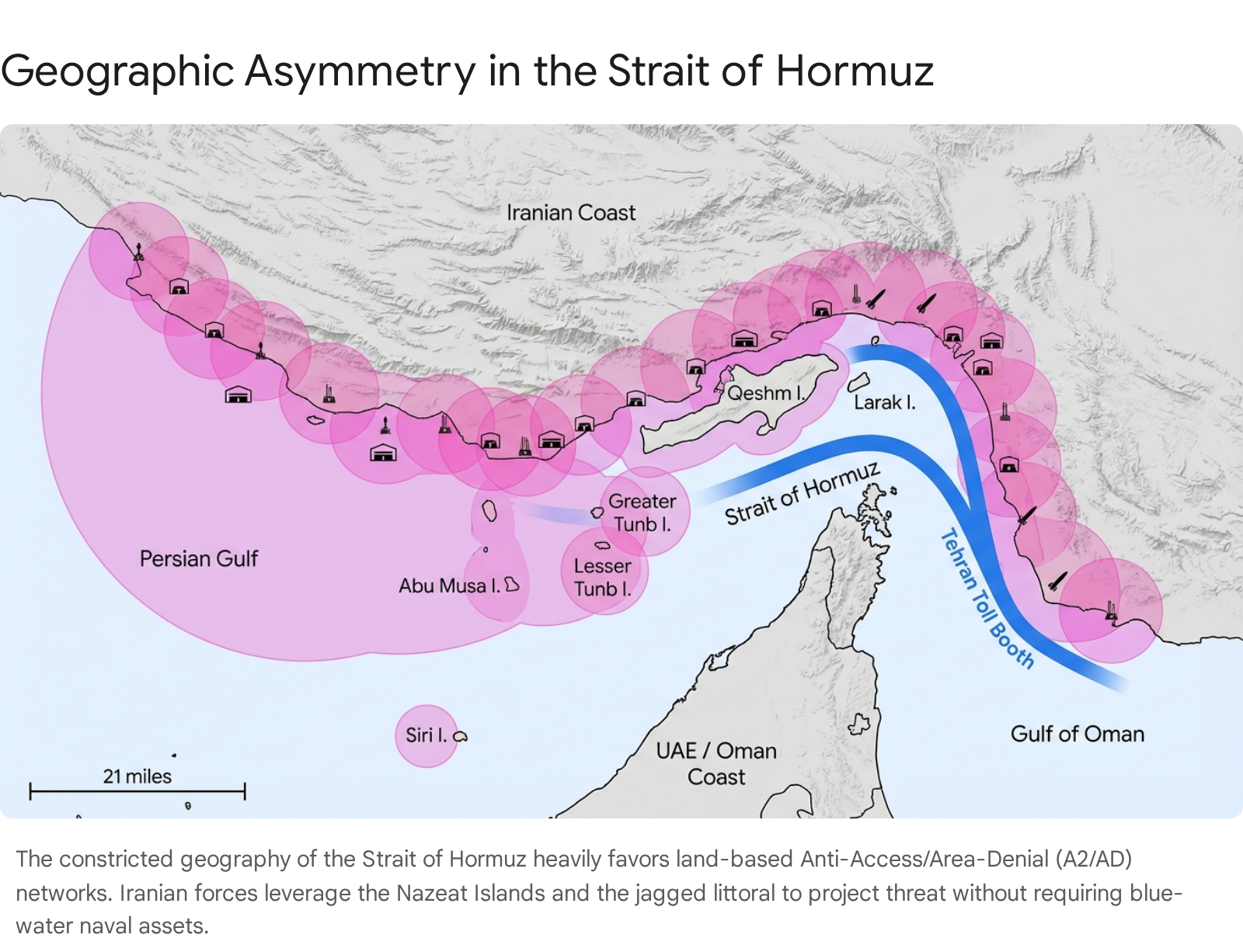

The physical mechanisms by which Iran enforces this blockade are deeply integrated into the geography of the Persian Gulf and the Gulf of Oman. The Strait of Hormuz is not merely a broad expanse of water; commercial shipping is canalized by draft restrictions and navigational safety requirements into a highly predictable transit pattern.12 This predictability allows Iran to optimize its A2/AD assets.

The Nazeat Islands: Forward Operating Fortresses

Iran has systematically fortified the Nazeat Islands—a strategic chain comprising Greater Tunb, Lesser Tunb, Abu Musa, and Siri—transforming them into unsinkable forward operating bases that project threat directly over the international shipping lanes.13 These islands host vital communications infrastructure, fuel depots, maintenance facilities, and aircraft hangars.13

More critically, the islands conceal a vast network of hardened underground bunkers utilized to store and launch anti-ship cruise missiles.13 Greater Tunb and Abu Musa also feature port facilities capable of sheltering and deploying fast-attack craft.13 While CENTCOM forces have utilized 5,000-pound GBU-72 penetrator munitions to strike subterranean targets along the coast and on these islands, the sheer volume of dispersed, fortified sites ensures that a lethal baseline threat remains highly resilient to aerial bombardment.1

Naval Mining and the Weaponization of Tides

Further complicating the maritime security environment is Iran’s deployment of advanced naval mines. The U.S. military has successfully engaged Iranian minelaying capabilities, with CENTCOM reporting the destruction of 44 dedicated minelaying vessels.13 However, the strategic reality of the Strait dictates that Iran does not strictly require specialized ships to lay mines. The notoriously strong tidal currents of the Strait of Hormuz allow Iranian forces to covertly float mines into the transit lanes from various obscured points along their extensive shoreline.10

Intelligence assessments confirm that Iran has deployed the Maham 3 and Maham 7 series naval mines into the waterway.13 The Maham 3 is a moored, buoyant, high-explosive anti-shipping mine capable of being set at depths of up to 100 meters.13 It utilizes sophisticated magnetic and acoustic sensors capable of detecting a ship’s presence from approximately three meters in any direction.13 The Maham 7 is a lightweight “bottom influence” mine that rests on the seafloor, designed to target medium-sized ships, landing craft, and small submarines.13 It can be rapidly deployed by small surface vessels or dropped via parachute from helicopters.13

The strategic impact of these weapons is wildly disproportionate to their numbers. Intelligence suggests that Iran has deployed only a highly limited number of mines—estimated at between fewer than ten to a dozen active units.13 Yet, the mere confirmed presence of unexploded ordnance in a confined maritime terrain instantly alters the risk calculus. Because mine clearance operations are slow, technically demanding, and leave specialized minesweeping vessels highly vulnerable to follow-on drone or missile attacks, even a token deployment of mines can keep the world’s most critical oil chokepoint closed indefinitely.9

“Smart Control” and Electronic Warfare

Iran’s physical A2/AD infrastructure is augmented by advanced electronic warfare (EW) and drone capabilities. Just prior to the outbreak of the war, in February 2026, the IRGCN conducted a large-scale exercise explicitly branded as “Smart Control of the Strait of Hormuz”.15 This drill showcased the integration of artificial-intelligence-based guidance systems for cruise missiles designed to counter electronic interference, alongside the deployment of roaming Shahed attack drones and the naval variant of the “Seyed-3” surface-to-air missile, which provides a regional air defense umbrella over IRGCN assets.16

The conflict has also seen a severe degradation of the electromagnetic spectrum. The proliferation of GPS spoofing and signal jamming in the region poses an extreme hazard to civilian navigation.18 Modern merchant vessels rely entirely on Global Navigation Satellite Systems (GNSS). When these signals are spoofed, large, slow-to-maneuver vessels can appear to be miles off course, increasing the catastrophic risk of collisions or groundings in the narrow channels of the Strait.18

The Commercial Paralysis: Safety, Insurance, and the “Tehran Toll Booth”

The physical threat posed by Iranian munitions represents only the kinetic dimension of the blockade. The ultimate enforcement mechanism of the Strait’s closure is commercial. Before the IRGCN actively began striking large numbers of tankers, the Strait had already been effectively closed by the structural logic of global maritime commerce, marine insurance, and institutional risk aversion.20

The Weaponization of Maritime Insurance

Within 48 hours of the initial U.S.-Israeli airstrikes on February 28, the marine insurance market reacted violently.20 War risk premiums surged from nominal peacetime levels to between 5 and 10 percent of a vessel’s total hull value.21 For a Very Large Crude Carrier (VLCC), a single transit could incur millions of dollars in additional premium costs alone. Consequently, major marine insurers issued 72-hour cancellation notices on existing war risk extensions, and the Lloyd’s Joint War Committee (JWC) redesignated the entire Arabian Gulf, Gulf of Oman, and adjacent corridors as active conflict zones.20

However, the narrative that the Strait is closed purely because insurance is unavailable is technically inaccurate. The Lloyd’s Market Association (LMA) issued formal statements clarifying that marine war insurance cover remains robustly available within the London market.23 A market survey indicated that 88 percent of main participants in the Lloyd’s marine war market retain the appetite to underwrite hull war risks, and over 90 percent will underwrite cargo.23 Furthermore, liability coverage through Protection and Indemnity (P&I) Clubs remains non-cancellable.23

The LMA firmly asserts that the primary driver halting commercial traffic is acute safety concerns held by shipowners and masters, not the lack of insurance capacity.23 Operators are making rational commercial decisions based on extreme operational hazards. The conflict has already exacted a heavy human and material toll; there have been at least 11 confirmed seafarer fatalities, tugboats have been sunk while attempting salvage operations, and dozens of merchant ships have been damaged or abandoned (including the MT Skylight, MKD Vyom, and the UAE-flagged Mussafah 2).1 Ships stranded in the region face depleting bunkers, while chemical tankers report running dangerously low on stabilizers required to prevent hazardous cargoes from degrading.23 Given the high probability of targeted strikes, shipowners are simply unwilling to risk total asset loss, catastrophic environmental pollution, and crew fatalities, regardless of whether an underwriter is willing to write a policy.

The Extortionary “Tehran Toll Booth” Regime

In the vacuum created by the withdrawal of standard commercial shipping, Iran has implemented a highly formalized, extortionary transit system recognized by maritime intelligence agencies as the “Tehran Toll Booth”.24 This system forces vessels to abandon standard international traffic separation schemes and navigate exclusively through a tightly controlled corridor within Iranian territorial waters, specifically passing between Qeshm and Larak Islands.24

The operational mechanics of this system are rigorous, demonstrating Iran’s transition from mere disruption to managed exploitation. Vessel operators seeking passage must first contact approved intermediaries with direct connections to the IRGC.25 Operators are required to submit a comprehensive documentation package, which includes the ship’s IMO number, the full corporate ownership chain, the cargo manifest, the final destination, and a complete crew list.25 These intermediaries forward the intelligence to the IRGC Navy’s Hormozgan Provincial Command, which conducts “geopolitical vetting,” sanctions screening, and cargo alignment checks—currently prioritizing the export of oil over all other commodities.25

If a vessel passes this geopolitical screening, the IRGC issues a specific clearance code and strict route instructions. Upon approaching the corridor, the vessel is hailed over VHF radio for code verification, after which an IRGC pilot boat is dispatched to physically escort the ship through the Larak Island detour.25

In exchange for this “safe passage,” Iran extracts exorbitant sovereign fees. Intelligence confirms that vessels are being charged up to US$2 million per transit, with payments actively brokered by maritime service companies and settled covertly in Chinese yuan.6 Iranian parliamentarians are actively drafting legislation to permanently formalize these tolls as a new “sovereign regime” over the waterway.6

This system has effectively bifurcated the global shipping industry. Western operators are entirely excluded from the corridor, or actively refuse to participate due to the severe, multi-jurisdictional legal risks.25 The IRGC is designated as a Foreign Terrorist Organization (FTO) by the U.S. State Department. Under U.S. law, providing “material support”—including the payment of transit tolls—to a designated FTO carries massive civil, regulatory, and criminal liabilities.25 Consequently, no cargoes transiting under the toll system have been destined for the United States or European markets.6

Shadow Fleets, AIS Spoofing, and Sanctions Evasion

To exploit the toll corridor while attempting to mitigate international scrutiny, a complex ecosystem of sanctions evasion and identity spoofing has accelerated. A shadow fleet of “zombie tankers” has emerged, utilizing sophisticated AIS spoofing to impersonate decommissioned or scrapped vessels.24 For example, a vessel assumed the digital identity of the Japan-flagged LNG carrier LNG Jamal (which was recycled in Alang, India in late 2025) to exit the Middle East Gulf via the Larak detour.24 Another vessel impersonated the aframax Nabiin (broken up in Chittagong in 2021), utilizing its IMO number while transmitting a Mozambique flag and the false name Nature Heart.24

While Western fleets remain paralyzed, China-affiliated vessels and Indian bulk carriers have actively utilized the detour, heavily backed by state-level diplomatic intervention.24 A Chinese-owned feeder containership, the Newvoyager, became the first confirmed vessel with mainland Chinese ownership to pay for passage through the corridor, utilizing a Chinese maritime services company as a payment intermediary.24 To signal compliance to Iranian coastal forces, vessels have begun broadcasting their strategic alignment directly into their AIS transmissions, with the Newvoyager broadcasting “DUQM ALL CREW CHINA” during its transit.24

India has also leveraged intense diplomatic backchannels to secure the release of its critical energy supplies. This diplomatic effort was operationalized by the Indian Navy under the banner of Operation Urja Suraksha.27 Deploying more than five frontline warships, including advanced destroyers and frigates, the Indian Navy successfully guided high-priority, India-bound vessels carrying liquefied petroleum gas (LPG)—including the Jag Vasant, Pine Gas, Shivalik, and Nanda Devi, alongside the crude tanker Jag Laadki—out of the danger zone.27 While highly successful for India, this operation underscores that transit is currently reliant on bilateral appeasement of Tehran rather than the enforcement of international maritime law.

Global Macroeconomic Contagion: The Collapse of the Commodity Supply Chain

The strategic implications of the Strait of Hormuz closure extend far beyond regional security; the blockade has precipitated a systemic shock to the global macroeconomic order. Traffic through the corridor—which normally accommodates upwards of 150 vessels per day—collapsed by over 97 percent following the outbreak of hostilities, with only 116 total transits recorded between March 1 and March 25.6

The primary casualty has been the global energy market. The Strait is the conduit for approximately 20 million barrels of oil per day (representing 20 percent of global consumption) and 20 percent of the world’s liquefied natural gas (LNG) trade.1 The sudden removal of this capacity triggered historic volatility.

The economic devastation, however, is not limited to hydrocarbons. The crisis has triggered a massive contagion effect across global agricultural and industrial supply chains, threatening food security and industrial production in highly vulnerable, import-dependent nations.

The Agricultural Crisis: Fertilizers and Food Security

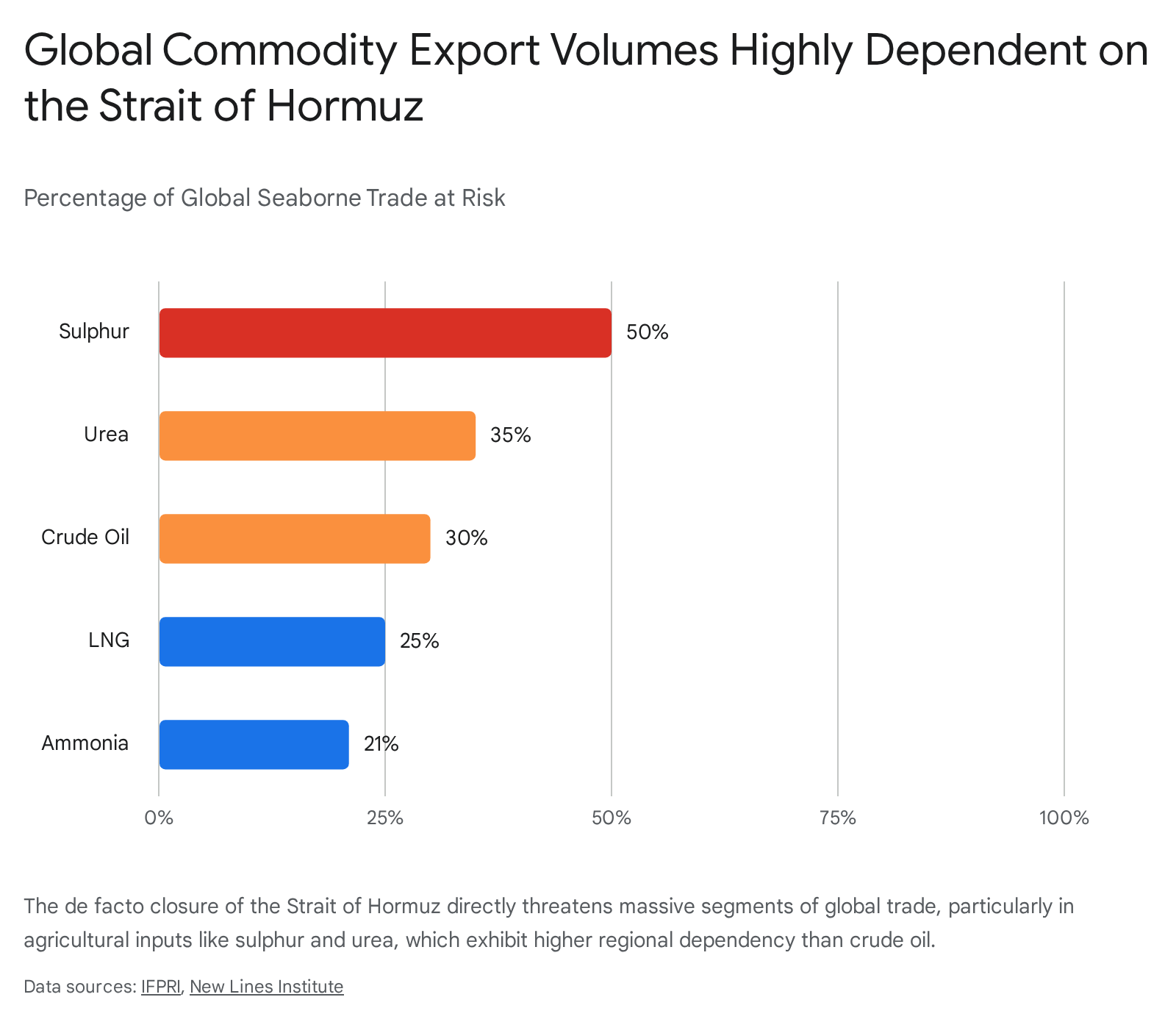

The Persian Gulf region is a structural pillar of the global agricultural sector, accounting for nearly 50 percent of the global sulfur trade (a critical input for phosphate fertilizers) and roughly one-third of all seaborne fertilizer exports.6 The sudden blockage of these materials has generated an immediate crisis for the spring planting season in the Northern Hemisphere.

The economic metrics clearly illustrate the severity of the supply shock:

| Economic Indicator | Pre-Conflict Baseline (Early Feb 2026) | Peak Crisis Level (March 2026) | Percentage Change / Impact |

| Daily Strait Transits | ~150 vessels/day | Near zero (~4-5/day) | >97% Collapse in Volume |

| Brent Crude Oil Price | ~$70 – $81 USD/barrel | $126 USD/barrel | ~55% – 80% Increase |

| Urea Fertilizer (May Contract) | ~$405 USD/metric ton | $681 USD/metric ton | 68% Increase |

| Corn-to-Urea Purchasing Power | 125 bushels for 1 ton of Urea (2022 levels) | 145 bushels for 1 ton of Urea | Severe margin compression for growers |

The downstream effects of this fertilizer shock are profound. The United States Department of Agriculture (USDA) projects that soaring input costs will push corn planting expenses to US150 per acre for American growers.6 Compounding the price issue is absolute physical scarcity; approximately 25 percent of American growers were unable to secure fertilizer deliveries for spring planting, a situation the U.S. Secretary of Agriculture has escalated to a “national security issue”.6

Globally, the Food and Agriculture Organization (FAO) projects that fertilizer costs could average 15 to 20 percent higher throughout the first half of 2026.6 The UN World Food Programme has issued dire warnings that tens of millions of people in vulnerable, import-dependent nations will face acute hunger if the supply chains remain severed through June.30

Industrial Supply Chains: Aluminum, Helium, and Plastics

The blockade has also severed the flow of critical industrial commodities. The Middle East supplies between 10 and 20 percent of the polyethylene and polypropylene utilized in food packaging and medical supplies across Europe and Asia.6 Furthermore, nations like Turkey—which alone imports up to US2 billion in plastic raw materials, and a fifth of its helium from the Gulf states annually—are facing severe industrial rationing.29 The disruption to helium is particularly threatening to the global semiconductor manufacturing industry, which relies heavily on Qatari exports.1 The Kiel Institute for the World Economy projects that prolonged disruption will result in severe welfare losses (up to 5.49 percent) and potential deindustrialization in highly exposed economies.6

Expanded Theater: The Bab al-Mandab and the Houthi Wildcard

Compounding the strategic nightmare in the Strait of Hormuz is the horizontal escalation of the conflict into the Red Sea corridor. As of March 28, 2026, the Yemen-based Houthi movement—a core constituent of Iran’s Axis of Resistance—officially joined the war, launching their first direct ballistic missile and drone attacks against southern Israeli military sites and the city of Tel Aviv.31

The Houthi entry into the conflict poses an extreme threat to the Bab al-Mandab Strait. With the Strait of Hormuz effectively closed, global shipping companies and Gulf energy exporters (particularly Saudi Arabia) had increasingly diverted their oil shipments via the East-West pipeline to Red Sea ports like Yanbu to bypass the Iranian blockade.33 The Houthis have now threatened to impose a secondary naval blockade on the Red Sea, specifically targeting vessels belonging to “aggressor countries”.34

This creates a scenario where vessels are trapped between two hostile chokepoints. If the Houthis successfully degrade traffic through the Bab al-Mandab—a route that ordinarily handles US$1 trillion worth of goods annually—the logistical rerouting around the Cape of Good Hope will further inflate global freight rates, stretch supply lines, and compound the macroeconomic damage already inflicted by the Hormuz closure.32 The presence of Houthi missiles also immensely complicates the deployment of U.S. naval assets, forcing Carrier Strike Groups to operate under continuous threat of asymmetric attack from multiple vectors.

Strategic Countermeasures: Five Scenarios for the U.S. and Allies

Faced with a degraded but deeply entrenched Iranian A2/AD network, the paralyzing weaponization of commercial insurance, and the threat of a two-front chokepoint war, the United States and its allies must evaluate pathways to restore global maritime trade. The following five strategic scenarios are ranked from the most likely to be effective and sustainable, to the least.

1. Diplomatic Corridors and Overland Pipeline Bypasses (Most Effective)

What would be done:

This scenario abandons the immediate, high-risk military objective of forcing the Strait open via naval confrontation. Instead, it focuses on structurally bypassing the chokepoint through infrastructure maximization while establishing UN-mediated diplomatic trade corridors.

Economically, this strategy requires maximizing the throughput of existing pipeline infrastructure to circumvent Hormuz entirely. This includes the Saudi East-West Crude Oil Pipeline (Petroline), which can move up to 7 million barrels per day to the Red Sea port of Yanbu, and the UAE’s Abu Dhabi Crude Oil Pipeline (ADCOP), which can transport 1.5 million barrels per day directly to Fujairah on the Gulf of Oman.36 Furthermore, the Kirkuk-Ceyhan pipeline in Iraq offers an alternative route to the Mediterranean.38

Simultaneously, the international community relies on the newly established United Nations Task Force, led by UN Under-Secretary-General Jorge Moreira da Silva.39 Utilizing representatives from the UN Conference on Trade and Development (UNCTAD), the International Maritime Organization (IMO), and the International Chamber of Commerce (ICC), this task force aims to operationalize a diplomatic mechanism to guarantee the safe, non-politicized movement of humanitarian goods and fertilizers.39 This mechanism draws direct inspiration from the successful Black Sea Grain Initiative and the UN Verification, Inspection and Monitoring Mechanism for Yemen (UNVIM).39

The Results: While overland pipelines cannot entirely replace the 20 million barrels per day normally transiting the Strait, maximizing the 10–15 million bpd capacity of combined bypass routes significantly blunts the global energy shock and stabilizes baseline supply.36 More importantly, the UN diplomatic mechanism provides a face-saving, internationally legitimate off-ramp for Iran. By allowing agricultural and humanitarian commodities to flow under UN monitoring, it bypasses the extortionary “Tehran Toll Booth” and prevents the IRGC from enriching itself via illicit transit fees.25 It effectively de-weaponizes the Strait without requiring kinetic escalation.

Further Investigation:

Highly recommended. The U.S. and allied partners should immediately fund urgent capital investment feasibility studies to rapidly expand the pumping capacity of the ADCOP and East-West pipelines. Furthermore, intensive diplomatic support must be thrown behind the UN Task Force, with Secretary-General envoy Jean Arnault leading negotiations to finalize the legal and operational framework required to prevent the impending global agricultural famine.

2. Multinational Stand-Off “Overwatch” Operations

What would be done: Led by the United Kingdom and France, a broad coalition of up to 35 nations forms an “overwatch” maritime security mission, independent of U.S. command structures.40 Unlike direct escort operations, this coalition strictly avoids entering the highly constricted, mine-threatened, and missile-locked waters of the Middle East Gulf.

Instead, naval assets—coordinated by French Armed Forces Chief Fabien Mandon and UK Chief of the Defense Staff Sir Richard Knighton—remain stationed in the Gulf of Oman and the Arabian Sea.40 Utilizing advanced radar, autonomous minehunting drones, and long-range interceptors, the coalition provides a defensive umbrella over the approaches to the Strait.24

The Results: This scenario creates a sanitized staging area and protects merchant vessels immediately before and after their transit through the highest-risk zone. It successfully demonstrates international resolve and secures the outer maritime perimeter without presenting highly vulnerable, concentrated naval targets to IRGCN coastal batteries and drone swarms.41 However, the French Defense Ministry has explicitly stated that the mission’s purpose is to organize the resumption of shipping once hostilities have ceased.41 Therefore, while it mitigates threats on the periphery, it relies heavily on a prior de-escalation of the U.S.-Israel-Iran conflict and does not solve the core, immediate issue of vessels having to run the gauntlet of the 21-mile-wide chokepoint unescorted today.

Further Investigation:

Moderately recommended. The diplomatic consensus-building is highly valuable, and deploying autonomous minehunting systems from stand-off ranges reduces human risk while addressing the psychological fear of unlocated bottom mines. However, policymakers must recognize it is a preparatory half-measure that does not fundamentally break the immediate A2/AD bubble over the Strait itself.

3. State-Backed Reinsurance and Targeted Naval Escorts

What would be done: This scenario attempts to address the commercial paralysis directly through sovereign financial intervention combined with hard military force. The U.S. International Development Finance Corporation (DFC), acting as a sovereign backstop and partnering with lead underwriter Chubb, provides a massive US$20 billion maritime reinsurance facility for qualified vessels.43 Because private insurers view the risk of a VLCC loss as catastrophically uninsurable without state backing, the U.S. government absorbs the extreme financial risk to lower war risk premiums to acceptable levels.43

To mitigate the physical threats that would trigger these massive insurance payouts, vessels utilizing this DFC insurance are escorted in heavily defended convoys by the U.S. Navy and allied forces.43 This operates under a doctrine similar to the 1980s Operation Earnest Will during the Tanker War, where U.S. warships physically shielded reflagged Kuwaiti tankers.45

The Results: Financially, the DFC’s $20 billion reinsurance program successfully provides the necessary market confidence for shipowners to legally operate, directly circumventing the IRGC’s extortion ring.43 However, the military component is highly problematic. Internal U.S. Navy assessments have concluded that widespread, routine escort operations in the current threat environment are “too dangerous”.47 The risk of drone swarms, remote-controlled explosive boats, and unlocated bottom mines overwhelming a destroyer’s defenses in such narrow waters is unacceptably high.47 The interceptor math remains highly unfavorable; emptying a multi-million-dollar VLS magazine to defend a commercial tanker against cheap Shahed drones is a losing attritional strategy.10 Therefore, while a massive U.S. escort program guarantees transit, it actively invites direct, high-casualty engagements with Iranian asymmetric forces.

Further Investigation: Recommended, but with extreme operational caution. The DFC’s reinsurance program is a necessary economic tool to combat the weaponization of insurance. However, U.S. lawmakers, including Senator Jeanne Shaheen, have rightly raised concerns about exposing U.S. taxpayers to massive liabilities, particularly if the escorted oil ultimately benefits strategic competitors like China.48 The rules of engagement and the sheer volume of required naval assets for continuous escorting must be strictly evaluated by CENTCOM to avoid catastrophic loss of a major surface combatant.

4. Comprehensive Cyber and Electronic Warfare (EW) Suppression

What would be done: The United States and Israel escalate non-kinetic, multi-domain operations to completely blind and disorient the IRGC’s targeting complex. This involves the mass deployment of GPS spoofing, widespread radar jamming, and offensive cyberattacks targeting command nodes such as the IRGC Navy 2nd Nouh-e Nabi Region Headquarters in Bushehr, as well as the communications infrastructure deeply buried on the Nazeat Islands.13 The objective is to sever the command-and-control links between Iranian coastal batteries, drone operators, and their targets, rendering their anti-ship cruise missiles useless.

The Results: Disrupting the electromagnetic spectrum temporarily degrades Iran’s ability to coordinate sophisticated, multi-vector swarm attacks or utilize AI-guided munitions. However, the secondary effects are severe. The maritime environment in the region is already suffering from heavy GNSS interference. Blanketing the Strait in intense electronic warfare makes civilian navigation exponentially more dangerous. As seen with the grounding of the MSC Antonia in the Red Sea due to GPS spoofing, removing reliable navigational data causes large, slow-to-maneuver vessels to appear miles off course, radically increasing the risk of collisions or groundings in the narrow, shallow channels of the Strait.18 More critically, EW does absolutely nothing to neutralize the Maham 3 and Maham 7 acoustic and magnetic naval mines already deployed in the water, which operate independently of RF command links.13

Further Investigation:

Warrants investigation as a strictly supplemental, highly targeted tactical tool, but it cannot serve as a primary strategic solution. While blinding Iranian radar is tactically sound prior to a specific transit, indiscriminately increasing electronic interference in a narrow waterway makes civilian navigation hazardous, ironically increasing the exact safety concerns that are keeping insurers and shipowners away from the region.

5. Littoral Occupation and Escalation to Total War (Least Effective)

What would be done: Based on the unyielding premise that naval power alone cannot secure a narrow strait against a hostile shore, the U.S. military commits to a massive amphibious and airborne ground invasion to physically occupy the Iranian littoral. This would require securing over 150 kilometers of mountainous, heavily fortified coastline, stretching from Qeshm Island past Bandar Abbas to Jask.10 U.S. Marines and the 82nd Airborne Division would be tasked with physically dismantling the subterranean coastal defense cruise missile (CDCM) sites, bunker complexes, and artillery positions yard by yard.10

The Results: This represents the “Ghost of Gallipoli” scenario realized.10 It would result in a catastrophic strategic overextension for the United States. Occupying the Iranian coastline offers no defensible depth; U.S. forces would be pinned against the sea, subjected to continuous, attritional guerrilla warfare and ballistic missile strikes from interior Iranian lines.10

Furthermore, such a massive escalation would trigger total regional destabilization. It would invite direct intervention or massive logistical resupply of Iranian forces by the Russian Federation via the Caspian Sea—a supply line the U.S. cannot interdict without initiating a direct conflict with Russian forces.10 The operation would result in unacceptable U.S. casualties, likely fracture the NATO alliance, and ensure the permanent destruction of the region’s energy infrastructure. The political, economic, and human costs would vastly outweigh the benefits of reopening the Strait.

Further Investigation:

Should not be investigated under any circumstances. It represents a fundamental failure of strategic cost-benefit analysis and ignores the painful historical lessons of asymmetrical warfare in constricted littoral environments against highly motivated, ideologically entrenched defenders.

Conclusion

The 2026 Strait of Hormuz crisis vividly demonstrates that in constricted maritime geography, asymmetric area-denial capabilities inherently outmatch conventional naval power projection. The joint U.S.-Israeli Operation Epic Fury succeeded brilliantly in devastating Iran’s conventional military infrastructure, decapitating its leadership, and sinking its blue-water fleet, but it fundamentally failed to secure the maritime commons. By leveraging low-cost mines, impenetrable coastal geography, and the structural, risk-averse nature of global marine insurance, Iran has successfully weaponized the global supply chain. It has held agricultural and energy markets hostage through its extortionary “Tehran Toll Booth” regime, effectively achieving strategic paralysis without requiring a traditional navy.

Because kinetic naval solutions are either deemed “too dangerous” by internal U.S. Navy assessments or invite catastrophic, Gallipoli-style escalation, the path forward must creatively circumvent the tactical deadlock. The United States and its international partners must prioritize structural bypasses—maximizing overland pipeline capacities—while simultaneously throwing full diplomatic weight behind the UN Task Force’s mechanisms to secure the movement of vital agricultural commodities. Breaking the blockade will ultimately not be achieved by sinking more Iranian fast attack craft, but by rendering the Strait of Hormuz strategically and economically irrelevant through diversified infrastructure and robust, state-backed financial countermeasures.

Please share the link on Facebook, Forums, with colleagues, etc. Your support is much appreciated and if you have any feedback, please email us in**@*********ps.com. If you’d like to request a report or order a reprint, please click here for the corresponding page to open in new tab.

Sources Used

- 2026 Strait of Hormuz crisis – Wikipedia, accessed March 28, 2026, https://en.wikipedia.org/wiki/2026_Strait_of_Hormuz_crisis

- Operation Epic Fury Situation Report | Battlefield Effects and Early Strategic Signals, accessed March 28, 2026, https://www.hudson.org/missile-defense/operation-epic-fury-situation-report-battlefield-effects-strategic-outcomes-can-kasapoglu

- Interim Assessment: Evaluating the Strategic Damage Caused to Iran in Operation “Roaring Lion” (Week 3 – March 21), accessed March 28, 2026, https://israel-alma.org/interim-assessment-evaluating-the-strategic-damage-caused-to-iran-in-operation-roaring-lion-week-3-march-21/

- What They’re Saying About Operation Epic Fury—March 26, 2026 | UANI, accessed March 28, 2026, https://www.unitedagainstnucleariran.com/press-releases/what-theyre-saying-about-operation-epic-fury-march-26-2026

- Iran Update Special Report, March 17, 2026 – Institute for the Study of War, accessed March 28, 2026, https://understandingwar.org/research/middle-east/iran-update-special-report-march-17-2026/

- Tehran’s “toll booth” in Hormuz cuts Western buyers out of fertilizer …, accessed March 28, 2026, https://www.foodingredientsfirst.com/news/hormuz-toll-fertilizer-food-costs.html

- Operation Epic Fury | U.S. Department of War, accessed March 28, 2026, https://www.war.gov/Spotlights/Operation-Epic-Fury/

- Operation Epic Fury and the Collapse of Iran’s Layered Naval Defense, accessed March 28, 2026, https://gulfif.org/operation-epic-fury-and-the-collapse-of-irans-layered-naval-defense/

- Top Eight Iranian Weapons That Could Shut the Strait of Hormuz Indefinitely — Inside Tehran’s A2/AD Arsenal Threatening Global Oil Supply and Naval Power Balance – Defence Security Asia, accessed March 28, 2026, https://defencesecurityasia.com/en/iran-weapons-strait-of-hormuz-shutdown-a2ad-mines-missiles-irgc-navy-oil-supply-threat/

- Ghost of Gallipoli: US warships cannot control the Strait of Hormuz …, accessed March 28, 2026, https://www.aspistrategist.org.au/ghost-of-gallipoli-us-warships-cannot-control-the-strait-of-hormuz/

- Hormuz Flashpoint 2026: The Siege of the World’s Energy Jugular and the Rise of the Tri-Lateral Naval Bloc – https://debuglies.com, accessed March 28, 2026, https://debuglies.com/2026/02/18/hormuz-flashpoint-2026-the-siege-of-the-worlds-energy-jugular-and-the-rise-of-the-tri-lateral-naval-bloc/

- Iran does not need to close the Strait of Hormuz to disrupt it – Al Jazeera, accessed March 28, 2026, https://www.aljazeera.com/opinions/2026/3/20/iran-does-not-need-to-close-the-strait-of-hormuz-to-disrupt-it

- Iran Update Special Report, March 24, 2026 | ISW, accessed March 28, 2026, https://understandingwar.org/research/middle-east/iran-update-special-report-march-24-2026/

- Iran Update Morning Special Report, March 11, 2026 | ISW, accessed March 28, 2026, https://understandingwar.org/research/middle-east/iran-update-morning-special-report-march-11-2026/

- Iran’s Ultra-Professional Drill in the Strait of Hormuz – YouTube, accessed March 28, 2026, https://www.youtube.com/watch?v=bG6JbawPbjM

- Iranian Naval Drill in the Strait of Hormuz Showcases New Missile and Drone Capabilities -, accessed March 28, 2026, https://wanaen.com/iranian-naval-drill-in-the-strait-of-hormuz-showcases-new-missile-and-drone-capabilities/

- Iran Update, February 24, 2026 | ISW, accessed March 28, 2026, https://understandingwar.org/research/middle-east/iran-update-february-24-2026/

- When GPS Lies at Sea: How Electronic Warfare is Threatening Ships and Their Crews, accessed March 28, 2026, https://news.gatech.edu/news/2026/03/12/when-gps-lies-sea-how-electronic-warfare-threatening-ships-and-their-crews

- Maritime security update: Gulf Region / Strait of Hormuz and Red Sea – Skuld, accessed March 28, 2026, https://www.skuld.com/topics/port/port-news/asia/maritime-security-update-gulf-region–strait-of-hormuz-and-red-sea/

- The Insurance Weapon: How Commercial Risk Logic Became an Irregular Warfare Tool at Hormuz, accessed March 28, 2026, https://irregularwarfare.org/articles/insurance-weapon-irregular-warfare-hormuz/

- China Sails Through Hormuz as Iran Blocks the World – House of Saud, accessed March 28, 2026, https://houseofsaud.com/china-cosco-hormuz-blockade-iran-selective-shipping/

- Maritime Terms Explained: Iran War & Strait of Hormuz Crisis – Windward, accessed March 28, 2026, https://windward.ai/blog/maritime-terms-explained-iran-war/

- Safety concerns, not insurance availability, driving reduced vessel traffic in the Strait of Hormuz – Lloyd’s Market Association, accessed March 28, 2026, https://lmalloyds.com/safety-concerns-not-insurance-availability-driving-reduced-vessel-traffic-in-the-strait-of-hormuz/

- ‘Zombie’ tankers take Tehran Toll Booth route as more vessels make detour – Lloyd’s List, accessed March 28, 2026, https://www.lloydslist.com/LL1156694/Zombie-tankers-take-Tehran-Toll-Booth-route-as-more-vessels-make-detour

- Tehran’s ‘toll booth’ system is now controlling Hormuz traffic :: Lloyd’s …, accessed March 28, 2026, https://www.lloydslist.com/LL1156720/Tehrans-toll-booth-system-is-now-controlling-Hormuz-traffic

- Tehran’s ‘toll booth’ system is now controlling Hormuz traffic, accessed March 28, 2026, https://mykn.kuehne-nagel.com/news/article/tehrans-toll-booth-system-is-25-mar-2026

- Indian Navy launches op to secure energy vessels in Strait of Hormuz amid war, accessed March 28, 2026, https://www.indiatoday.in/india/story/middle-east-war-indian-navy-launches-op-urja-suraksha-to-secure-energy-vessels-in-strait-of-hormuz-2886733-2026-03-25

- Indian Navy Launches ‘Operation Urja Suraksha’ To Secure India-Bound Ships Passing Through Strait of Hormuz, accessed March 28, 2026, https://www.marineinsight.com/indian-navy-launches-operation-urja-suraksha-to-secure-india-bound-ships-passing-through-strait-of-hormuz/

- Deep Dive: Strait of Hormuz’s Closure Will Hit Every Economy, accessed March 28, 2026, https://inkstickmedia.com/deep-dive-strait-of-hormuzs-closure-will-hit-every-economy/

- UN moves to create mechanism to safeguard Hormuz trade in face of Iran war By Reuters, accessed March 28, 2026, https://m.investing.com/news/world-news/un-moves-to-create-mechanism-to-safeguard-hormuz-trade-in-face-of-iran-war-4585778?ampMode=1

- Iran-Israel war LIVE: Israel says it intercepted first incoming missile from Yemen as war in West Asia intensifies, accessed March 28, 2026, https://www.thehindu.com/news/international/iran-israel-us-war-west-asia-conflict-strait-of-hormuz-attacks-march-28-2026/article70795241.ece

- US-Israel-Iran War Live: Yemen’s Houthis join Iran war for first time, launch missiles at Israel, accessed March 28, 2026, https://www.indiatoday.in/world/story/us-israel-iran-war-live-updates-middle-east-crisis-conflict-strait-of-hormuz-2887660-2026-03-27

- The Yemeni Front of the War: The Houthi Wild Card – Gulf International Forum, accessed March 28, 2026, https://gulfif.org/the-yemeni-front-of-the-war-the-houthi-wild-card/

- Red Sea crisis – Wikipedia, accessed March 28, 2026, https://en.wikipedia.org/wiki/Red_Sea_crisis

- Yemen’s Houthis claim responsibility for missile attack on Israel, their first since war started, accessed March 28, 2026, https://apnews.com/article/iran-us-israel-trump-lebanon-march-27-2026-195444c54cbb7545d0a77f8ffbc0e4c0

- How to make the Strait of Hormuz irrelevant, accessed March 28, 2026, https://www.washingtonpost.com/opinions/2026/03/25/iran-hormuz-energy-pipeline-bypass/

- Strait of Hormuz – About – IEA, accessed March 28, 2026, https://www.iea.org/about/oil-security-and-emergency-response/strait-of-hormuz

- Hormuz crisis: Why Gulf’s energy export alternatives remain limited, accessed March 28, 2026, https://www.aa.com.tr/en/economy/hormuz-crisis-why-gulf-s-energy-export-alternatives-remain-limited/3877060

- Note to Correspondents: on the Strait of Hormuz | Secretary-General – the United Nations, accessed March 28, 2026, https://www.un.org/sg/en/content/sg/notes-correspondents/2026-03-27/note-correspondents-the-strait-of-hormuz

- UK to host talks on mission to reopen Hormuz: Official – Courthouse News Service, accessed March 28, 2026, https://courthousenews.com/uk-to-host-talks-on-mission-to-reopen-hormuz-official/

- France says it approached 35 countries over future Hormuz mission – KFGO, accessed March 28, 2026, https://kfgo.com/2026/03/26/france-says-it-approached-35-countries-over-future-hormuz-mission/

- Joint statement from the leaders of the United Kingdom, France, Germany, Italy, the Netherlands, Japan, Canada and others on the Strait of Hormuz: 19 March 2026 – GOV.UK, accessed March 28, 2026, https://www.gov.uk/government/news/joint-statement-from-the-leaders-of-the-united-kingdom-france-germany-italy-the-netherlands-and-japan-on-the-strait-of-hormuz-19-march-2026

- Trump Official Says Hormuz Ship Insurance Program to Launch …, accessed March 28, 2026, https://gcaptain.com/trump-official-says-hormuz-ship-insurance-program-to-launch-soon-as-tanker-traffic-struggles-to-recover/

- Chubb Outlines Structure of $20B Gulf Reinsurance Facility, Now Including Liability Cover, accessed March 28, 2026, https://www.insurancejournal.com/news/international/2026/03/23/863026.htm

- Operation Earnest Will – Wikipedia, accessed March 28, 2026, https://en.wikipedia.org/wiki/Operation_Earnest_Will

- The Hormuz Crisis: Why Controlling a Chokepoint is Harder Than Winning a War, accessed March 28, 2026, https://moderndiplomacy.eu/2026/03/28/the-hormuz-crisis-why-controlling-a-chokepoint-is-harder-than-winning-a-war/

- Behind Closed Doors, U.S. Navy Says Hormuz Escorts Are Too …, accessed March 28, 2026, https://gcaptain.com/behind-closed-doors-u-s-navy-says-hormuz-escorts-are-too-dangerous-for-now/

- US senator presses DFC on taxpayer risk in $20 billion maritime reinsurance proposal, accessed March 28, 2026, https://www.insurancebusinessmag.com/reinsurance/news/breaking-news/us-senator-presses-dfc-on-taxpayer-risk-in-20-billion-maritime-reinsurance-proposal-569928.aspx

- Iran’s Next Move: How to Counter Tehran’s Multidomain Punishment Campaign – CSIS, accessed March 28, 2026, https://www.csis.org/analysis/irans-next-move-how-counter-tehrans-multidomain-punishment-campaign

- US moves airborne troops, Marines as Iran rejects ceasefire, raising ground war potential, accessed March 28, 2026, https://www.wfmd.com/2026/03/25/us-moves-airborne-troops-marines-as-iran-rejects-ceasefire-raising-ground-war-potential/