Executive Summary

The week ending February 28, 2026, encapsulates a highly dynamic, structurally contradictory, and legally volatile period for the United States small arms industry. Market data, federal procurement documents, and intelligence indicators reveal an industry undergoing a fundamental transition. This transition is characterized by severe commercial retail inventory overhangs, an unprecedented and exponential explosion in specialized accessory markets, and highly divergent military procurement strategies that threaten to permanently fracture the domestic defense industrial base. At the civilian consumer level, the broader firearms market is enduring a protracted contraction. Retail unit sales declined significantly throughout the previous year and are projected to fall further throughout 2026, forcing price compression on legacy inventory and driving publicly traded manufacturers to adopt defensive margin-preservation strategies.

Conversely, the market for firearm suppressors and regulated accessories is experiencing historic growth, directly catalyzed by federal legislative action. The elimination of the National Firearms Act (NFA) $200 tax stamp via the “One Big, Beautiful Bill” (OBBB)—which took full effect on January 1, 2026—has unleashed years of pent-up consumer demand, crashing federal processing infrastructure and providing a vital revenue lifeline to domestic retailers. Within the defense and federal agency sectors, domestic manufacturers are finding crucial financial stabilization to offset the commercial slump. The Department of Homeland Security (DHS), specifically through Immigration and Customs Enforcement (ICE) and Customs and Border Protection (CBP), has initiated a massive, multi-million-dollar procurement surge targeting lethal weapons, ammunition, and accessories.

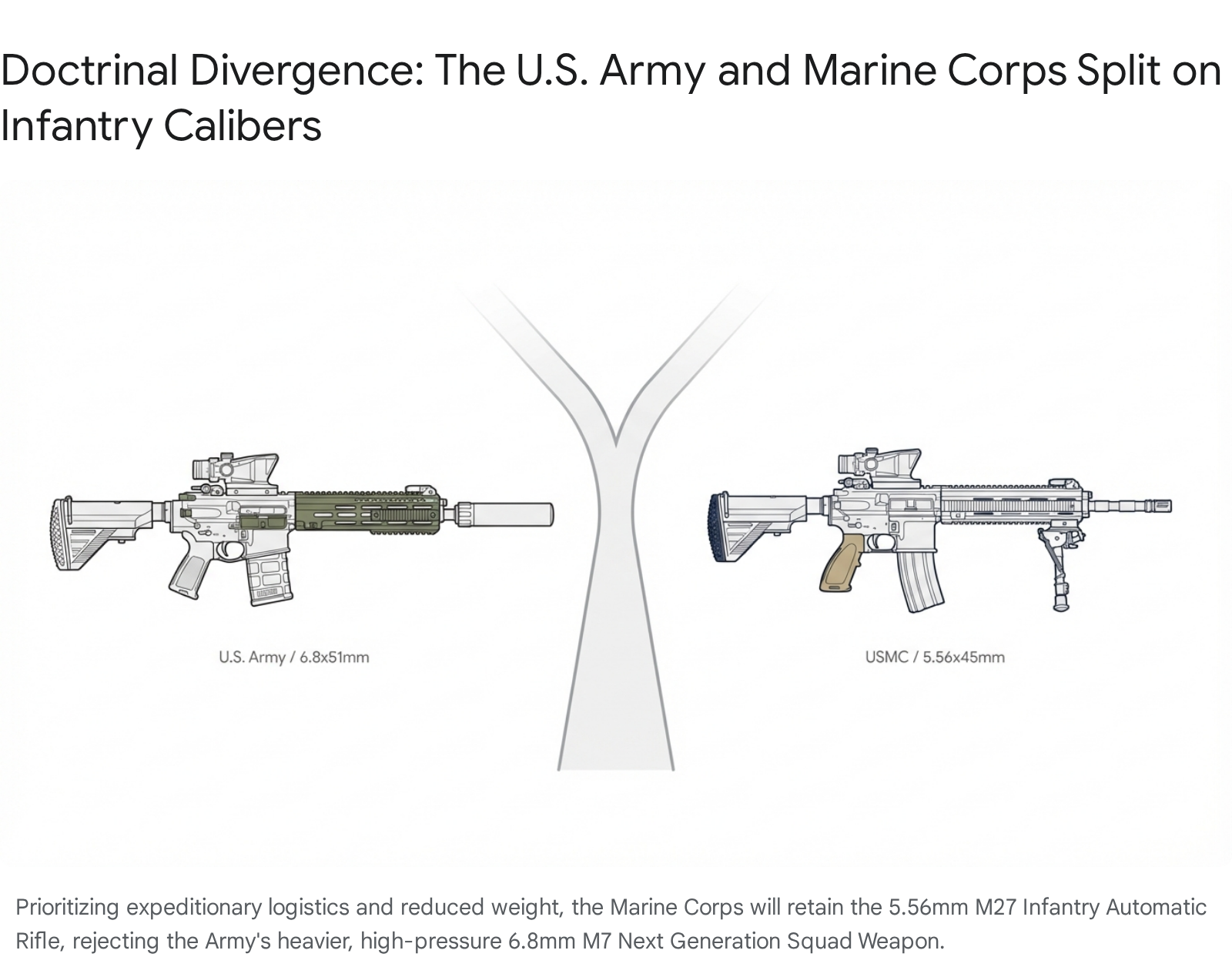

Simultaneously, a profound doctrinal split has formalized within the Department of Defense regarding infantry small arms. The U.S. Marine Corps has officially and definitively rejected the Army’s Next Generation Squad Weapon (NGSW) M7 platform chambered in the high-pressure 6.8x51mm cartridge, opting to retain the 5.56x45mm M27 Infantry Automatic Rifle to preserve expeditionary mobility and logistical agility. This decision forces the ammunition manufacturing sector to maintain dual primary production lines for the foreseeable future. Legally and legislatively, the industry faces an increasingly fragmented and hostile map. Manufacturers are currently fighting a critical battle before the United States Supreme Court in NSSF v. James to protect the federal Protection of Lawful Commerce in Arms Act (PLCAA) from state-level “public nuisance” circumventions. State legislation remains highly polarized, exemplified by Michigan’s simultaneous rollout of strict criminal penalties for unsecured storage alongside new, state-funded public school hunter safety curricula. From an engineering standpoint, the focus remains acutely on recoil mitigation in lighter chassis, modernized manufacturing techniques utilizing automated laser marking, and the rapid integration of artificial intelligence in strategic defense applications following the Pentagon’s abrupt pivot from Anthropic to OpenAI. This comprehensive situation report details the intersecting market forces, engineering realities, political maneuvers, and geopolitical factors driving the small arms sector through the end of February 2026.

1. Commercial Market Dynamics and the Financial Environment

The commercial small arms market is currently defined by a severe “bullwhip effect” originating from the pandemic-era demand surge. Manufacturers and distributors aggressively overproduced to meet historical sales records between 2020 and 2022. As consumer demand normalized, the resulting inventory glut has come to dictate retail pricing, stock valuations, and product development strategies across the domestic landscape.

1.1 Retail Inventory Pressures and Unit Sales Contractions

Data sourced from the Gearfire 2025 Annual Industry Report provides a stark, empirical view of retail velocity and consumer appetite. According to the RetailBI Firearm Sales Index, same-store new firearm unit sales declined by approximately 13 percent in 2025 compared to 2024 levels.1 The broader deceleration has resulted in sales dipping 10.5 percent below the pre-pandemic baseline of 2019, indicating a market that has not merely normalized, but actively contracted below historical trend lines.1

The categories suffering the sharpest declines are traditional long guns. Shotgun sales fell 16 percent year-over-year, and rifles dropped 15.4 percent.1 Handguns continue to command the highest overall volume, serving as the financial anchor for the retail sector, though they too experienced an 11.5 percent drop in sales as the personal defense market achieved saturation.1 The primary structural issue choking the retail channel is inventory density. Current on-hand inventory across the domestic retail sector remains up to 33 percent higher than pre-pandemic levels.2 This physical and financial backlog traps capital, forcing retailers to discount heavily to move stock and generate necessary cash flow to cover overhead.2 Consequently, the average price enthusiasts paid for ammunition, rifles, and optics dropped steadily throughout 2025.2

Retailers are attempting to aggressively reduce this overhang, successfully managing to trim year-end 2025 firearm inventory by 10.6 percent year-over-year, though the broader market remains saturated.1 Forecasts indicate that absent a major geopolitical or domestic political catalyst, 2026 will yield another contraction, with Gearfire analysts predicting an additional 7 to 12 percent drop in overall firearm unit sales.1

1.2 Public Market Equities and Manufacturer Valuations

This macroeconomic reality is directly reflected in public market equities. Major manufacturers are attempting to hold margins through operational discipline and targeted product releases rather than relying on volume. During the week ending February 28, 2026, Smith & Wesson Brands (NASDAQ: SWBI) traded in a narrow, volatile band. The stock remains nearly 35 percent off its 52-week high of $12.15, reflecting entrenched investor hesitation surrounding the broader firearms retail slump.3

| Date | Open | High | Low | Close | Volume |

| Feb 26, 2026 | $11.78 | $11.90 | $11.76 | $11.90 | 254,430 |

| Feb 25, 2026 | $11.89 | $11.95 | $11.66 | $11.76 | 240,410 |

| Feb 24, 2026 | $11.66 | $11.91 | $11.63 | $11.88 | 237,410 |

| Feb 23, 2026 | $12.00 | $12.00 | $11.46 | $11.64 | 396,470 |

Vista Outdoor (NYSE: VSTO), a conglomerate heavily driven by its ammunition segment, has seen similarly complex trading, closing the week around $44.63 amidst ongoing market restructurings and its underlying price-to-earnings volatility.6 The financial data demonstrates that the industry is relying heavily on specialized accessories, law enforcement contracts, and international exports to supplement the sagging domestic civilian market.

2. The 2026 Suppressor Boom and Legislative Catalysts

In stark, aggressive contrast to the contracting standard firearms market, the suppressor accessory segment is undergoing an explosive, historically unprecedented boom. This divergence is the direct and exclusive result of federal legislative action, representing the most significant shift in small arms regulation since the Firearm Owners Protection Act of 1986.

2.1 The “One Big, Beautiful Bill” and Tax Elimination

The “One Big, Beautiful Bill” (OBBB), signed into law by President Donald Trump in the summer of 2025, utilized the federal budget reconciliation process to fundamentally alter the National Firearms Act (NFA).9 The legislation effectively eliminated the punitive $200 NFA tax stamp on suppressors, short-barreled rifles (SBRs), short-barreled shotguns (SBSs), and “Any Other Weapons” (AOWs), reducing the federal transfer tax to zero dollars.9

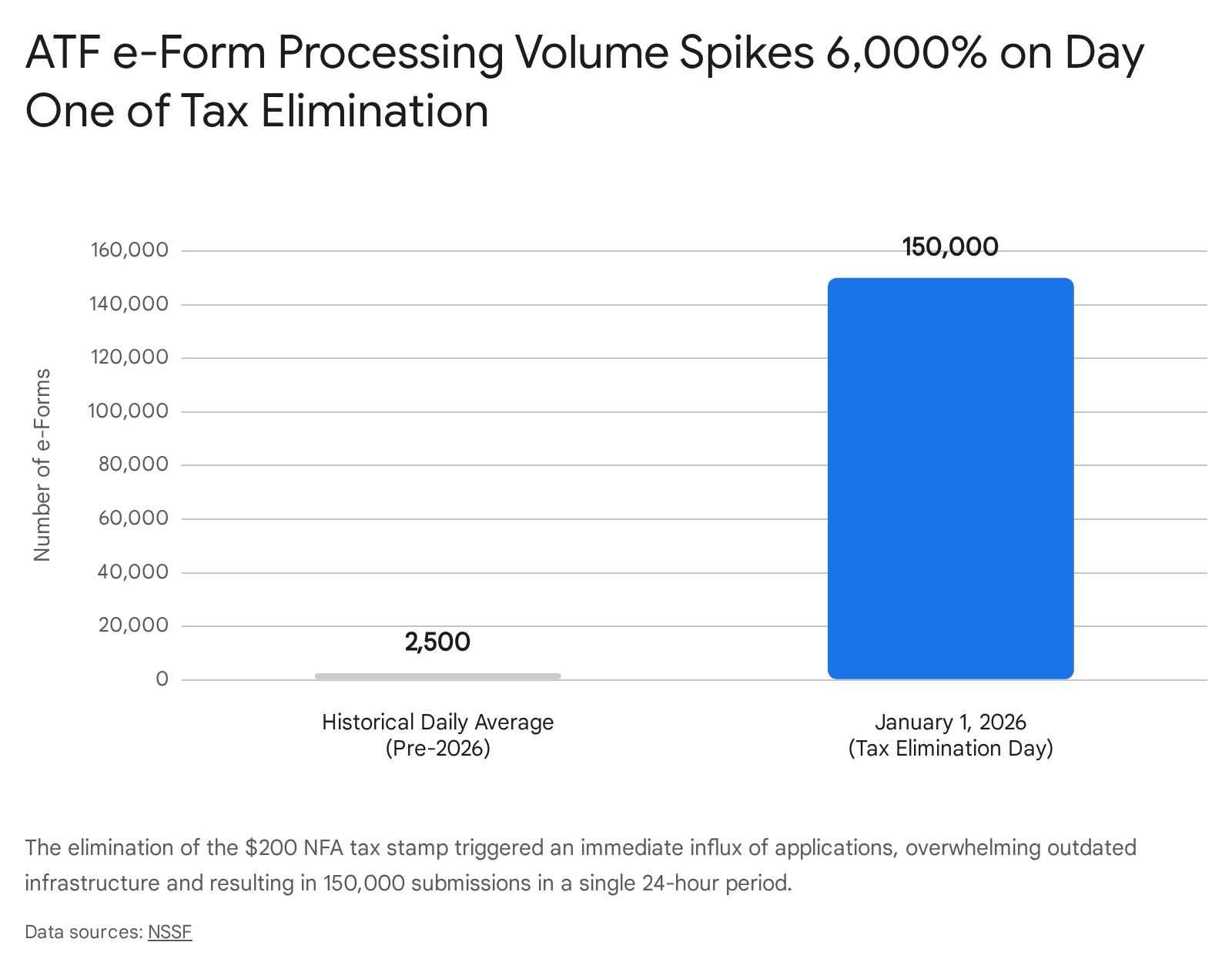

The tax reduction officially took effect on January 1, 2026, triggering an immediate and overwhelming market response.9 The Bureau of Alcohol, Tobacco, Firearms and Explosives (ATF) reported processing an astonishing 150,000 e-Forms on January 1 alone.9 To contextualize the sheer scale of this surge, the typical daily volume for e-Forms involving NFA items historically hovered around 2,500 prior to the legislative change.9 This massive influx of applications instantly overwhelmed the ATF’s outdated and under-resourced IT infrastructure, causing intermittent system glitches, widespread portal crashes, and severe processing delays that continue to frustrate industry members nationwide through late February 2026.9

2.2 Market Expansion and Full Deregulation Advocacy

Even prior to the official January 1 implementation, the market was primed for an explosion. Between 2020 and 2024, the suppressor market experienced a 265 percent growth in Form 4 registrations, doubling the total number of suppressors in circulation and driving the overall market valuation to $820 million by 2024.9 With manufacturers strategically absorbing the $200 tax during the holiday season of late 2025 to front-run the January 1 change, the momentum was immense.9 The American Suppressor Association (ASA) projects that with the finalization of early 2026 data, the total number of registered, consumer-owned suppressors in the United States will safely eclipse 5 million.9 Retailers nationwide, such as those polled in Utah and Idaho, cite suppressor sales as the singular force lifting early 2026 revenues out of the broader slump, noting that foot traffic driven by NFA item curiosity frequently results in secondary firearm or ammunition sales.10

Furthermore, the industry is leveraging this momentum to push for total deregulation. The National Shooting Sports Foundation (NSSF) and aligned advocacy groups are currently utilizing significant political capital to push for the passage of the Hearing Protection Act (H.R. 404 / S. 364).9 This legislation would remove suppressors from the purview of the NFA entirely, treating them as standard firearms requiring only a standard ATF Form 4473 and a National Instant Criminal Background Check System (NICS) check.9 Similarly, the Stop Harassing Owners of Rifles Today (SHORT) Act (H.R. 2395) seeks similar total deregulation for SBRs and SBSs, alongside a mandatory provision requiring the destruction of existing NFA registry records within 365 days of enactment.9 The success of these bills would permanently alter the retail landscape, shifting high-margin accessories from a niche waiting-period purchase to an over-the-counter impulse buy.

3. Ammunition Supply Chain Pressures and Forward Pricing

While firearm unit prices decrease due to retail inventory gluts, ammunition pricing is following a completely divergent, upstream-constrained trajectory. Ammunition availability and retail pricing are currently dictated not by consumer panic buying or political hoarding, but by fundamental, structural limits in the global raw material manufacturing supply chain.12

3.1 Raw Material Bottlenecks and Global Defense Demands

The global ammunition market, valued at $23.3 billion in 2025 and projected to grow steadily to $33.7 billion by 2035 at a CAGR of 3.7 percent, is heavily strained by geopolitical conflict.13 The sustained, high-volume demand for artillery shells, mortars, and military small-caliber rounds in active conflict zones such as Eastern Europe and the Middle East has created a severe bottleneck in the global supply of energetic materials. Specifically, the chemical precursors required for smokeless powder (such as highly refined nitrocellulose) and the specialized, highly volatile chemical compounds required for centerfire primers are operating at absolute maximum global capacity limits.12

Expanding production for these hazardous chemical components is notoriously difficult. It requires years of lead time, massive capital expenditure, specialized engineering expertise, and navigating complex environmental permitting processes. Consequently, short-term supply elasticity for the civilian market is practically zero. When military contracts consume the baseline supply of energetic materials, civilian production lines are forced to bid higher for the remaining fraction, driving up the baseline cost of goods sold.

3.2 Imminent Price Hikes: April 2026

During 2025, average retail ammunition prices experienced a slight 4.8 percent year-over-year decline.2 However, this decline was entirely artificial, driven by retailers liquidating massive reserves of bulk pandemic-era inventory at a loss to generate cash flow.2 The floor for this liquidation has now been reached.

Industry intelligence confirms that several major ammunition brands—including Federal, CCI, and Remington, operating under the Kinetic Group umbrella—have announced definitive price increases scheduled to take effect on April 1, 2026.12 These hikes are a direct, unavoidable pass-through of sustained volatility in raw material acquisition costs.12 Retail analysis suggests that the consumer market has not fully digested the reality of these structural shortages. The most reliable approach for high-volume shooters and retail inventory managers is planning purchases around actual usage rather than attempting to time the market, as supply will continue to arrive in sporadic, allocation-based cycles rather than a return to the state of full, cheap, normalized availability seen prior to 2020.12

4. Doctrinal Fractures in Defense Procurement: NGSW vs. M27

The institutional landscape for small arms in the United States is currently experiencing its most significant doctrinal and logistical shift since the controversial adoption of the 5.56x45mm cartridge during the Vietnam War. During the week ending February 28, 2026, the contrast between the U.S. Army’s focus on technological overmatch and the U.S. Marine Corps’ focus on expeditionary mobility crystallized into definitive, permanent procurement splits.

4.1 The Army’s Pursuit of Overmatch: The M7 and 6.8x51mm

The U.S. Army is pressing forward aggressively with the integration and fielding of the Next Generation Squad Weapon (NGSW) program. Having officially selected SIG Sauer to produce the M7 rifle and the M250 light machine gun, the Army is actively conducting Expeditionary Operational Assessments (EOA).15 Units such as the 101st Airborne Division at Fort Polk are rapidly evaluating the systems under tactical loads to refine the fielding process.17

The foundational engineering logic behind the M7 is lethality overmatch against modern near-peer body armor. The system revolves around the revolutionary 6.8x51mm hybrid cartridge. This ammunition utilizes a specialized high-pressure design—often featuring a stainless steel base joined to a brass body—to withstand internal chamber pressures approaching 80,000 psi, vastly exceeding legacy systems.16 This immense pressure allows the 6.8mm projectile to achieve superior terminal ballistics, massive kinetic energy transfer, and extended effective range compared to the 5.56x45mm NATO cartridge.16 Furthermore, the NGSW’s performance parameters are so promising that the Army has officially suspended a separate effort to design a lightweight machine gun chambered in 6.5mm Creedmoor, consolidating their future infantry lethality entirely around the 6.8mm family.18

However, the ballistic superiority of the 6.8x51mm round introduces severe physical penalties. The high chamber pressures require heavier, reinforced weapon actions and barrels. The ammunition itself is significantly heavier and bulkier, reducing the standard combat load a soldier can carry. Finally, the increased powder charge results in substantially higher felt recoil and severe muzzle blast, necessitating that the M7 be fielded with standard-issue suppressors to mitigate blast overpressure and protect the operator’s hearing and situational awareness.16

4.2 The Marine Corps Rejection and the Return to 5.56mm

Due to these exact logistical and physiological constraints, the United States Marine Corps has officially and definitively rejected the adoption of the M7 rifle for its infantry squads.19 In late February 2026, Marine Corps leadership confirmed that the service will retain the Heckler & Koch-designed M27 Infantry Automatic Rifle, chambered in the traditional 5.56x45mm NATO cartridge, as its primary close-combat formation weapon.19

The Marine Corps operates under a fundamentally different doctrine than the Army, prioritizing amphibious, expeditionary warfare where logistical footprints, resupply chains, and individual infantry weight limits are strictly capped.19 Adopting the M7 would inherently reduce the total volume of fire a Marine rifle squad could carry into a beachhead or littoral environment due to the sheer physical weight and bulk of the 6.8mm ammunition. The M27, originally introduced to replace the M249 squad automatic weapon, has evolved into a highly reliable, accurate, and relatively lightweight standard infantry weapon.19

While the USMC will continue to monitor the Army’s M7 rollout, this decision officially fractures the long-standing post-WWII paradigm of joint-service small arms uniformity. For the domestic industrial base, this divergence is critical. Manufacturers must now simultaneously support two entirely distinct primary infantry calibers across the DoD.19 The 5.56x45mm production lines will remain highly active to supply the USMC and allied nations, providing secondary stability for civilian AR-15 owners concerned about military caliber abandonment, while vast new capital must be invested to scale the complex 6.8x51mm hybrid casing production.

4.3 Broader Acquisition Shifts: ERCA and LTAMDS

The Army’s shift away from rapid, unproven programs extends beyond small arms. The Government Accountability Office (GAO) reported in late February 2026 that the Army is transitioning two massive weapon development programs—the Extended Range Cannon Artillery (ERCA) and the Lower Tier Air and Missile Defense Sensor (LTAMDS)—out of the middle-tier acquisition (MTA) rapid prototyping pathway.20 Because both programs failed to field within the strict five-year MTA window, the Department of Defense denied a waiver for extension. Army acquisition chief Doug Bush determined the programs will now transition to the traditional, highly regulated major capability acquisition pathway.20 The ERCA program, focusing on upgrading BAE Systems’ Paladin M109A7 self-propelled howitzer, highlights the engineering difficulties of safely scaling extreme chamber pressures in larger artillery formats, mirroring the metallurgical challenges faced in the NGSW small arms program.20

5. Federal Law Enforcement Acquisition Surge

While commercial retail markets sag under the weight of inventory, domestic manufacturers are finding robust capital inflow from federal law enforcement agencies. A February 2026 congressional report titled “Armed for Violence,” released by Senator Adam Schiff, detailed a massive, largely unpublicized surge in procurement by the Department of Homeland Security (DHS), specifically targeting U.S. Immigration and Customs Enforcement (ICE) and Customs and Border Protection (CBP).21

During the first year of the current administration’s second term, ICE and CBP committed an aggregate of more than $144 million to weapons, ammunition, and related tactical accessories.21 The scaling of this procurement is dramatic and historically anomalous. ICE’s spending commitments surged over 360 percent—a fourfold increase—compared to 2024 baselines, while CBP’s contracts doubled in the same exact timeframe.21

| Agency | Procurement Category | Scope of Expenditure |

| ICE & CBP | Lethal Weapons & Accessories | Tens of millions allocated for thousands of AR-style patrol rifles, duty pistols, optical sights, and suppressors. |

| ICE & CBP | Ammunition | Over $30 million allocated exclusively for lethal ammunition stockpiling and training reserves. |

| ICE & CBP | “Less-Lethal” Systems | Over $25 million allocated for TASERs, pepper sprays, tear gas canisters, and crowd control launchers. |

The procurement allocations are highly specific. The expenditure includes tens of millions of dollars for thousands of AR-style patrol rifles, duty pistols, and high-end accessories such as optical sights and, notably, suppressors (further fueling the industrial base for suppressed systems mentioned in Section 2).21 An additional $30 million was exclusively allocated for ammunition procurement.21 This massive ammunition buy inherently competes with commercial retail pipelines for primer and powder allocations, exacerbating the civilian market’s upcoming April price increases by locking up finite manufacturing capacity.21 Furthermore, over $25 million was directed toward “less-lethal” crowd control devices, indicating a hardening of border and immigration enforcement tactical postures.21 The scale of this federal spending provides a vital, high-margin revenue floor for domestic small arms manufacturers currently weathering the commercial retail slump.

6. Artificial Intelligence, Strategic Defense, and Unmanned Weaponization

The intersection of small arms, standoff weapons, and artificial intelligence is rapidly evolving, driving unprecedented policy shifts within the Pentagon regarding technology sourcing and autonomous kill chains.

6.1 The Anthropic Ban and the OpenAI Pivot

The underlying digital architecture of modern targeting and strategic defense is undergoing a volatile political restructuring. In late February 2026, the White House issued an executive directive ordering all federal agencies to immediately cease the use of products from the artificial intelligence firm Anthropic, mandating a six-month phase-out period.22 The Pentagon subsequently designated Anthropic a national security supply-chain risk, functionally blacklisting the company from working with the U.S. military or any associated defense contractors.22

The dispute centered on Anthropic’s strict adherence to its internal Terms of Service, which the company argued prohibited its AI tools from being integrated into mass surveillance programs or autonomous weapons systems.22 The administration viewed this refusal as a direct threat to military readiness and an attempt by a commercial entity to dictate federal defense policy.22 In immediate response to the ban, rival AI developer OpenAI rapidly secured a lucrative contract with the Department of Defense to provide its generative and analytical technology for classified military networks.22 This rapid vendor replacement underscores the military’s aggressive posture toward integrating AI into the tactical kill chain, refusing to tolerate commercial entities that attempt to limit the combat application of their software on ethical grounds.

6.2 Modifying ISR Platforms for Deep Strike

Concurrently, the physical platforms carrying these advanced targeting systems are being up-gunned. General Atomics Aeronautical Systems (GA-ASI) announced in late February that it is actively developing the integration of long-range standoff weapons into its MQ-9B SkyGuardian and SeaGuardian unmanned aerial systems.23

Engineering teams are fundamentally modifying the payload capacity, structural stability, and avionics suites of the MQ-9B to carry heavy, precision munitions traditionally reserved for manned fighter aircraft or strategic bombers. These include the Lockheed Martin Joint Air-to-Surface Standoff Missile (JASSM), the Long-Range Anti-Ship Missile (LRASM), and the Kongsberg/Raytheon Joint Strike Missile (JSM).23 Initial flight testing of these configurations is scheduled to begin in 2026.23 This engineering effort represents a massive doctrinal pivot: transforming the drone from a primary ISR (Intelligence, Surveillance, and Reconnaissance) platform into a persistent, deep-strike asset capable of loitering outside hostile anti-access/area-denial (A2/AD) zones in the Pacific and launching coordinated strikes at extreme standoff ranges.23

7. Engineering Innovations and Intellectual Property

Despite the financial headwinds in the retail sector, the engineering and design divisions within the small arms industry remain highly active. Driven by the need to innovate to capture shrinking consumer capital and adapt to complex, highly restrictive state laws, manufacturers are focusing on modernized legacy platforms and advanced manufacturing techniques.

7.1 Modernizing the Lever-Action and Concealed Carry

Product reporting following the massive January 2026 SHOT Show indicates a continuation of several distinct consumer trends.24 Rather than risking entirely unproven, ground-up architectures in a weak market, manufacturers are leaning heavily into modernizing highly successful legacy platforms. Notable releases include the Blaser R8 Professional 2.0 straight-pull rifle, updating a classic European hunting design, and KelTec’s reintroduction of the deep-concealment PR-3AT, capitalizing on the persistent demand for micro-compact defensive handguns.25

A highly notable engineering trend is the rapid tactical modernization of the lever-action rifle. As several states push to aggressively ban semi-automatic modern sporting rifles (MSRs) via complex feature restrictions, the lever-action platform provides consumers with a 50-state compliant, high-rate-of-fire alternative that avoids semi-automatic regulatory triggers. In February 2026, the United States Patent and Trademark Office (USPTO) issued Patent D1,114,926 to Smith & Wesson Inc. for a new firearm element/attachment explicitly tied to the lever-action rifle ecosystem.26 This patent indicates that major, top-tier manufacturers are investing heavily in tactical upgrades—such as modular M-LOK handguards, threaded barrels for the booming suppressor market, and modernized optics mounts—for century-old operating systems to cater directly to legally restricted markets.

7.2 Recoil Mitigation in Lightweight Chassis

As calibers increase in pressure to defeat body armor (as seen in the military’s 6.8x51mm adoption) and as civilian hunters demand increasingly lighter rifles for backcountry deployment, recoil management has become a paramount mechanical engineering challenge. The physics of internal ballistics dictate that lighter rifle mass results in exponentially higher felt recoil, which degrades shooter accuracy, induces flinching, and dramatically increases target re-acquisition time.

In early February 2026, the USPTO processed application data for Patent 16,532,332, titled “Folding Buttstock for Firearms with Recoil Assemblies Contained Within the Buttstock”.28 Traditional folding stocks on tactical rifles represent a rigid metal-on-metal or polymer lockup; they are inherently poor at dampening kinetic energy. Integrating a complex spring-and-buffer or hydraulic recoil assembly entirely within the folding mechanism itself represents a significant metallurgical and mechanical challenge. The locking hinges must be engineered to withstand the secondary impact of the recoil buffer bottoming out, requiring advanced materials to prevent stress fractures over high round counts. This patent points toward a future where highly compact, foldable rifles can comfortably chamber magnum or Next Generation calibers without physically punishing the operator.

7.3 Advanced Manufacturing Integration: Laser Photonics

The margin compression caused by the retail inventory glut is forcing manufacturers to optimize their assembly lines, reducing labor overhead and increasing part throughput. In mid-February, Laser Photonics Corporation (NASDAQ: LASE) confirmed a substantial order from one of the largest U.S. firearm manufacturers for its CMS Laser semi-automatic marking system.29 This represents the manufacturer’s fifth purchase of the system, indicating a permanent shift away from legacy tooling.29

Automated laser marking is critical for modern firearms manufacturing. It allows for the rapid, deep-engraving of ATF-mandated serialized parts, the application of QR codes for internal digital inventory tracking, and complex aesthetic checkering on grips or frames without the tool-wear, maintenance downtime, and labor costs associated with traditional mechanical engraving or roll-stamping. The adoption of these semi-autonomous systems drastically reduces per-unit manufacturing time, a vital adaptation for manufacturers operating in a contracting retail market where every point of margin is fiercely contested.

8. The Legal Environment: PLCAA Defense and State-Level Polarization

The legal and legislative environment for small arms in February 2026 is sharply bifurcated. At the federal level, the industry enjoys favorable tailwinds regarding deregulation (e.g., the NFA tax removal), but at the state level, a fierce, high-stakes battle is underway regarding both ownership restrictions and the fundamental civil liability of manufacturers.

8.1 Defending the PLCAA: The NSSF v. James Supreme Court Petition

The most critical legal event for the long-term, existential viability of the US small arms industry occurred on February 23, 2026. The National Shooting Sports Foundation (NSSF) officially filed a petition for a writ of certiorari with the U.S. Supreme Court in the case of NSSF v. James.9

This landmark case challenges a New York statute designed explicitly to bypass the federal Protection of Lawful Commerce in Arms Act (PLCAA) of 2005. The PLCAA is the bedrock of the modern commercial firearms industry; it protects manufacturers and dealers from devastating civil liability when third parties criminally misuse their products.9 However, the PLCAA contains a narrow, highly specific “predicate exception,” allowing lawsuits if a manufacturer knowingly violated a state or federal statute directly applicable to the sale or marketing of the firearm.9

New York, followed by roughly 10 other states, passed “public nuisance” laws attempting to weaponize this exception. These states argue that standard marketing campaigns or otherwise lawful sales practices inherently create a public nuisance, thereby violating the new state statutes and triggering the predicate exception.9 The U.S. Court of Appeals for the Second Circuit allowed the New York law to stand in 2025. The NSSF’s petition to the Supreme Court highlights a critical circuit split, noting that the D.C. and Ninth Circuits have adopted a stricter, common-sense reading of the predicate exception.9 From a market perspective, if the Supreme Court declines to hear the case or rules against the NSSF, it opens the floodgates for mass civil litigation designed to bankrupt the domestic firearms manufacturing base via exorbitant legal defense fees and massive civil damage awards.

Simultaneously, state attorneys general are aggressively pursuing individual retailers for negligence at the point of sale. On February 24, 2026, Minnesota Attorney General Keith Ellison announced a $1 million settlement and a consent judgment with regional retailer Fleet Farm.30 The state sued the company in 2022 for negligently selling firearms to straw purchasers, utilizing internal company training documents that highlighted the exact warning signs the retail clerks ignored.30 This settlement enforces strict new internal compliance policies for the retailer and serves as a highly visible warning mechanism that states will aggressively utilize civil law to hold corporations accountable for retail-level compliance failures.

8.2 The Michigan Case Study: A Microcosm of National Tension

The State of Michigan provides a profound case study of the complex, often contradictory legislative forces impacting the firearms market at the local level. Following tragic mass shootings at Oxford High School and Michigan State University, the state enacted sweeping gun control measures that are now actively coming into force, while simultaneously facing fierce political backlash and competing educational initiatives.31

| Michigan Legislation | Status / Effective Date | Core Market or Legal Impact |

| Public Act 17 of 2023 (Secure Storage) | Effective Feb 13, 2026 | Mandates unattended firearms be locked if minors are present. Imposes felony charges up to 10 years for severe violations. Drives local retail sales for biometric safes and lockboxes. 32 |

| Extreme Risk Protection Orders (ERPO) | Active (Repeal Attempted Feb 26, 2026) | “Red flag” laws allowed 287 confiscation orders in recent years. House Republicans introduced a repeal bill citing Second Amendment due process violations. 33 |

| Senate Bill 226 (Government Building Ban) | Advancing in Senate | Criminalizes firearm possession in the State Capitol and Senate/House office buildings, exempting only serving lawmakers with Concealed Pistol Licenses. 34 |

| House Bill 4285 (Firearm Education) | Signed into Law Feb 24, 2026 | Directs the state to develop a voluntary firearm and hunter safety curriculum for public school students (grades 6–12), focusing on responsible handling and outdoor stewardship. 35 |

This schizophrenic legislative environment—where a state mandates severe criminal penalties for unsecured storage in the home while simultaneously funding firearm handling education in public middle schools—forces local retailers to constantly adapt their compliance models, inventory profiling, and community engagement strategies to avoid running afoul of rapidly shifting statutes.

9. Human Engineering: Military Marksmanship and Collegiate Programs

Beneath the macro-level procurement of expensive weapon systems lies the fundamental requirement for human proficiency. The U.S. military heavily utilizes competitive marksmanship not merely as a sporting event, but as a critical laboratory for evaluating human engineering, weapon ergonomics, and combat stress management under extreme conditions.

During the week ending February 28, 2026, the competitive shooting landscape reached a peak, providing vital feedback loops for industry engineers. The U.S. Army is actively finalizing preparations for the 2026 U.S. Army Small Arms Championships (ALL-ARMY), scheduled for March 8-14 at Fort Moore (formerly Fort Benning).36 Hosted by the elite U.S. Army Marksmanship Unit (USAMU), this comprehensive live-fire training event forces Active Duty, Reserve, National Guard, and ROTC personnel to employ both primary and secondary weapon systems under intense, physically demanding competitive stress.36 The ALL-ARMY championship serves a dual purpose: it raises the baseline lethality of the fighting force, and it provides real-time, high-volume data on weapon reliability, ammunition consistency, and optic performance directly to Army engineers and procurement officers.36

Simultaneously, the collegiate pipeline for absolute precision marksmanship was showcased at the United States Military Academy. On February 28 and March 1, 2026, Army West Point hosted the Great America Rifle Conference (GARC) Championship at the Tronsrue Marksmanship Center.39 Featuring top-tier, nationally ranked NCAA programs including No. 1 Kentucky, No. 4 West Virginia, and No. 7 Navy, these smallbore and air rifle competitions push the absolute limits of precision barrel manufacturing, specialized target ammunition, and biometric shooting suits.39 The engineering innovations developed to win at the GARC and NCAA levels—where matches are decided by fractions of a millimeter—routinely filter down into the commercial precision rifle market, driving retail sales in the high-margin bolt-action and specialized rimfire sectors.

10. Strategic Outlook and Analyst Conclusions

Based on the aggregated data, geopolitical shifts, engineering developments, and market indicators from the week ending February 28, 2026, the following strategic realities govern the US small arms industry:

1. The Suppressor Market Will Anchor Retail Revenue: With standard firearm unit sales projected to drop up to 12 percent in 2026, the suppressor market is the single most vital growth vector for commercial retailers and manufacturers. The $0 tax stamp has unleashed a historic wave of demand. Manufacturers must pivot machining time toward baffles, tubes, and quick-detach mounting systems, while retailers must streamline their digital footprint to handle ATF e-Form processing efficiently, despite the agency’s current infrastructure delays. If the HPA or SHORT Act passes, this segment will permanently redefine the retail floor.

2. Divergent Military Supply Chains are Now Permanent: The USMC’s rejection of the 6.8mm M7 solidifies a doctrinal split within the DoD. Ammunition manufacturers must now maintain massive, simultaneous production lines for both the legacy 5.56x45mm NATO cartridge (for the Marines and vast allied forces) and the complex, bi-metal 6.8x51mm cartridge (for the Army). This split guarantees that 5.56mm will not be rendered obsolete in the near or medium term, ensuring stability for civilian AR-15 owners concerned about military caliber abandonment.

3. Ammunition Costs Will Remain High: The April 2026 price increases by major ammunition brands confirm that the global shortage of energetic materials (nitrocellulose, primers) will outlast the current drop in consumer demand. Even as retailers discount rifles to clear inventory, the ongoing conflicts in Eastern Europe and the Middle East will keep the basic cost of shooting high, potentially suppressing long-term recreational volume.

4. Existential Legal Risks Loom Large: The industry’s fate rests heavily on the Supreme Court’s response to the NSSF v. James petition. If states are permitted to utilize consumer protection and public nuisance laws to completely bypass the PLCAA, the risk profile of domestic firearms manufacturing will alter fundamentally. Such an outcome would likely drive insurance premiums to unsustainable levels and force smaller, innovative manufacturers into bankruptcy or corporate acquisition by larger conglomerates capable of weathering protracted litigation.

The industry is navigating a volatile transition, delicately balancing the engineering triumphs of new military calibers and deregulated accessories against the immense economic gravity of an oversupplied civilian market, critical raw material shortages, and an increasingly hostile state-level legal environment.

Please share the link on Facebook, Forums, with colleagues, etc. Your support is much appreciated and if you have any feedback, please email us in**@*********ps.com. If you’d like to request a report or order a reprint, please click here for the corresponding page to open in new tab.

Sources Used

- Gearfire Provides Complimentary Access to Annual Industry Report – NSSF, accessed February 28, 2026, https://www.nssf.org/articles/gearfire-provides-complimentary-access-to-annual-industry-report/

- Prices On Rifles, Ammo, Optics & Suppressors Dropped In 2025, According To Retail Report | An Official Journal Of The NRA – American Rifleman, accessed February 28, 2026, https://www.americanrifleman.org/content/prices-on-rifles-ammo-optics-suppressors-dropped-in-2025-according-to-retail-report/

- Smith & Wesson Brands – 28 Year Stock Price History | SWBI – Macrotrends, accessed February 28, 2026, https://www.macrotrends.net/stocks/charts/SWBI/smith-wesson-brands/stock-price-history

- Historical Price Lookup – Investors | Smith & Wesson, accessed February 28, 2026, https://ir.smith-wesson.com/stock-information/historical-price-lookup/

- Smith & Wesson Stock Price History – Investing.com, accessed February 28, 2026, https://www.investing.com/equities/smith—wesson-historical-data

- VSTO Stock Price Quote & News – Vista Outdoor – Robinhood, accessed February 28, 2026, https://robinhood.com/stocks/VSTO

- Stock Info – Vista Outdoor – Investor Relations, accessed February 28, 2026, https://investors.vistaoutdoor.com/Investors/stock-info/default.aspx

- Vista Outdoor(VSTO) Stock Price, News, Quotes – Tiger Brokers, accessed February 28, 2026, https://www.itiger.com/stock/VSTO

- New Year Buying Surge Shows 2026 Could Be The Year Of … – NSSF, accessed February 28, 2026, https://www.nssf.org/articles/new-year-buying-surge-shows-2026-could-be-the-year-of-suppressors/

- What’s Selling Where January / February 2026 – SHOT Business, accessed February 28, 2026, https://shotbusiness.com/2026/01/departments/whats-selling-where-january-february-2026/

- 2026 Sales Trends Already Emerging – Shooting Industry Magazine, accessed February 28, 2026, https://shootingindustry.com/dealer-advantage/2026-sales-trends-already-emerging/

- Ammunition in 2026: Supply Conditions, Price Pressures, and Market Signals, accessed February 28, 2026, https://blog.targetsportsusa.com/2026-ammunition-outlook-supply-pricing-availability/

- Ammunition Market – Global Insight Services, accessed February 28, 2026, https://www.globalinsightservices.com/press-releases/ammunition-market/

- Ammunition Market Report 2026 – Research and Markets, accessed February 28, 2026, https://www.researchandmarkets.com/reports/5751765/ammunition-market-report

- Next Generation Squad Weapon Winner: Army Picks SIG SAUER – Athlon Outdoors, accessed February 28, 2026, https://athlonoutdoors.com/article/next-generation-squad-weapon-winner/

- Next Generation Squad Weapon of The US Army – Grey Dynamics, accessed February 28, 2026, https://greydynamics.com/next-generation-squad-weapon-of-the-us-army/

- Revolutionizing operational testing: The Next Generation Squad Weapon expeditionary operational assessment | Article – Army.mil, accessed February 28, 2026, https://www.army.mil/article/286308/revolutionizing_operational_testing_the_next_generation_squad_weapon_expeditionary_operational_assessment

- US Army Begins Testing Next Generation Squad Weapon, accessed February 28, 2026, https://defensemirror.com/news/26994/US_Army_Begins_Testing_Next_Generation_Squad_Weapon

- U.S. Marine Corps rejects switch to M7 rifle – Defence Blog, accessed February 28, 2026, https://defence-blog.com/u-s-marine-corps-rejects-switch-to-m7-rifle/

- US Army set to phase down two weapon development programs | Caliber.Az, accessed February 28, 2026, https://caliber.az/en/post/us-army-set-to-phase-down-two-weapon-development-programs

- ARMED FOR VIOLENCE – Senator Adam Schiff – Senate, accessed February 28, 2026, https://www.schiff.senate.gov/wp-content/uploads/2026/02/ARMED-FOR-VIOLENCE-REPORT2.18.26.pdf

- OpenAI announces Pentagon deal after Trump bans Anthropic – WGLT, accessed February 28, 2026, https://www.wglt.org/2026-02-27/openai-announces-pentagon-deal-after-trump-bans-anthropic

- GA-ASI Develops Long-Range Weapons Capabilities for MQ-9B, accessed February 28, 2026, https://www.ga-asi.com/ga-asi-develops-long-range-weapons-capabilities-for-mq-9b

- Comprehensive New-Product Reporting for Firearms and Accessories Introduced in 2026, accessed February 28, 2026, https://www.prnewswire.com/news-releases/comprehensive-new-product-reporting-for-firearms-and-accessories-introduced-in-2026-302684525.html

- ICYMI: Industry News From Jan 31 — Feb 6 2026, accessed February 28, 2026, https://shootingindustry.com/dealer-advantage/icymi-industry-news-from-jan-31-feb-6-2026/

- Firearm – Patents – Justia, accessed February 28, 2026, https://patents.justia.com/patent/D1114926

- Zachary Kusnierz, Westfield, MA (US) – Official Gazette for Patents, accessed February 28, 2026, https://patentsgazette.uspto.gov/week08/OG/html/1543-4/USD1114926-20260224.html

- Application Data – Patent File Wrapper, accessed February 28, 2026, https://data.uspto.gov/patent-file-wrapper/search/details/16532332/application-data

- U.S. firearms manufacturer places order for CMS Laser marking system – Investing.com, accessed February 28, 2026, https://www.investing.com/news/company-news/us-firearms-manufacturer-places-order-for-cms-laser-marking-system-93CH-4505500

- Minnesota obtains significant policy changes and $1 million settlement from Fleet Farm for selling guns to straw buyers despite multiple warning signs, accessed February 28, 2026, https://www.ag.state.mn.us/Office/Communications/2026/02/24_FleetFarm.asp

- Michigan’s Firearm Safety Laws, accessed February 28, 2026, https://firearminjury.umich.edu/mi-firearm-laws/

- New gun safety laws to protect families go into effect February 13 – State of Michigan, accessed February 28, 2026, https://www.michigan.gov/mdhhs/inside-mdhhs/newsroom/2024/02/08/firearms-laws

- Michigan House Republicans introduce bills to repeal gun safety laws, accessed February 28, 2026, https://michiganindependent.com/politics/red-flag-laws-gun-safety-repeal-house-republicans-legislation/

- PROHIBIT GUNS IN LEGISLATIVE OFFICE BUILD. S.B. 225 & 226 – Michigan Legislature, accessed February 28, 2026, https://legislature.mi.gov/documents/2025-2026/billanalysis/Senate/pdf/2025-SFA-0225-U.pdf

- Michigan: Firearm Safety Education Bill Signed Into Law – NRA-ILA, accessed February 28, 2026, https://www.nraila.org/articles/20251226/michigan-firearm-safety-education-bill-signed-into-law

- US ARMY SMALL ARMS CHAMPIONSHIPS – Civilian Marksmanship Program, accessed February 28, 2026, https://thecmp.org/wp-content/uploads/2025/11/2026-All-Army-program.pdf

- 2026 US Army Small Arms Championship – Civilian Marksmanship Program, accessed February 28, 2026, https://thecmp.org/event/2026-us-army-small-arms-championship/

- U.S. Army Marksmanship Unit, accessed February 28, 2026, https://www.army.mil/usamu

- WVU Eyes Fourth Straight Title as GARC Championship Returns to West Point | An NRA Shooting Sports Journal, accessed February 28, 2026, https://www.ssusa.org/content/wvu-eyes-fourth-straight-title-as-garc-championship-returns-to-west-point/