Introduction: The Geoeconomic Paradigm Shift of 2026

The global economic architecture of 2026 represents a definitive and irreversible departure from the hyper-globalized, efficiency-optimized frameworks that characterized the post-Cold War era. The international system has transitioned into a highly fractured multipolar environment where bilateral trade and integrated supply chains are no longer viewed merely as neutral conduits for mutual prosperity, but rather as primary vectors for statecraft, coercion, and strategic preclusion.1 The weaponization of supply chains—specifically those underpinning critical minerals, rare earth elements, and advanced technological components—has emerged as the defining national security challenge of the decade. For the defense industrial bases of the United States, the European Union, and their aligned partners, the chaotic transition from “just-in-time” logistics to “just-in-case” structural resilience has triggered profound disruptions across both commercial and military manufacturing sectors.2

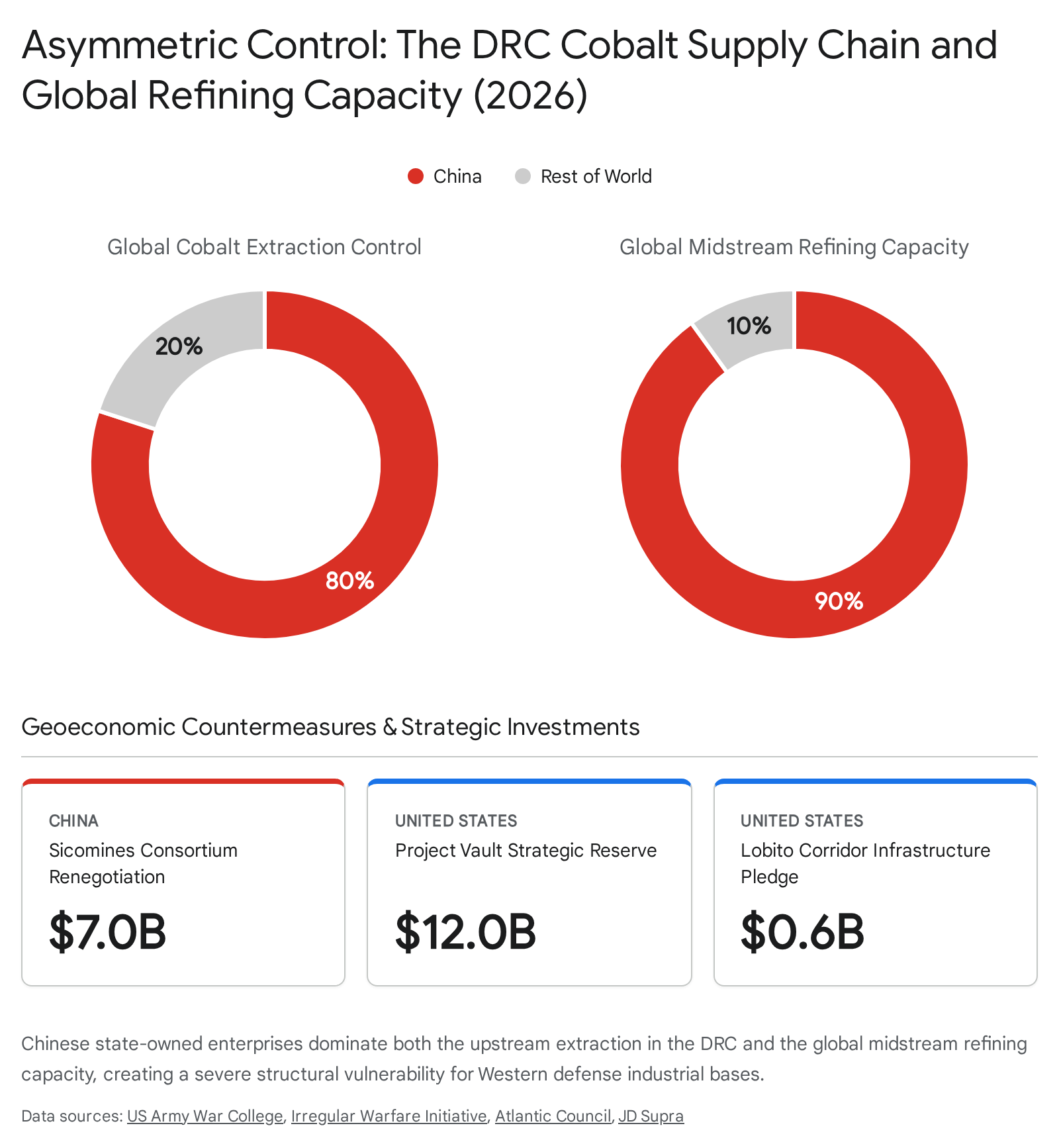

At the absolute center of this paradigm shift lies a fundamental misunderstanding long held by Western policymakers, often termed the “Mining Fallacy” by defense analysts.3 This fallacy posits the mistaken belief that resource security is strictly a function of possessing, accessing, or discovering geological reserves.3 It relies on the assumption that simply digging more holes in the ground guarantees a secure supply chain. In reality, the true center of gravity in modern economic warfare does not reside at the mine gate; it resides in the complex, highly toxic, and intensely capital-heavy midstream processing and refining sectors.3 The United States and its allies theoretically possess sufficient geological reserves of rare earth elements, cobalt, and copper to meet long-term demand.3 However, by systematically monopolizing between 85 percent and 90 percent of the world’s processing capacity for these critical materials, the People’s Republic of China (PRC) has engineered a systemic, end-to-end dependency that grants Beijing a functional “kill switch” over Western industrial capability.3

This comprehensive analysis dissects the mechanics and profound implications of supply chain weaponization in 2026. It meticulously examines foreign state control over the highly concentrated cobalt and copper sectors in the Democratic Republic of the Congo (DRC) and evaluates the strategic implications for the manufacturing of smart weapons, high-capacity batteries, and advanced aerospace components. The report further investigates the insidious nature of infrastructure capture through foreign control of South American energy grids, focusing specifically on the political and strategic crisis confronting Chile. Subsequently, the analysis details the sweeping architectural countermeasures implemented by the United States and the European Union—ranging from the physical infrastructure of the Lobito Corridor to the geoeconomic frameworks of Project Vault, the Forum on Resource Geostrategic Engagement (FORGE), and the Pax Silica alliance. Finally, the report quantifies the severe second-order effects of these geopolitical maneuvers on the production timelines and unit costs of advanced Western military hardware, offering a stark assessment of what defense economists now term the “price of resilience”.6

Section I: The Chokepoint in the Congo: Cobalt, Copper, and Strategic Monopolies

The Mechanics of Resource Capture in the Democratic Republic of the Congo

The Democratic Republic of the Congo (DRC) remains the undeniable global epicenter of the cobalt and copper trade, commanding an asymmetric influence over the raw materials required for the ongoing global energy transition and the modernization of advanced military forces. The DRC accounts for more than 70 to 80 percent of the world’s total cobalt output, alongside producing an estimated 3.3 million metric tons of copper annually.1 Cobalt is an indispensable element required for the production of high-capacity lithium-ion batteries, advanced munitions, and the high-temperature aerospace superalloys that form the backbone of modern military aviation.1 Over the past two decades, the PRC has systematically established a vice-like grip over the DRC’s mineral wealth, executing a patient, long-term strategy of infrastructure-for-resource deals that have fundamentally compromised the supply chain security of Western nations.1

As of 2026, Chinese state-owned enterprises (SOEs) and policy banks exercise control over roughly 80 percent of the DRC’s total cobalt output.1 The concentration of this control is staggering: of the ten largest cobalt mines globally—nine of which are located within the mineral-rich Katanga region of the DRC—five are under direct Chinese ownership and administration.1 This structural dominance was largely cemented by the original 2008 Sicomines agreement, a landmark $6 billion infrastructure-for-minerals exchange that successfully transferred ownership of 15 of the DRC’s 19 most lucrative cobalt and copper sites to Chinese entities.1

Over time, the asymmetric nature of this relationship generated intense political friction within the DRC. Congolese state auditors determined that the mining assets transferred to China had been vastly undervalued, while the promised infrastructure investments lagged significantly behind schedule, totaling less than $1 billion by 2023.1 Despite aggressive attempts by the government of President Félix Tshisekedi to renegotiate these terms to correct the severe imbalances—efforts that culminated in a revised agreement in early 2024 committing the Chinese-backed Sicomines consortium to $7 billion in infrastructure development—the fundamental ownership structure of the mining sites remained entirely unchanged.1 Chinese companies continue to administer the mines, extract the resources, and operate with highly favorable tax statuses, leaving the West heavily exposed.1

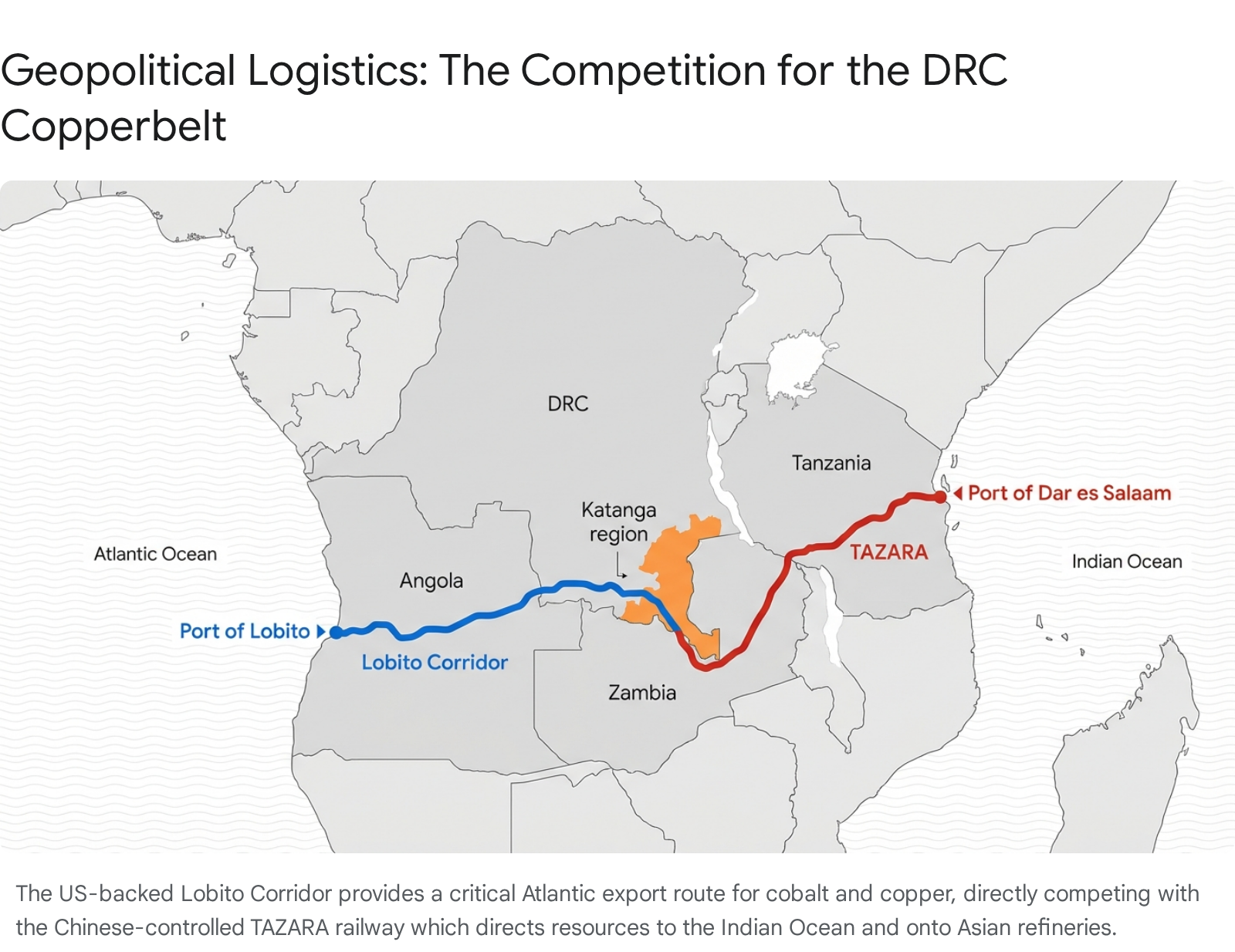

Crucially, China’s geoeconomic strategy in Central Africa extends far beyond the perimeter of the mine gate. By seamlessly linking upstream extraction to dedicated, state-financed logistics corridors, Beijing ensures the unbroken, highly efficient flow of critical minerals to its domestic refineries. The Chinese-backed modernization of the Tan-Zam (TAZARA) railway, fueled by a sweeping $1 billion investment program in exchange for operational control, facilitates the mass export of bulk minerals from the isolated Katanga region directly to the Tanzanian port of Dar es Salaam, effectively bypassing traditional, Western-accessible transport networks in southern Africa.1 Additionally, China has pursued a massive $10 billion project to modernize the Bagamoyo port in Tanzania, further securing its maritime logistics architecture.1 Consequently, an estimated 67.5 percent of China’s refined cobalt is sourced directly from the DRC, feeding a massive domestic refining apparatus that accounts for between 60 and 90 percent of global capacity.1

Evolving Diplomatic Frictions and the 2026 Shift

The strategic landscape surrounding DRC mineral rights began to shift significantly in late 2025 and early 2026, driven by a convergence of Congolese domestic politics and aggressive new U.S. foreign policy initiatives under the incoming Trump administration. Recognizing the geostrategic leverage inherent in his nation’s mineral wealth, President Tshisekedi adopted a strategy designed to play major powers against one another to maximize domestic returns.10 During the U.S. presidential transition period leading up to January 2025, Tshisekedi dispatched specialized emissaries to Washington to engage with the incoming administration, explicitly offering to assist the United States in its dual objectives of securing access to critical minerals and curtailing China’s expansionist footprint within the African supply chain.10

This diplomatic maneuvering rapidly yielded tangible results. By February 2025, with explicit encouragement from the U.S. House Foreign Affairs Committee, the Congolese government and the state mining company Gécamines took the unprecedented step of blocking a massive $1.4 billion takeover bid for Chemical of Africa (Chemaf).10 The rejected bidder was Norin Mining, a direct subsidiary of the massive Chinese state-owned weapons manufacturer Norinco.10 This rejection marked a watershed moment, signaling the DRC’s willingness to actively deny Chinese defense conglomerates further penetration into its most promising cobalt and copper projects when backed by U.S. diplomatic support.10

Strategic Implications for Advanced Defense Technology

The implications of this structural monopoly extend far beyond the commercial markets for consumer electronics and civilian electric vehicles; they strike directly at the core of Western defense readiness and technological superiority. In 2023, both the U.S. Department of Energy and the Department of Defense officially designated cobalt as a critical mineral, citing its indispensable applications across multiple spectrums of military technology.1

High-capacity, energy-dense batteries are increasingly vital for military logistics, the propulsion of unmanned ground and aerial vehicles, and the broad electrification of tactical platforms required for distributed operations.1 Furthermore, cobalt is a critical alloying element utilized to produce specialized superalloys. These superalloys possess extraordinary high-temperature strength, thermal stability, and unique magnetic properties, making them absolutely foundational to the manufacturing of aerospace components, including the hot sections of fighter jet engines, missile guidance systems, and advanced smart weapon actuation mechanisms.1

When a single adversarial state controls both the physical extraction of the raw material and the vast majority of its global processing capacity, it possesses the latent capability to enact targeted, devastating export controls that can paralyze the defense production lines of its strategic rivals. This is not a theoretical vulnerability; the weaponization of economic interdependence is actively deployed by Beijing through opaque environmental regulations, restrictive export licensing regimes, and state-directed production quotas that function as blunt instruments of geopolitical coercion.3 Without secure, Western-aligned access to refined cobalt and copper sourced from the DRC, the production and sustainment of next-generation Western defense platforms remains entirely subject to the strategic tolerance of the PRC.

| Strategic Mineral | Key Defense Applications | Structural Vulnerability in 2026 |

| Cobalt | High-temperature superalloys for jet engines, high-capacity tactical battery systems, smart weapon actuation. | 80% of DRC extraction controlled by China; up to 90% of global refining centralized in the PRC. |

| Copper | Advanced electrical infrastructure, radar/sensor arrays, defense microelectronics, data transmission. | Heavy reliance on DRC and Chilean output; refining capacity heavily concentrated in Asia. |

| Samarium & Gadolinium | Specialized rare earth magnets (Sm-Co) crucial for F-35 fighter jets, THAAD, and PAC-3 missile interceptors. | Near-total PRC monopoly; subject to active Chinese export licensing restrictions implemented in 2025. |

| Dysprosium & Terbium | Heat-resistant permanent magnets required for hypersonic glide vehicles and advanced propulsion. | Constrained global supply entirely dependent on Chinese heavy rare earth metallization facilities. |

Section II: Energy Infrastructure as a Sanctions Network: The Chilean Vector

The Subtle Architecture of Infrastructure Capture in South America

While the race for critical minerals heavily relies on the physical extraction and processing of resources in Africa, an equally potent and arguably more insidious form of supply chain weaponization is unfolding within the domain of critical public infrastructure. In South America, Chinese state-owned enterprises have systematically acquired controlling stakes in the energy generation, transmission, and distribution networks of key resource-rich nations, creating what defense analysts now characterize as a latent “physical sanctions network”.12

The scale and concentration of this infrastructure capture are profound. In Lima, Peru, a sprawling metropolis of 10 million people representing roughly one-third of the nation’s total population, electricity distribution is now 100 percent controlled by just two Chinese firms: China Southern Power Grid International (CSGI) and China Three Gorges Corporation.12 In Brazil, Chinese firms have poured billions of dollars into the sector, securing control over an estimated 12 percent of all national electricity transmission and distribution.12

However, the most strategically consequential penetration has occurred in Chile. Chile represents a critical node in the global energy transition, possessing vast reserves of lithium and serving as the world’s leading producer of copper.13 Despite this geoeconomic importance, Chinese companies currently control an estimated 66 percent of the country’s power distribution networks and approximately 55 percent of its electricity transmission infrastructure.12 This staggering degree of market concentration by foreign state-affiliated entities transcends conventional commercial investment; it represents a fundamental curtailment of host nation sovereignty and strategic autonomy.

The Threat to Strategic Autonomy and Industrial Reliability

Control over a nation’s energy grid dictates the operational reliability and output capacity of its entire industrial base. The vulnerability of this arrangement was vividly illustrated in February 2025, when widespread blackouts in Chile led to severe disruptions across the country’s crucial mining and industrial sectors.12 When the power grid fails, the extraction, processing, and export of the copper and lithium required by Western defense and commercial sectors grind to an immediate halt.

The strategic peril generated by this infrastructure capture is twofold. First, countries heavily dependent on foreign state-owned entities to illuminate their cities and power their economies are structurally disincentivized from aligning against those entities in broader geopolitical disputes.12 This dynamic severely curtails the options available to host governments regarding domestic industrial policy, foreign alignments, and participation in international trade consortiums. If the PRC were to weaponize this control, it could leverage the implicit threat of reduced grid efficiency, delayed maintenance, or intentional operational disruption to extract significant political concessions from Santiago or Lima.12

Second, the rapid modernization of these electrical grids introduces severe cybersecurity vulnerabilities. The widespread deployment of Chinese-supplied “smart meters”—such as the 600,000 units recently provided to neighboring Uruguay—creates entirely new vectors for cyber exploitation.12 Because these advanced meters monitor energy consumption in real-time and interface directly with national telecommunications networks, security researchers have demonstrated that they could be manipulated by hostile actors to simulate severe grid oscillations or initiate coordinated, cascading power shut-offs, effectively transforming civilian electrical infrastructure into a latent offensive military capability.12

The 2026 Chilean Political Crisis: Submarine Cables and the Kast Administration

This escalating geoeconomic tension culminated dramatically during the presidential transition to the Kast administration in Chile in early 2026. The transition of power—a historically stable bedrock of Chilean democracy since the end of the Pinochet dictatorship in 1990—was abruptly halted just days before the March 11 inauguration.16 Conservative President-elect José Antonio Kast publicly broke off transition talks with outgoing left-wing President Gabriel Boric over a highly controversial, last-minute infrastructure concession.16

The Boric government had abruptly granted a massive concession to a Chinese consortium comprising China Mobile International, China Unicom, and China Telecom to construct the “Chile-China Express” submarine fiber-optic cable.16 This project, which aimed to link the Chilean port of Valparaiso directly to Hong Kong across 20,000 kilometers of the Pacific Ocean, included manufacturing and deployment contracts awarded to HMN Tech, a firm formerly affiliated with Huawei.16

The United States explicitly identified this digital infrastructure project as a severe regional security threat, arguing that a direct Chinese cable would allow Beijing to route Latin American data traffic outside of North American visibility, deeply compromising the operational security of the hemisphere.17 In an unprecedented move against a close ally, the U.S. State Department invoked Section 212(a)(3)(C) of the Immigration and Nationality Act to impose strict visa restrictions on three Chilean government officials who had authorized the project, citing their actions as “undermining regional security”.17

President Kast, who won the election with 58.2 percent of the vote on a platform prioritizing strict security, immediate economic stabilization, and a decisive pivot toward alignment with the United States, faced a monumental challenge upon taking office on March 11, 2026.19 Kast merged the Mining and Economy ministries under single leadership to streamline investment and permitting, but he must now untangle Chile from these deep geoeconomic dependencies while maintaining the country’s status as a reliable Western supplier.14 The Kast administration’s ability to execute its economic agenda and attract U.S. capital will depend heavily on its capacity to mitigate the latent threats embedded within its own energy and digital networks.

| Sector | Chinese Ownership/Influence in South America | Strategic Vulnerability |

| Electricity Distribution (Chile) | ~66% controlled by PRC state-affiliated entities. | Direct exposure of copper/lithium mining operations to politically motivated grid disruptions. |

| Electricity Transmission (Chile) | ~55% controlled by PRC state-affiliated entities. | Curtailed sovereign ability to dictate industrial energy policy and green transition priorities. |

| Power Grid (Peru) | 100% of Lima distribution controlled by CSGI and Three Gorges. | Total capture of capital city infrastructure, creating a massive “physical sanctions” deterrent. |

| Telecommunications (Chile) | “Chile-China Express” submarine cable concession (HMN Tech/China Mobile). | Potential routing of sovereign Latin American data outside Western surveillance architectures; cyber espionage risk. |

Section III: The Architecture of Western Counter-Offensives: Alliances, Near-Shoring, and Industrial Policy

Recognizing the acute, cascading vulnerabilities exposed by the PRC’s dominance in the DRC’s mineral sectors and the insidious capture of South American energy grids, the United States and the European Union have aggressively accelerated a series of structural countermeasures in 2025 and 2026. These initiatives represent a comprehensive overhaul of Western industrial policy, designed to physically bypass adversarial supply chains, aggressively stimulate domestic and allied processing capacities, and enforce geopolitical loyalty through integrated financial and trade architectures.

Physical Bypasses and Trading Structures: The Lobito Corridor and Project Orion

To immediately neutralize China’s logistical advantage in Central Africa—specifically the flow of resources eastward via the TAZARA railway to the Indian Ocean—the United States and the European Union have heavily backed the physical development of the Lobito Corridor.1 This multi-billion-dollar infrastructure initiative aims to rehabilitate and drastically expand the colonial-era Benguela railway, creating a direct, Atlantic-facing export route that physically links the mineral-rich Katanga region of the DRC and the Zambian Copperbelt directly to the deep-water port of Lobito in Angola.22

The rail system encompasses 1,289 kilometers of track within Angola and a vital 450-kilometer extension into the DRC.24 Supported by a $600 million direct pledge from U.S. President Joe Biden and a subsequent $753 million financing package largely driven by a $553 million loan from the U.S. International Development Finance Corporation (DFC), the corridor became operational in August 2024.23 By early 2026, the Lobito Atlantic Railway consortium (comprising Mota-Engil, Trafigura, and Vecturis) had increased cargo throughput to over 60 percent of its capacity, achieving an 85 percent on-time delivery reliability metric.24 By bypassing traditional, congested southern African routes through Durban and countering Chinese-controlled eastern ports, the Lobito Corridor grants Western mining entities vastly enhanced supply chain flexibility and drastically reduced transit times to Atlantic markets.24

Complementing this physical infrastructure bypass is “Project Orion,” a sophisticated financial maneuver orchestrated by the United States. Utilizing the Orion Critical Mineral Consortium and leveraging deep partnerships with commodity trading giants like Glencore, the U.S. has secured its first major foothold in DRC copper and cobalt mines without assuming the severe sovereign and operational risks associated with direct state ownership of mining assets.9 Backed by an estimated $9 billion in aggregate frameworks and utilizing guaranteed, government-backed offtake agreements, this strategy structurally ensures that a substantial portion of the output from these specific mines will physically bypass Chinese refineries and flow directly into U.S.-aligned manufacturing networks.9

Geoeconomic Architecture: Project Vault, FORGE, and Pax Silica

The United States has rapidly moved beyond traditional diplomacy, deploying sweeping industrial policies aimed at market stabilization and strategic stockpiling. On February 2, 2026, the Trump administration officially launched Project Vault, a monumental $12 billion public-private partnership establishing the U.S. Strategic Critical Minerals Reserve.28 Backed by the largest single loan in the history of the Export-Import Bank of the United States (EXIM)—a massive $10 billion outlay—alongside $2 billion in expected private-sector capital, Project Vault represents a radically decentralized, demand-driven approach to stockpiling.28

Unlike centralized government purchasing programs, Project Vault allows original equipment manufacturers (OEMs) and defense contractors to submit lists of required minerals, committing to purchase them later at fixed prices.29 This structure covers all 60 minerals on the USGS Critical Minerals List, acting as a profound shield for domestic manufacturers against adversarial supply shocks and global price volatility.29 This is heavily augmented by the Department of Defense utilizing Defense Production Act (DPA) Title III authorities to fund domestic processing, such as a $15 million agreement with Jervois Mining for cobalt extraction in Idaho, and significant funding for REalloys to establish a “zero-China” heavy rare earth metallization facility in Ohio by 2027.1

Concurrently, the U.S. engineered the launch of FORGE (the Forum on Resource Geostrategic Engagement) at the inaugural 2026 Critical Minerals Ministerial.34 Chaired initially by the Republic of Korea and superseding the earlier Minerals Security Partnership, FORGE operates as a plurilateral coalition of 54 countries and the European Commission.32 It is designed to establish a preferential trading zone for critical minerals.36 Its most potent geoeconomic mechanism is the implementation of coordinated reference prices and strict price floors.35 By setting minimum price thresholds enforced through adjustable tariffs, FORGE aims to protect Western and allied mining ventures from the PRC’s established, predatory tactic of market manipulation—specifically, dumping cheap processed minerals onto the global market to bankrupt nascent Western competitors before they can achieve commercial scale.35

Expanding the perimeter of technological defense beyond raw materials, the U.S. formalized the Pax Silica alliance in December 2025, culminating in India joining as the tenth signatory in February 2026 alongside nations like Japan, the UK, Australia, and Israel.38 Pax Silica aggressively aligns the industrial policies of advanced economies to secure the entirety of the technology stack—from mineral extraction and advanced manufacturing to semiconductor fabrication, data centers, and AI infrastructure.38 By committing to pro-innovation frameworks, cross-border investments, and the reduction of coercive dependencies, Pax Silica explicitly attempts to isolate adversarial nodes from the critical technologies that will define the 21st century.39

The European Union’s Regulatory Shield: The Critical Raw Materials Act (CRMA)

Across the Atlantic, the European Union has operationalized its own aggressive defense mechanisms through the strict implementation of the Critical Raw Materials Act (CRMA), a cornerstone of its broader economic security strategy.43 Realizing the existential peril of its profound dependencies on foreign imports for the green and digital transitions, the EU established ambitious, legally binding benchmarks for 2030. The CRMA mandates that the EU must source at least 10 percent of its annual consumption from domestic extraction, 40 percent from domestic processing, and 25 percent from domestic recycling.44 Crucially, it dictates that no more than 65 percent of the EU’s annual consumption of any strategic material can be sourced from a single third country.44

To achieve these formidable metrics, the EU established a framework to fast-track “Strategic Projects,” offering these initiatives highly accelerated permitting timelines (maximum 27 months for extraction, 15 months for processing) and preferential access to massive public and private financing hubs.43 Following the closure of its second call for applications in early 2026, the European Commission had officially designated 47 internal Strategic Projects located within 13 Member States, and 13 external Strategic Projects located in partner nations such as Canada, Brazil, and South Africa.45

These approved projects heavily emphasize the raw materials directly applicable to both the energy transition and the resilience of the defense and aerospace sectors. The portfolios include extensive projects focusing on lithium, nickel, cobalt, and manganese for battery-grade applications, alongside critical defense inputs such as tungsten, magnesium, and rare earth elements necessary for permanent magnets.45 While institutions like the European Court of Auditors have published reports expressing deep skepticism regarding the realistic feasibility of hitting the 2030 targets—citing severe bottlenecks in domestic production, struggles to secure offtake agreements, and protracted permitting issues that still plague early-stage developments—the CRMA represents an unprecedented, structural mobilization of European statecraft designed to secure the physical inputs of its strategic autonomy.48

| Initiative | Lead Entity | Primary Geoeconomic Objective | Core Mechanism / Investment Scale |

| Project Vault | United States (EXIM Bank) | Shield domestic OEMs and defense contractors from supply shocks and price volatility. | $12B public-private partnership; demand-driven stockpiling of 60 critical minerals with OEM commitments. |

| FORGE | US / Rep. of Korea / 54 Nations | Prevent adversarial market manipulation and predatory pricing (dumping). | Preferential trade zone; establishment of coordinated price floors and adjustable tariffs for minerals. |

| Pax Silica | United States / 9 Allies | Secure the end-to-end technology supply chain (minerals to semiconductors to AI). | Plurilateral alliance protecting sensitive technologies and coordinating cross-border infrastructure investment. |

| EU CRMA | European Commission | Mandate domestic capacity benchmarks and force supply chain diversification. | 10% extraction, 40% processing targets by 2030; accelerated permitting for 60+ designated Strategic Projects. |

Section IV: The Second-Order Effects on Western Military Hardware: The “Price of Resilience”

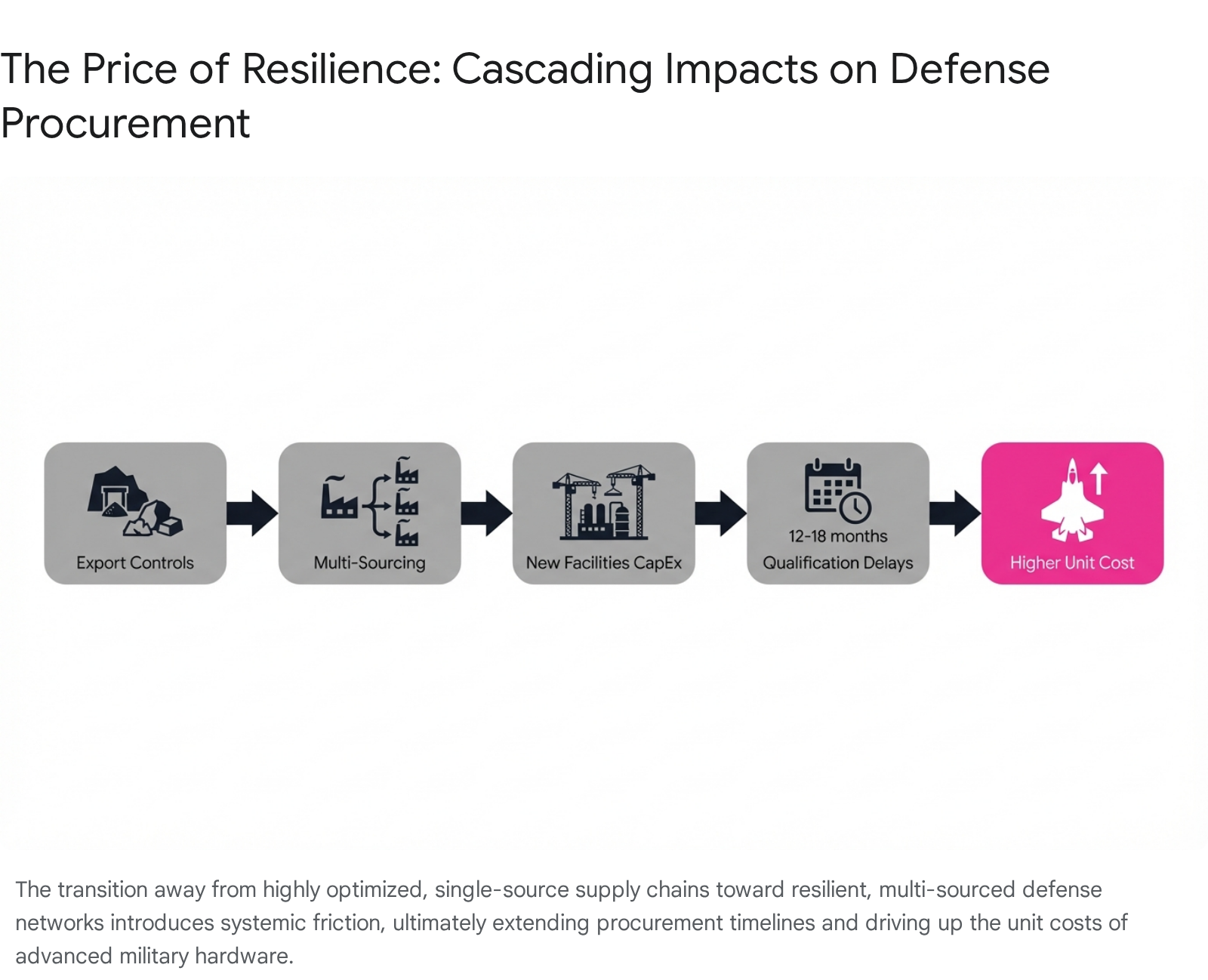

The aggressive, state-directed decoupling of defense supply chains and the rapid transition toward “friend-shoring,” near-shoring, and multi-sourcing is not a frictionless or cost-neutral endeavor. The deliberate rejection of the economically optimized, hyper-globalized trade system of the past three decades has exacted a profound, immediate toll on the Western defense industrial base. The consequence of prioritizing geopolitical reliability and national security over pure cost-efficiency is manifested in severe production delays and spiraling unit costs for advanced military hardware—a complex economic phenomenon widely categorized by analysts and finance ministers as the “price of resilience”.2

Production Timelines, Qualification Bottlenecks, and the Attrition of Readiness

The vulnerability of modern, highly sophisticated defense platforms to even minor supply chain perturbations is staggering. Consider the F-35 Lightning II program, the absolute cornerstone of allied air superiority. Each individual F-35 airframe requires approximately 430 kilograms of specialized materials that are entirely dependent on critical mineral inputs.11 Specifically, the F-35, along with critical precision-guided munitions such as the THAAD and PAC-3 interceptors, relies absolutely on samarium-cobalt (Sm-Co) and neodymium-iron-boron (NdFeB) magnets, as well as complex gadolinium-linked rare earth alloys.49 These specific rare earth materials are non-substitutable; they are critical for maintaining extreme heat tolerance, ensuring accurate missile guidance, and powering high-performance actuation systems in combat environments.51

The supply of these materials is currently under direct threat. In April 2025, the PRC aggressively tightened export licensing controls on specific medium and heavy rare earths, explicitly including samarium and gadolinium, effectively constraining Western defense supply chains.52 Concurrently, China’s sweeping 15th Five-Year Plan (2026–2030) explicitly coupled the domestic expansion of its rare earth industry with even stricter, centralized export management systems.53

The immediate impact on the U.S. military’s operational readiness has been severe. According to reports circulating in early 2026, U.S. military stockpiles maintained a perilous buffer of only two months’ worth of rare earth supplies necessary for systems like missile guidance and fighter jet actuators, posing massive risks to sustained operations in contested theaters.54 Because the specialized infrastructure required to process minerals like yttrium and dysprosium to 99.9 percent purity at temperatures exceeding 1,200°C currently resides almost exclusively in Asia, replacing these inputs with secure, Western-aligned sources requires an arduous, highly technical qualification process.11 Consequently, relatively minor supply shocks in raw material availability now translate into devastating procurement delays lasting 12 to 18 months for critical defense systems.11

This friction is heavily exacerbated by structural inefficiencies within the U.S. defense procurement apparatus. A pivotal 2026 report by the Government Accountability Office (GAO) explicitly warned that supply chain dependencies are critically compounded by the chronic use of Continuing Resolutions (CRs) in U.S. congressional defense appropriations.55 The GAO found that operating under temporary funding constraints hampered the military’s ability to award contracts, drastically delaying the delivery and fielding of crucial equipment.55 Specifically, 36 of 74 acquisition programs surveyed reported severe schedule effects directly tied to CRs, including major modernization efforts like the F-15 Eagle Passive Active Warning Survivability System (EPAWSS).55

Furthermore, the GAO highlighted a dangerous lack of visibility; defense prime contractors often lack total visibility into supply chains that are routinely five or more tiers deep.58 This results in highly costly retroactive auditing and the forced replacement of parts when adversarial components—such as a Chinese-origin alloy discovered by Honeywell in Lockheed Martin’s F-35 engine magnets—are inevitably uncovered deep within the sub-tier manufacturing base.58

The Escalation of Capital Expenditure and Hardware Unit Costs

The second-order financial effect of supply chain weaponization is the structural, permanent elevation of defense procurement costs. The World Trade Organization (WTO) previously issued stark warnings that the fragmentation of global trade into distinct, geopolitically aligned blocs could suppress global real GDP by nearly 7 percent over the long term.2 Within the highly specialized defense sector, this macroeconomic friction is magnified.

The necessity to rapidly rebuild vertically integrated “mine-to-magnet” supply chains domestically requires immense upfront capital expenditure (CapEx).2 Initiatives like the massive heavy rare earth metallization facility being constructed by REalloys in Ohio—which guarantees a “zero-China” sourcing nexus to comply with new 2027 U.S. defense procurement standards—demand tens of millions in immediate funding and years to achieve commercial scale.33 When defense contractors are forced by legislation to abandon highly optimized, single-supplier global models in favor of redundant, multi-sourced networks located in higher-cost jurisdictions, they inherently sacrifice decades of accumulated economies of scale.2

Furthermore, the geoeconomic tools designed to protect these new industries inherently inflate costs. The implementation of price floors under the FORGE initiative, while strategically necessary to protect domestic mining from predatory Chinese dumping, artificially raises the baseline input cost of raw materials for all downstream defense manufacturers.36

The cumulative financial impact is staggering. The GAO report highlights specific instances where the cost of a contract to sustain military facilities more than doubled directly due to CR-related delays and the necessity of re-evaluating supply pipelines in a fractured market.56 As the U.S. Department of Defense imposes new, draconian procurement standards that strictly forbid adversarial sourcing for key components like samarium-cobalt magnets by January 1, 2027, defense contractors are forced to rapidly qualify new, more expensive suppliers to meet compliance deadlines.33

This heavily compressed timeline forces the military establishment to absorb massive premium pricing to guarantee delivery. Consequently, the unit costs of highly complex systems like the F-35—which had previously benefited from slowly descending cost curves achieved through mass volume production and globalized sourcing—are now facing severe, structural upward pressure.58 The fundamental economics of their material inputs have been forcibly restructured by state policy. The integration of geopolitical risk premiums into capital expenditure decisions and supply chain design means that structurally higher military budgets, prolonged delivery timelines, and persistent supply bottlenecks are no longer temporary anomalies; they are the inescapable baseline reality for Western nations operating in the 2026 multipolar environment.2

Conclusion

The geoeconomic landscape of 2026 is defined by the absolute weaponization of critical supply chains. The foundational assumption of the late 20th century—that global markets will inherently and rationally allocate resources based on price, efficiency, and comparative advantage—has been entirely shattered by the reality of state-directed monopolies, predatory pricing, and the strategic preclusion of defense-critical materials.

The PRC’s deep entrenchment in the cobalt and copper extraction sectors of the Democratic Republic of the Congo, coupled with its overwhelmingly commanding ownership of global midstream refining capacity, has exposed catastrophic vulnerabilities within the Western defense industrial base. Simultaneously, the aggressive penetration of Chinese state-owned enterprises into the critical energy grids of South America, prominently highlighted by the severe political frictions currently confronting the Kast administration in Chile, clearly demonstrates that public infrastructure itself is being actively leveraged as a latent, physical sanctions network capable of totally undermining sovereign strategic autonomy.

The sweeping architectural responses executed by the United States and the European Union—ranging from the physical logistics bypass of the Lobito Corridor to the complex geoeconomic mechanisms of Project Vault, Pax Silica, FORGE, and the European CRMA—represent a monumental, albeit historically belated, mobilization of Western statecraft. However, this desperate pursuit of strategic resilience carries a profound and unavoidable cost. By forcing the decoupling of deeply integrated global supply chains and mandating the creation of redundant, multi-sourced networks, Western nations have triggered severe secondary economic and operational effects.

The F-35 Lightning II program, advanced missile interceptor systems, and next-generation aerospace platforms are now fundamentally subject to extended procurement delays lasting up to 18 months, alongside rapidly escalating unit costs. This occurs as the defense sector absorbs the immense friction of replacing highly optimized, adversarial inputs with nascent, heavily subsidized domestic capacity. Ultimately, successfully navigating the 2026 multipolar environment requires a sobering acceptance among Western policymakers that resource security is fundamentally an issue of industrial capability rather than mere geological endowment. As defense departments aggressively recalibrate to face the harsh realities of great power competition, this “price of resilience” will dictate the scope, speed, and financial viability of military modernization for the foreseeable future.

Please share the link on Facebook, Forums, with colleagues, etc. Your support is much appreciated and if you have any feedback, please email us in**@*********ps.com. If you’d like to request a report or order a reprint, please click here for the corresponding page to open in new tab.

Sources Used

- China in the Democratic Republic of the Congo: A New Dynamic in …, accessed March 14, 2026, https://ssi.armywarcollege.edu/SSI-Media/Recent-Publications/Article/3938204/china-in-the-democratic-republic-of-the-congo-a-new-dynamic-in-critical-mineral/

- The Weaponisation of Trade Is Transforming Global Supply Chains, accessed March 14, 2026, https://internationalbanker.com/finance/the-weaponisation-of-trade-is-transforming-global-supply-chains/

- Choke Points: Critical Minerals and Irregular Warfare in the Gray Zone, accessed March 14, 2026, https://irregularwarfare.org/articles/choke-points-critical-minerals-and-irregular-warfare-in-the-gray-zone/

- US Critical Minerals Supply Chain Resiliency Guide – Discovery Alert, accessed March 14, 2026, https://discoveryalert.com.au/resource-independence-strategies-critical-minerals-2026/

- Trump’s critical minerals meet: Who’s attending, what’s at stake? – Al Jazeera, accessed March 14, 2026, https://www.aljazeera.com/economy/2026/2/4/trumps-critical-minerals-meet-whos-attending-whats-at-stake

- Financial Tools for Boosting Resilience of CRM Value Chains and Strategic Stockpiling – Ifri, accessed March 14, 2026, https://www.ifri.org/sites/default/files/2026-02/ifri_eyl-mazzega_donnen_et_michel_financing_stockpilling_march2026.pdf

- Nature-positive rare earth governance: Japan’s strategy in a China-dominated system – DOI, accessed March 14, 2026, https://doi.org/10.1016/j.resourpol.2026.105852

- US challenges Chinese control in race for African minerals – CNBC Africa, accessed March 14, 2026, https://www.cnbcafrica.com/2026/us-challenges-chinese-control-in-race-for-african-minerals

- Inside the $9 billion U.S.-backed critical minerals deal in DRC and what it means for China, accessed March 14, 2026, https://www.mexc.com/news/886644

- Can the DRC Leverage U.S.-China Competition Over Critical Minerals for Peace?, accessed March 14, 2026, https://carnegieendowment.org/russia-eurasia/research/2025/03/can-the-drc-leverage-us-china-competition-over-critical-minerals

- Critical Minerals Meeting in US: Transforming Global Supply Security – Discovery Alert, accessed March 14, 2026, https://discoveryalert.com.au/critical-minerals-national-security-2026/

- Power Moves: How China’s Energy Investments Provide Durable …, accessed March 14, 2026, https://www.csis.org/analysis/power-moves-how-chinas-energy-investments-provide-durable-influence-south-america

- Mineral Commodity Summaries 2026 – USGS Publications Warehouse, accessed March 14, 2026, https://pubs.usgs.gov/periodicals/mcs2026/mcs2026.pdf

- Chile mining sector faces policy test under Kast government, accessed March 14, 2026, https://www.miningreporters.com/noticia/news/2026/03/chile-mining-sector-policy-test-kast-government

- Chinese Control of Critical Energy Infrastructure in Chile – Tearline.mil, accessed March 14, 2026, https://www.tearline.mil/public_page/chinese-control-of-critical-energy-infrastructure-in-chile

- What’s Behind the Submarine Cables Tying Up Chile’s Presidential Transition, accessed March 14, 2026, https://chinaglobalsouth.com/analysis/chile-submarine-cable-china-us-kast-transition/

- The Chinese Cable That Could Trip up Chile’s New Leader, accessed March 14, 2026, https://chinaglobalsouth.com/analysis/china-chile-undersea-cable-us-china-rivalry-kast/

- Visa Restrictions on Chilean Nationals Undermining Regional Security, accessed March 14, 2026, https://www.state.gov/releases/office-of-the-spokesperson/2026/02/visa-restrictions-on-chilean-nationals-undermining-regional-security

- First hundred days: How Kast can accelerate US investment in Chile – Atlantic Council, accessed March 14, 2026, https://www.atlanticcouncil.org/in-depth-research-reports/issue-brief/first-hundred-days-how-kast-can-accelerate-us-investment-in-chile/

- Chile’s new president to signal swift alignment with Trump – The Japan Times, accessed March 14, 2026, https://www.japantimes.co.jp/news/2026/03/12/world/politics/chile-president-alignment-trump/

- Chile’s Kast takes office pledging security crackdown and migration curbs – bne IntelliNews, accessed March 14, 2026, https://www.intellinews.com/chile-s-kast-takes-office-pledging-security-crackdown-and-migration-curbs-431209/?source=chile

- Joint Statement Declaration of Intent from the United States Government and the European Commission on the Lobito Corridor and Investment in the Great Lakes Region – U.S. Embassy to Angola and Sao Tome and Principe, accessed March 14, 2026, https://ao.usembassy.gov/joint-statement-declaration-of-intent-from-the-united-states-government-and-the-european-commission-on-the-lobito-corridor-and-investment-in-the-great-lakes-region/

- Understanding the Lobito Corridor: Infrastructure, Minerals and Trade – PACT, accessed March 14, 2026, https://africanpact.org/2026/02/04/understanding-the-lobito-corridor/

- Lobito Atlantic Railway Transforms Africa’s Critical Mineral Supply Chains – Discovery Alert, accessed March 14, 2026, https://discoveryalert.com.au/critical-mineral-supply-chain-architecture-2026/

- What to know about the Lobito Corridor—and how it may change how minerals move, accessed March 14, 2026, https://www.atlanticcouncil.org/blogs/africasource/what-to-know-about-the-lobito-corridor-and-how-it-may-change-how-minerals-move/

- US and EU critical minerals project could displace thousands in DRC – report | Democratic Republic of the Congo | The Guardian, accessed March 14, 2026, https://www.theguardian.com/world/2025/dec/04/us-eu-critical-minerals-project-drc-report-lobito-corridor

- 2023 Report – Perenco, accessed March 14, 2026, https://www.perenco.com/wp-content/uploads/2024/07/2023-ESG-Report-.pdf

- Project Vault: What the New Critical Minerals Reserve Means for Energy and Manufacturing Companies, accessed March 14, 2026, https://www.jdsupra.com/legalnews/project-vault-what-the-new-critical-7377088/

- Critical Minerals: “Project Vault” and the New US Critical Minerals Playbook, accessed March 14, 2026, https://www.jdsupra.com/legalnews/critical-minerals-project-vault-and-the-9160188/

- Week in Review: Project Vault and the U.S. Strategic Critical Mineral Reserve | EXIM.GOV, accessed March 14, 2026, https://www.exim.gov/news/week-review-project-vault-and-strategic-critical-mineral-reserve

- Project Vault and FORGE: The Administration’s Latest Moves to Secure Critical Minerals, accessed March 14, 2026, https://bipartisanpolicy.org/article/project-vault-and-forge-the-administrations-latest-moves-to-secure-critical-minerals/

- Project Vault and FORGE Signal Next Phase of U.S. Critical Minerals Policy | Brownstein, accessed March 14, 2026, https://www.bhfs.com/insight/project-vault-and-forge-signal-next-phase-of-u-s-critical-minerals-policy/

- REalloys Inc. Announces Plans for Largest U.S. Heavy Rare Earth Metallization Facility with Zero-China Nexus, Targeting Initial Operations in 2027, accessed March 14, 2026, https://www.quiverquant.com/news/REalloys+Inc.+Announces+Plans+for+Largest+U.S.+Heavy+Rare+Earth+Metallization+Facility+with+Zero-China+Nexus%2C+Targeting+Initial+Operations+in+2027

- Critical Minerals Ministerial Introduces New International Cooperation Strategy – CSIS, accessed March 14, 2026, https://www.csis.org/analysis/critical-minerals-ministerial-introduces-new-international-cooperation-strategy

- US critical minerals policy goes collaborative with FORGE – Atlantic Council, accessed March 14, 2026, https://www.atlanticcouncil.org/dispatches/us-critical-minerals-policy-goes-collaborative-with-forge/

- ‘FORGE’-ing ahead to protect critical mineral supply chains in the US, accessed March 14, 2026, https://ceramics.org/ceramic-tech-today/forum-on-resource-geostrategic-engagement/

- Critical Minerals in the Crosshairs: Navigating U.S. Supply Chain Policy and Global Competition – FTI Strategic Communications, accessed March 14, 2026, https://fticommunications.com/critical-minerals-navigating-us-supply-chain-policy-and-global-competition/

- Pax Silica: alliances, frontier and markets in the geopolitics of the chip – Real Instituto Elcano, accessed March 14, 2026, https://www.realinstitutoelcano.org/en/analyses/pax-silica-alliances-frontier-and-markets-in-the-geopolitics-of-the-chip/

- Pax Silica – United States Department of State, accessed March 14, 2026, https://www.state.gov/pax-silica

- United States and India Sign Pax Silica Declaration, accessed March 14, 2026, https://www.state.gov/releases/office-of-the-spokesperson/2026/02/united-states-and-india-sign-pax-silica-declaration

- US Inaugurates Pax Silica With Seven Allies, accessed March 14, 2026, https://bowergroupasia.com/us-inaugurates-pax-silica-with-seven-allies/

- Pax Silica – Wikipedia, accessed March 14, 2026, https://en.wikipedia.org/wiki/Pax_Silica

- Strategic projects on critical raw materials gain momentum in second selection round for potential funding and faster permitting, accessed March 14, 2026, https://single-market-economy.ec.europa.eu/news/strategic-projects-critical-raw-materials-gain-momentum-second-selection-round-potential-funding-and-2026-01-19_en

- Critical Raw Materials Act – Internal Market, Industry, Entrepreneurship and SMEs, accessed March 14, 2026, https://single-market-economy.ec.europa.eu/sectors/raw-materials/areas-specific-interest/critical-raw-materials/critical-raw-materials-act_en

- Strategic Projects for the EU: list of 47 Strategic Projects announced | White & Case LLP, accessed March 14, 2026, https://www.whitecase.com/insight-alert/strategic-projects-eu-list-47-strategic-projects-announced

- EU Designates 13 Non-EU Critical Raw Materials Projects as Strategic | Global Policy Watch, accessed March 14, 2026, https://www.globalpolicywatch.com/2025/06/eu-designates-13-non-eu-critical-raw-materials-projects-as-strategic/

- Selected strategic projects under CRMA, accessed March 14, 2026, https://single-market-economy.ec.europa.eu/sectors/raw-materials/areas-specific-interest/critical-raw-materials/strategic-projects-under-crma/selected-projects_en

- Special report 04/2026: Critical raw materials for the energy transition | European Court of Auditors, accessed March 14, 2026, https://www.eca.europa.eu/en/publications?ref=SR-2026-04

- Press Release – MINING.COM, accessed March 14, 2026, https://www.mining.com/press-release?id=69b01adf4d39924d679c2881

- Trump’s Secret Weapon in the Rare Earth War – MineralPrices.com, accessed March 14, 2026, https://mineralprices.com/trumps-secret-weapon-in-the-rare-earth-war/

- Ucore Accelerates Commercial Planning for Samarium and Gadolinium Oxides as Defense Supply Chains Face Urgent Shortages, accessed March 14, 2026, https://ucore.com/ucore-accelerates-commercial-planning-for-samarium-and-gadolinium-oxides-as-defense-supply-chains-face-urgent-shortages/

- Ucore Accelerates Commercial Planning for Samarium and Gadolinium Oxides as Defense Supply Chains Face Urgent Shortages – Stock Titan, accessed March 14, 2026, https://www.stocktitan.net/news/UURAF/ucore-accelerates-commercial-planning-for-samarium-and-gadolinium-1ichw522931r.html

- US has two months of rare earth supplies left, SCMP reports, accessed March 14, 2026, https://www.mining.com/us-has-two-months-of-rare-earth-supplies-left-scmp-reports/

- US rare earth two‑month buffer: supply‑chain risks for defence projects, accessed March 14, 2026, https://www.geomechanics.io/news/article/us-rare-earth-twomonth-buffer-supplychain-risks-for-defence-projects

- GAO-26-107065, DEFENSE BUDGET: Effects of Continuing Resolutions on Selected Activities and Programs Critical to DOD’s Nationa, accessed March 14, 2026, https://www.gao.gov/assets/gao-26-107065.pdf

- Defense Budget: Effects of Continuing Resolutions on Selected Activities and Programs Critical to DOD’s National Security Mission [Reissued with revisions on Feb. 4, 2026] – GAO, accessed March 14, 2026, https://www.gao.gov/products/gao-26-107065

- DoD Delays, Increased Costs A Result of Continuing Resolutions, GAO Report Finds, accessed March 14, 2026, https://www.nationaldefensemagazine.org/articles/2026/1/22/dod-delays-increased-costs-a-result-of-continuing-resolutions-gao-report-finds

- The U.S. Defense Industrial Base | The Heritage Foundation, accessed March 14, 2026, https://www.heritage.org/military-strength/topical-essays/the-us-defense-industrial-base

- REalloys (NASDAQ: ALOY) Announces Fully Financed Buildout of the Largest Heavy Rare Earth Metallization Facility Outside China, in Partnership with the Saskatchewan Research Council, accessed March 14, 2026, https://markets.businessinsider.com/news/stocks/realloys-nasdaq-aloy-announces-fully-financed-buildout-of-the-largest-heavy-rare-earth-metallization-facility-outside-china-in-partnership-with-the-saskatchewan-research-council-1035918247

- The Pentagon’s Most Important Tech is No Longer “Made in China” – Nasdaq, accessed March 14, 2026, https://www.nasdaq.com/press-release/pentagons-most-important-tech-no-longer-made-china-2026-03-03

- Russia and China Are Running in a Nuclear Arms Race | The Heritage Foundation, accessed March 14, 2026, https://www.heritage.org/defense/commentary/russia-and-china-are-running-nuclear-arms-race

- $3.7 Billion: Estimated Cost of Epic Fury’s First 100 Hours – CSIS, accessed March 14, 2026, https://www.csis.org/analysis/37-billion-estimated-cost-epic-furys-first-100-hours