1.0 Executive Summary

The military confrontation involving the United States, Israel, and the Islamic Republic of Iran, which commenced with coordinated strikes on February 28, 2026, has precipitated a structural rupture in the global energy and security architecture.1 At the epicentre of this crisis is the de facto closure of the Strait of Hormuz. Through the deployment of naval mines and the imposition of a highly restrictive, selective transit regime, Iran has effectively throttled the maritime corridor through which approximately 20 million barrels per day (bpd) of petroleum liquids and 20% of the world’s liquefied natural gas (LNG) normally transit.2

For Southeast Asia—a region heavily dependent on imported hydrocarbons to fuel its rapid industrialisation, technological manufacturing, and economic growth—this development represents far more than a cyclical price shock; it is a systemic vulnerability event of unprecedented scale. The crisis disproportionately impacts Asian markets, which absorb over 84% of the crude oil and 83% of the LNG flowing through the Strait of Hormuz.3 The immediate fallout is already severely straining regional power generation infrastructures, crippling maritime and aviation transportation networks, and testing the limits of national security and diplomatic frameworks across the Association of Southeast Asian Nations (ASEAN).8

Currently, global benchmark prices have surged dramatically, with Brent crude spiking above $100 per barrel and peaking near $120 in volatile trading sessions, while localized refined product markets are experiencing even steeper inflationary spikes.9 In response, ASEAN member states are deploying emergency demand-side management tactics. These interventions range from mandated shortened workweeks in the Philippines and public sector telecommuting in Vietnam and Thailand, to targeted fuel rationing and accelerated biofuel blending mandates in Indonesia.2 Simultaneously, the redeployment of critical U.S. military assets from the Indo-Pacific to the Middle East has generated acute “alliance anxiety,” forcing regional capitals to adopt a posture of “crisis-management neutrality” while recalibrating their defence strategies around secondary chokepoints like the Strait of Malacca.13

The intelligence forecast for the next 90 days indicates a nonlinear deterioration of the regional economic and security environment. While strategic petroleum reserves and spot-market interventions may buffer the first 30 days of the crisis, the 60-to-90-day window threatens to trigger severe industrial cascades.7 The exhaustion of middle distillate fuels and LNG stockpiles is projected to force severe refinery run cuts, disrupt regional semiconductor manufacturing, and elevate the risk of civil unrest due to compounding food, logistics, and energy inflation.7 This report provides an exhaustive analysis of the current crisis parameters, exploring the deep interconnections between maritime security, energy policy, and political stability in Southeast Asia.

2.0 The Strategic Operating Environment: Hormuz and Beyond

The strategic landscape in the first quarter of 2026 is defined by asymmetrical warfare, maritime domain constriction, and a rapid, destabilising reordering of global military postures. The conflict has moved beyond conventional military engagements into a sustained campaign of structural economic warfare targeting global supply chains.

2.1 The Mechanics of the Strait of Hormuz Constriction

The conflict has escalated into a sustained campaign of logistical attrition. The United States and Israel have conducted upward of 9,000 combat flights, striking thousands of targets to degrade Iranian ballistic missile infrastructure, air defences, and naval capabilities.9 In retaliation, Iran has engineered a “soft closure” of the Strait of Hormuz, shifting from rhetorical threats to the creation of an operational reality characterised by extreme physical risk and prohibitive financial costs.6

Rather than declaring a formal, legal blockade, Tehran has deployed asymmetrical area-denial tactics. Intelligence assessments confirm that Iran has seeded the strait with Maham 3 and Maham 7 naval mines.4 These high-explosive munitions utilize sophisticated acoustic and magnetic sensors capable of targeting commercial shipping, landing craft, and submersibles from the seafloor up to depths of 100 meters.4 To compound this physical threat, Iran has implemented a selective transit model, declaring that only “non-hostile” ships unassociated with the U.S. and Israel may pass, provided they coordinate directly with Iranian authorities.4 In numerous instances, vessels are reportedly being extorted for transit fees amounting to millions of dollars.4

This hostile posture has effectively collapsed commercial maritime traffic through the chokepoint. Normal daily transits of 70 to 80 vessels have plummeted by 80%, with only sporadic, highly controlled movements occurring through a restricted northern corridor.21 The resulting supply shock has stranded approximately 16 to 20 million barrels per day of crude oil and refined fuels.3 The global energy market has consequently fragmented into two partially disconnected systems: one centred on the Atlantic Basin where supply remains fluid, and another centred on the Gulf, where supply is severely constrained, thereby redistributing geopolitical power to states capable of delivering, rather than merely producing, energy.3

2.2 The Relocation of U.S. Indo-Pacific Assets and Alliance Anxiety

A critical second-order security effect of the Middle East war is the sudden security vacuum perceived by allies in the Indo-Pacific. To sustain its extensive combat operations against Iran, the U.S. Department of Defense has executed a massive and rapid reallocation of strategic military assets away from Asian theatres.13

This strategic shift includes the redeployment of Terminal High Altitude Area Defense (THAAD) system launchers from bases in South Korea, the removal of Patriot missile defence batteries, the transfer of guided munitions stockpiles, and the redirection of approximately one-third of the U.S. naval surface fleet.13 Notably, guided-missile destroyers usually based in Yokosuka, Japan, alongside carrier strike groups, have been diverted to the Arabian Sea and the Persian Gulf.13

For Southeast Asian nations navigating the complex strategic competition between Washington and Beijing, this pivot is highly destabilizing. It validates long-standing regional anxieties regarding the physical limitations of the American security umbrella during simultaneous global crises. Regional intelligence analysts note a growing phenomenon of “alliance anxiety,” characterized by profound concerns that opportunistic adversaries may exploit this distraction to aggressively alter the status quo in the South China Sea or the Taiwan Strait.13 While Japan and South Korea have voiced direct concerns about deterrence capacity, Southeast Asian defence planners are being quietly forced to reassess their reliance on extra-regional security guarantees and consider more autonomous regional defence postures.7

2.3 The “Malacca Dilemma” and ASEAN Maritime Security Postures

As the Strait of Hormuz constricts, the strategic premium on the Strait of Malacca has amplified exponentially. Carrying roughly 23.2 million barrels per day of oil and 29% of total global maritime oil flows, Malacca is the world’s largest oil chokepoint by volume and serves as the primary conduit for East Asia’s economic survival.14 For Beijing, the “Malacca Dilemma”—the strategic fear that its primary energy lifeline could be severed by hostile powers or blocked by regional instability—has never been more acute.14

The heightened global risk profile has prompted a swift and severe reaction from the international maritime insurance industry. Leading mutual marine insurers, including Norway’s Gard and Skuld, the UK’s NorthStandard, and the American Club, have cancelled war risk cover for the Persian Gulf.25 Where coverage is reinstated, premiums have skyrocketed by 50% to 100%, reaching up to 1% of the total value of the insured asset.25 This financial deterrent is forcing massive rerouting of global fleets and pushing vessel traffic toward alternative, longer routes that increase reliance on Southeast Asian transhipment hubs.

In Southeast Asia, this translates to increased pressure on the Malacca Straits Patrol (MSP), a cooperative security framework established by Indonesia, Malaysia, Singapore, and Thailand.27 While the MSP has historically been successful in deterring localized piracy and armed robbery, the current geopolitical climate demands a massive upgrade in maritime domain awareness (MDA). Security infrastructure in the Straits is highly localized, with deterrent effects diminishing rapidly beyond a 50-nautical-mile radius of security posts.28 Regional navies are now forced to monitor for the potential spillover of irregular warfare tactics seen in the Gulf, including GNSS spoofing, drone surveillance, and state-sponsored sabotage, ensuring that ASEAN’s critical waterways remain open amid global maritime panic.22

3.0 Macroeconomic Transmission: The Anatomy of the 2026 Energy Shock

The economic transmission of the Hormuz crisis into Southeast Asia is fundamentally different from the supply chain shocks experienced during the COVID-19 pandemic or the 2022 Russia-Ukraine conflict. This is not merely a redirection of trade flows; it is a physical blockade resulting in absolute volumetric losses, creating a systemic shock characterized by compounding inflation, currency volatility, and extreme fiscal strain.

3.1 Brent-WTI Spreads and the “Double Premium”

Southeast Asian economies are highly integrated into global manufacturing but remain structurally dependent on imported energy. As global benchmark prices surged in early March 2026, the structural forces of global oil pricing began to heavily penalize Asian importers.11 Unlike the United States, which benefits from domestic crude production priced against the West Texas Intermediate (WTI) benchmark, Asian economies remain firmly tethered to Brent-linked imports and Middle Eastern sour crude blends.11

Under current geopolitical stress, the Brent-WTI spread has widened significantly. Consequently, Southeast Asia is paying a “double premium”: a higher absolute base price for crude oil and an expanding differential that further inflates the cost of imports relative to Western competitors.11 This dual shock forces a fundamental shift in how markets function. Energy pricing is no longer driven purely by demand growth or standard supply quotas; the market is now pricing access itself—access to secure shipping lanes, specialized financing, and geopolitical stability.11 In such an environment, traditional financial hedges weaken, historical market correlations break down, and extreme volatility becomes a systemic feature of the regional economy.

3.2 Inflationary Pressures and Fiscal Subsidy Burdens

The macroeconomic buffer provided by ASEAN’s relatively low inflation entering 2026 is evaporating rapidly.30 Initial assessments by regional macroeconomic surveillance organizations estimated that if oil prices remained elevated at around $90 per barrel, regional inflation would increase by 0.7 percentage points, with a corresponding 0.2 percentage point reduction in GDP growth.30 However, with crude regularly breaching the $100 threshold and peaking near $120, these estimates are proving overly conservative.9

The transmission of these costs to the domestic economy poses a critical challenge. In Southeast Asia, governments frequently utilize complex subsidy mechanisms to shield consumers from global price volatility. In Indonesia, for example, energy subsidies peaked at IDR 886.1 trillion (approximately $59.7 billion) in 2022 during previous price spikes.31 While these were moderated in subsequent years, the 2026 crisis threatens a catastrophic subsidy overrun. The Indonesian government relies on complex compensation schemes, such as reimbursing the state utility PLN for selling power below cost, and compensating the national energy company Pertamina for selling subsidized Solar (diesel) and 3-kg LPG cylinders.31

As the import bill balloons, maintaining these artificial price ceilings drains national foreign exchange reserves and diverts capital away from essential infrastructure and social programs. If governments choose to pass the costs to consumers to protect sovereign credit ratings, they risk triggering immediate social unrest, creating a difficult zero-sum policy environment for regional finance ministries.11

4.0 Disruptions to Southeast Asian Power Generation

Over the past decade, Southeast Asia has fundamentally restructured its power generation strategy. Driven by rapid urbanization, industrialization, and international pressure to decarbonize, the region has aggressively marketed liquefied natural gas (LNG) as the ideal “bridging fuel” to transition away from heavy coal reliance.5 The 2026 crisis has exposed this strategy as a critical vulnerability.

4.1 The Collapse of the LNG “Bridging Fuel” Paradigm

Southeast Asia imports nearly all of its LNG, and its exposure to Gulf suppliers is highly concentrated and deeply alarming. As of 2025, Qatar alone served as the dominant source for key ASEAN economies, supplying 45% of Singapore’s LNG and 28% of Thailand’s total LNG imports.5 The disruption of the Strait of Hormuz—which processes roughly one-fifth of the entire global LNG trade—has effectively fractured this vital supply chain.5

Compounding the logistical blockade of the strait, military action has directly damaged critical infrastructure. Iranian missile strikes have targeted the Ras Laffan Industrial City, the absolute centre of Qatar’s LNG system.34 This has forced QatarEnergy to halt production at several assets and declare force majeure to its international buyers, instantly cutting Qatar’s export capacity by 17% and removing massive volumes of gas from the global market.35

Unlike the crude oil market, which possesses substantial strategic petroleum reserves (SPRs) globally, the natural gas market lacks deep storage buffers and logistical flexibility.7 Furthermore, ASEAN nations are primarily “price-takers” in a brutal global energy market.5 With European nations still structurally reliant on LNG following the loss of Russian pipeline gas in 2022, Southeast Asian buyers find themselves forced into a bidding war against wealthier European and East Asian economies for the limited non-Gulf cargoes available.5 European natural gas futures surged 25% to above €68 per MWh almost immediately, dragging Asian spot prices up alongside them.34

4.2 Emergency Demand Destruction and Grid Management Tactics

Faced with astronomical spot prices and looming physical fuel shortages, Southeast Asian governments have rapidly transitioned from passive market monitoring to active demand destruction to prevent wholesale power grid failures.37 The interventions reflect the severity of the crisis and the thin margins of error within regional power systems.

| Country | Key Demand-Side Energy Management Policies (March 2026) |

| Philippines | Implemented a mandatory four-day workweek for government employees; established targets to reduce national electricity consumption by up to 20%.5 |

| Thailand | Mandated temperature minimums of 26–27°C in government buildings; ordered reductions in elevator usage; launched a national campaign for workers to wear T-shirts instead of business suits to lower cooling demand; considering capping fuel station operating hours at 10:00 PM.38 |

| Vietnam | Ordered extensive telecommuting and work-from-home mandates for public sector employees to drastically cut commercial electricity demand.5 |

| Sri Lanka | Declared nationwide holidays on Wednesdays for public institutions; relaunched the QR code National Fuel Authorisation System with strict weekly quotas based on vehicle categories.2 |

| Singapore | Absorbing significant fiscal pressure as wholesale electricity prices jumped 20% in the third week of March; maintaining price caps to shield the consumer market and protect the financial hub’s operational stability.35 |

These measures illustrate that the energy shock is no longer a market abstraction but a physical force actively reorganizing the daily rhythms of civic and commercial life across Southeast Asia.40

4.3 Structural Reassessments: Coal Reversion and the ASEAN Power Grid

The 2026 crisis is decisively rewriting long-term power planning in Southeast Asia. The foundational narrative that LNG guarantees energy security and supply resilience has been fundamentally discredited.5 In the immediate term, there is a reactionary pivot back to highly polluting fossil fuels. Indonesia, for instance, has actively expanded coal utilization to buffer the petroleum and gas shortfall, prioritizing immediate macroeconomic stability over long-term climate commitments and emissions reduction targets.11 Asian nations are ramping up coal usage to tackle power shortages, acknowledging that while it raises emissions, it provides vital insulation from maritime import dependence.9

Conversely, the shock is heavily accelerating the strategic mandate for renewable energy and regional grid integration. Projects that were previously stalled by bureaucratic inertia, financing debates, and sovereignty concerns are gaining emergency momentum. The realization of the ASEAN Power Grid (APG) is now viewed as an existential security requirement rather than merely an economic ambition.5 By interconnecting national electrical grids, ASEAN aims to pool diverse, localized energy sources—such as extensive hydropower from Laos, emerging offshore wind potential from Vietnam, and geothermal capacity from Indonesia.5 This regionalized approach is seen as the only viable mechanism to systematically dilute the region’s collective reliance on vulnerable maritime energy imports from the Middle East.

5.0 The Transportation and Logistics Crisis

The transportation sector in Southeast Asia is experiencing a compounding, multifaceted crisis. It is driven not only by raw crude oil shortages but by a catastrophic breakdown in the regional refining ecosystem, leading to acute shortages of finished fuels necessary to power aviation, maritime logistics, and domestic transit.

5.1 The Asian Refinery Run-Cut Contagion

The closure of the Strait of Hormuz is fundamentally a “feedstock famine” for Asian refineries.17 Roughly 80% of the 14 to 15 million bpd of Gulf crude that transits the Strait is destined for Asian markets.17 Without this massive inflow of raw material, regional refining hubs have been forced to execute severe “run cuts,” taking an estimated 4 to 5 million bpd of refining capacity offline across the continent.17

In Southeast Asia, the impacts on downstream operations are acute and highly disruptive. Singapore, a major global refining centre, has seen drastic reductions. ExxonMobil’s expansive Jurong Island operations have been cut to 50% capacity or lower, while the Singapore Refining Co has reduced its runs to 60%.17 In neighbouring Malaysia, the Pengerang Refining Company (Prefchem) unexpectedly shut one of its critical 70,000-bpd residue fluid catalytic cracking (RFCC) units, effectively halving the output of its 300,000 bpd facility.42 This forced Petronas Trading Corp to slash shipments and cancel regional diesel and gasoline export cargoes.42

The crisis is mathematically compounded by the fact that the Strait of Hormuz also typically processes 5 to 6 million bpd of finished refined products—representing 19% of all global seaborne trade in fuels.17 Consequently, the total shortfall of usable, finished fuel in Asia approaches an estimated 9 to 11 million bpd, creating a scarcity environment where prices detach from crude oil benchmarks and skyrocket independently.17

5.2 Bunkering Shocks, Maritime Shipping, and War-Risk Insurance

As the primary transhipment hub of the Indo-Pacific, Singapore’s maritime logistics sector is under immense operational and financial strain. The Fujairah bunkering hub in the United Arab Emirates—the world’s third-largest and a critical node outside Hormuz—has been functionally taken offline due to repeated drone-related fires that damaged storage infrastructure and forced suppliers to declare force majeure.34 Hundreds of displaced commercial vessels are scrambling to secure marine fuel in Singapore, Colombo, and Indian ports, creating a severe demand shock.34

This demand surge, paired with the broader regional refining deficit, has sent marine fuel prices into record territory. In Singapore, Very Low Sulphur Fuel Oil (VLSFO) skyrocketed from $490 per tonne in mid-February to over $1,073 per tonne by mid-March.34 Similarly, standard heavy bunker fuel (HSFO) jumped 62% in a matter of weeks.34

Simultaneously, the collapse of security in the Gulf has triggered a massive spike in shipping insurance. War-risk premiums have been added to ocean freight, with rates destined for South and Southeast Asia rising precipitously. Freight rates to India, for example, have jumped to $3,000–$3,500 per 40-foot equivalent unit (FEU).44 Shipping lines are passing these emergency fuel surcharges and insurance premiums directly to charterers and cargo owners.44 For Southeast Asia, this dramatically inflates the cost of all imported goods, raw materials, fertilizers, and agricultural inputs, generating broad-based, supply-side inflation that threatens regional food security.46

5.3 Aviation Constraints and the Middle Distillate Squeeze

The shortage of refined products has caused the prices of middle distillates—specifically diesel and aviation fuel—to soar well above the peaks witnessed during the 2022 energy crisis. In Singapore, gasoil (industrial diesel) prices surged by 57% to $143.88 per barrel, while aviation jet fuel expanded by an unprecedented 114% to nearly $200 per barrel.7

The jet fuel crack spread reached a staggering $52.10 per barrel in mid-March, sending a clear signal that the global system is desperately scrambling for distillate molecules.17 Consequently, regional aviation connectivity is rapidly degrading. Major carriers serving the Asia-Pacific region, such as Qantas and Air New Zealand, have been forced to raise international fares by approximately 5% and cancel roughly 5% of their flight schedules through early May to offset fuel costs.17 This contraction threatens to cripple the tourism and business travel sectors, which are integral pillars of economic stability for many ASEAN economies.48

6.0 Country-Specific Threat Vectors and National Security Responses

The intersection of energy scarcity, logistics breakdowns, and rampant inflation is rapidly evolving into a severe internal security threat for ASEAN member states. Historically, abrupt fuel price shocks in Southeast Asia have served as primary catalysts for social unrest, regime instability, and political upheaval. Each nation is deploying unique strategic countermeasures to mitigate the fallout.

6.1 Indonesia: Biofuel Mandates and Subsidy Brinkmanship

Indonesia, Southeast Asia’s largest economy and a major net importer of refined petroleum products, has deployed a uniquely aggressive countermeasure to insulate its domestic transportation network. To ease its massive $23.46 billion annual petroleum import bill, the government in Jakarta has accelerated its transition from a B40 to a B50 biodiesel mandate—meaning all diesel fuel must contain 50% palm-based biodiesel.49

While this policy provides vital strategic depth to Indonesia’s fuel supply and reduces reliance on the Middle East, it carries severe technical and macroeconomic risks. Implementing a B50 mandate will push Indonesia’s biodiesel production infrastructure near its absolute maximum capacity, utilizing over 97% of available infrastructure and requiring up to 20.1 million kilolitres of biodiesel annually.49 Producing this volume necessitates diverting approximately 16 million tons of crude palm oil (CPO) to domestic fuel tanks.51

This diversion will severely throttle Indonesian CPO exports. Because Indonesia subsidizes its domestic biodiesel program using the revenue generated from palm oil export levies (currently set at 12.5% of the CPO reference price), a sharp drop in exports will directly deprive the state budget of the exact funds needed to maintain the fuel subsidy.51 Furthermore, logistics networks face the threat of widespread engine degradation, as older heavy industrial machinery, railway engines, and marine vessels remain untested on B50 blends, leading to business sector pushback over clogged filters and maintenance costs.49

6.2 Malaysia: Petronas Duality and Supply Chain Complexity

Malaysia’s energy security position is characterized by a complex structural duality: the country is a net energy exporter overall, primarily through its robust LNG exports, but it remains a net crude oil importer heavily reliant on foreign supply to feed its domestic refining sector.52 Domestic crude production has steadily declined from over 700,000 bpd in the 1990s to approximately 350,000 bpd in 2026, while the national refinery system requires about 600,000 bpd to meet domestic fuel demand.52

Petroliam Nasional Bhd (PETRONAS), the national oil and gas company, anticipates that the US-Iran conflict will yield highly mixed financial and operational outcomes.52 While the surge in global crude prices will undoubtedly boost revenue from upstream production, PETRONAS explicitly warns that these gains will be almost entirely offset by exponentially increased costs across the downstream value chain, including importing raw crude, refining, shipping, and war-risk insurance.52

Unlike international oil companies that operate purely on profit-maximizing commercial terms, PETRONAS operates with a mandated responsibility to support Malaysia’s domestic energy security and affordability.52 As global prices rise, fuel subsidy commitments place massive additional pressure on national finances, forcing the government and PETRONAS to absorb billions in losses to prevent sudden price hikes at the pump that could destabilize the economy.52

6.3 The Philippines and Vietnam: Civil Unrest and Strategic Realignment

In the Philippines, the economic breaking point regarding fuel prices has already been reached. In late March, transport groups launched massive, nationwide strikes across 15 to 20 protest centres in Metro Manila and major provinces.53 Protesters demanded the immediate rollback of oil prices, the suspension of excise and value-added taxes on petroleum products, and the expansion of subsidies to protect public transport operators.53 Anticipating severe social unrest and potential violence, the Philippine National Police placed the capital on high alert, deploying nearly 10,000 personnel to manage the strikes.53

Vietnam is similarly exposed, possessing one of the thinnest energy buffers in Asia, with oil reserves estimated to last less than 20 days.7 Retail petrol prices in Vietnam have surged by 50%, generating immediate inflationary shocks across its manufacturing-heavy economy.48

In response to these mutual vulnerabilities, both nations are accelerating structural and diplomatic realignments. Geopolitically, the realisation that extra-regional powers are absorbed in Middle Eastern theatres has catalyzed intra-ASEAN security integration. Manila and Hanoi are moving rapidly to formalize a strategic partnership, deepening diplomatic and law enforcement cooperation, enhancing joint maritime capabilities, and presenting a unified front to ensure regional stability in the South China Sea, effectively hedging against the perceived unreliability of the distracted U.S. security umbrella.54

6.4 ASEAN’s “Crisis-Management Neutrality”

Diplomatically, the broader ASEAN bloc finds itself navigating a treacherous geopolitical minefield. The overarching regional response has been characterized by a strict posture of “crisis-management neutrality”.7 In official communications, ASEAN foreign ministers have expressed “serious concern” over the escalation initiated by the U.S. and Israel, while equally condemning the retaliatory attacks by Iran.56

The diplomatic rhetoric consistently defers to the preservation of international law, the UN Charter, the protection of civilians, and the urgent need to provide emergency consular assistance to the millions of ASEAN nationals working as expatriate labour in the Middle East.56 This neutrality is not passive; it is a calculated, strategic survival mechanism. Unlike Japan or Taiwan—which have aligned rhetorically with Washington’s narrative out of alliance obligations—most Southeast Asian capitals refuse to assign direct blame.37 This hedging behaviour reflects their acute, multifaceted vulnerability: ASEAN nations cannot afford to alienate the United States (their primary security guarantor), antagonise Middle Eastern energy suppliers (upon whom their economies rely), or frustrate China (their primary trading partner).37

7.0 Strategic Intelligence Forecast: 30, 60, and 90 Days

Geoeconomic modelling of the Hormuz closure dictates that the crisis will manifest as a cumulative and highly nonlinear event. Mitigation capacity via alternative pipelines and commercial strategic reserves is structurally insufficient to cover a sustained 20 million bpd deficit.7 The following forecast outlines the expected degradation of Southeast Asian economic and security architectures over the next three months, assuming no immediate diplomatic resolution or military de-escalation.

7.1 The 30-Day Outlook (April 2026): Volatility, Drawdowns, and Immediate Inflation

- Logistics and Markets: The first 30 days will be defined by extreme price volatility and the near-total collapse of standard spot market operations. Shipping rates will remain at record highs, effectively creating a “Circle of Pain” for global logistics as war-risk insurance remains prohibitively expensive or entirely unavailable for key routes.7

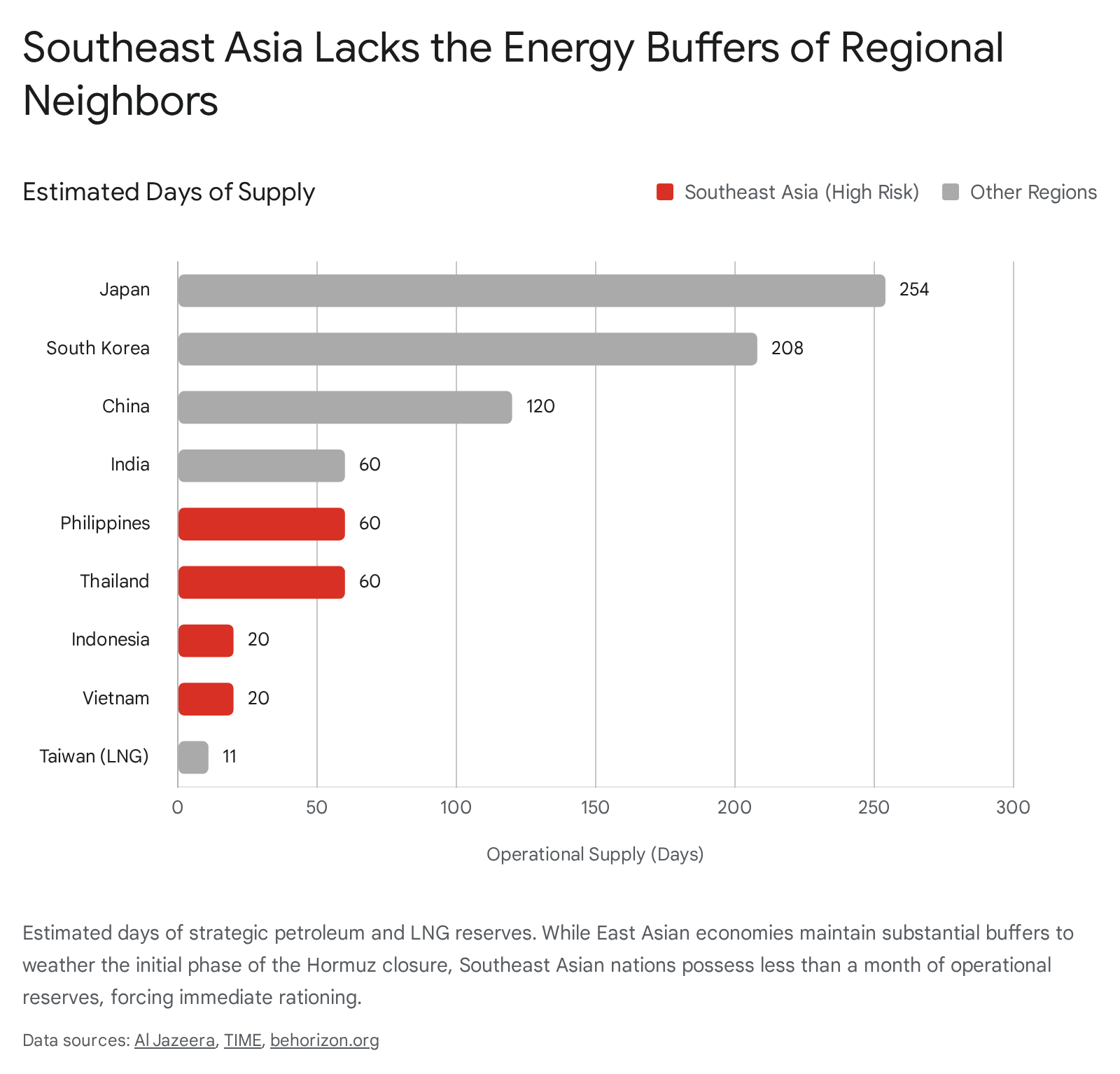

- Inventory Exhaustion: Low-reserve economies will cross critical operational thresholds. Taiwan’s 11-day LNG supply will be completely exhausted, forcing draconian industrial rationing that will immediately ripple into regional supply chains.7 Vietnam and Indonesia will burn through their respective 20-day commercial oil reserves, necessitating emergency government interventions, mandatory fuel quotas for civilian populations, and the cessation of non-essential domestic transport.7 India will operate on thin refinery inventories of just 20 to 25 days, intensifying regional competition for the few available fuel shipments.7

- Social Unrest: The frequency and intensity of protests, similar to the transport strikes witnessed in Manila, will escalate rapidly across urban centres in Thailand, Indonesia, and Malaysia as the initial shock of consumer price inflation takes firm hold.53 Governments will be forced to react with heavy-handed policing measures and emergency, budget-breaking subsidies to maintain civil order and prevent regime instability.

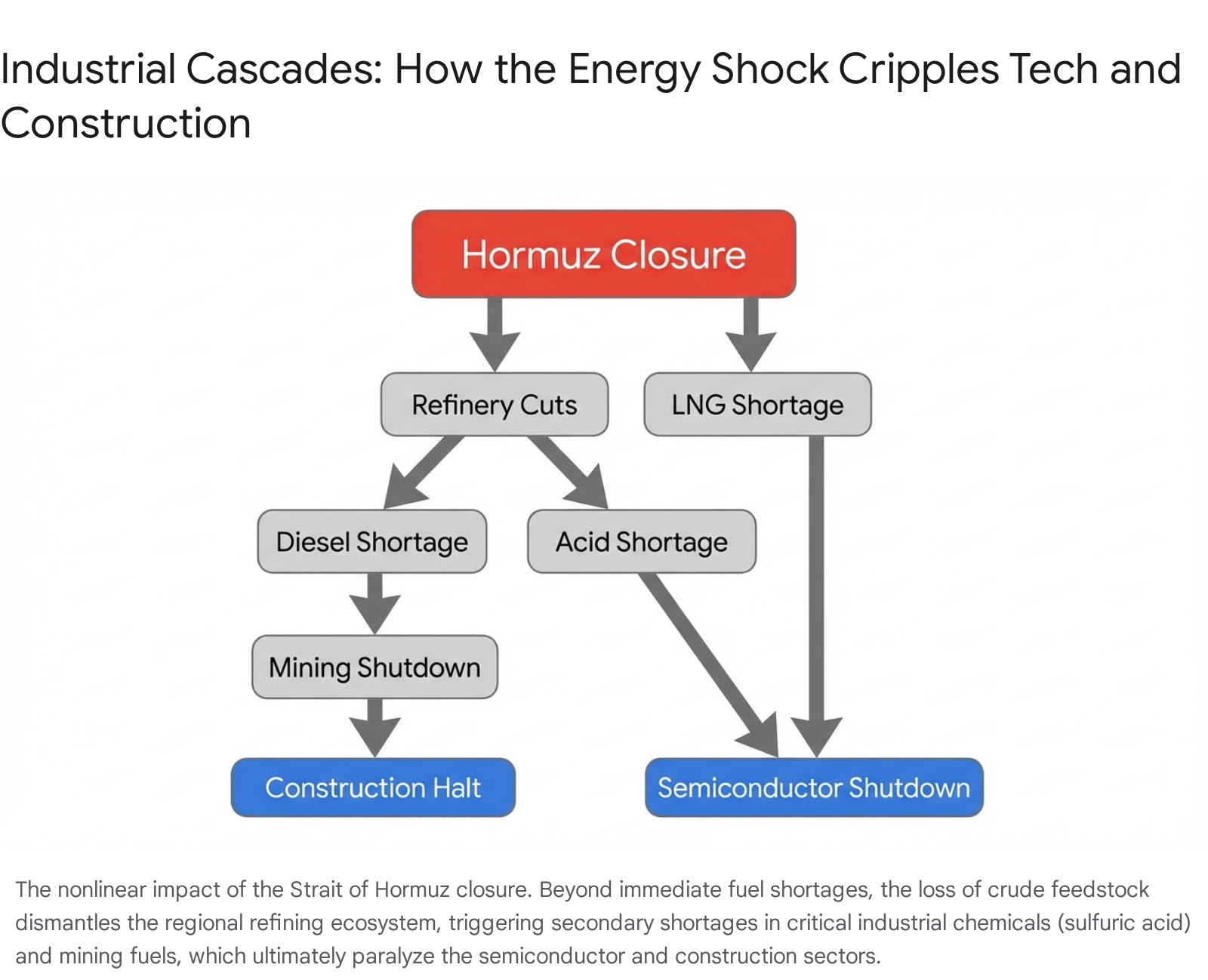

7.2 The 60-Day Outlook (May 2026): Industrial Cascades and Supply Chain Fractures

- Refining and Export Bans: By day 60, China—the region’s “Insulated Giant”—will reach the absolute limits of its 35-day natural gas reserves.7 To protect its domestic market and prevent internal social unrest, Beijing will likely implement strict export bans on refined petroleum products.7 This action will sever a vital secondary supply line for Southeast Asia, deepening the regional deficit of diesel and gasoline.

- The Mining-Energy Loop: The crisis will trigger severe cross-sector industrial cascades. Diesel shortages will force the shutdown of Australian iron ore and coal mining operations, which consume 40% of their operational energy as diesel.7 Because Southeast Asia relies heavily on these raw materials for construction, infrastructure development, and thermal power generation, regional steel industries and major infrastructure projects will stall abruptly, leading to mass layoffs in the construction sector.7

- Semiconductor Threat: The halt in regional oil refining will critically throttle the production of sulphuric acid, a necessary byproduct of refining used extensively in semiconductor etching and cleaning processes.7 Coupled with LNG-driven power rationing in tech hubs like Malaysia and Vietnam, this shortage will cripple Southeast Asia’s electronics and chip-packaging industries. This localized failure will rapidly initiate a global technology supply chain crisis, halting production lines worldwide.7

7.3 The 90-Day Outlook (June 2026): Systemic Energy Failure and Geopolitical Reordering

- Exhaustion of Buffers: By day 90, the mathematically sustainable window for mitigating the disruption permanently closes. Public emergency stocks, which provide a maximum buffer of 73 to 83 days against a 14.5 to 16.5 million bpd net supply shortfall, will be utterly exhausted across the region.7 Coordinated SPR releases, such as the IEA’s 412 million barrels, will prove insufficient to replace the physical loss of maritime flows.12

- Nonlinear Tipping Point: The region will tip from extreme price volatility into absolute physical scarcity. “Just-in-time” LNG and refined fuel shipments will cease entirely.7 Blackouts will transition from managed, rolling schedules to uncontrolled, spontaneous grid failures across highly exposed nations like the Philippines, Vietnam, and Thailand.7

- Strategic Realignment and Financial Shifts: The economic devastation will force a permanent strategic pivot. As the U.S. remains militarily bogged down in the Middle East and traditional Gulf suppliers remain offline, ASEAN states will be forced to abandon their hedging strategies. Survival will necessitate aggressive diversification toward Russian, African, and Latin American hydrocarbons.15 Furthermore, the crisis may accelerate the erosion of dollar dominance in energy trade, as sanctioned entities like Iran and major consumers like China increasingly conduct bypass transactions in Yuan to secure alternative supplies outside the Western financial system.63 “Crisis-management neutrality” will inevitably evolve into a definitive regionalization of supply chains, with Southeast Asia drawing closer to alternative economic and strategic orbits out of sheer material necessity.

Works cited

- Iran-Israel war LIVE: Iran issues its own ceasefire proposal, calling for war reparations and sovereignty over Strait of Hormuz, accessed March 25, 2026, https://www.thehindu.com/news/international/iran-israel-war-west-asia-conflict-march-25-2026-live-updates/article70782463.ece

- From Hormuz to South Asia: The Energy Crisis Unfolding at Home, accessed March 25, 2026, https://moderndiplomacy.eu/2026/03/26/from-hormuz-to-south-asia-the-energy-crisis-unfolding-at-home/

- After Hormuz: Winners, Losers, and the Return of Energy Geopolitics, accessed March 25, 2026, https://moderndiplomacy.eu/2026/03/23/after-hormuz-winners-losers-and-the-return-of-energy-geopolitics/

- Iran Update Special Report, March 24, 2026 | ISW, accessed March 25, 2026, https://understandingwar.org/research/middle-east/iran-update-special-report-march-24-2026/

- How the Strait of Hormuz Disruption Exposed Southeast Asia’s …, accessed March 25, 2026, https://chinaglobalsouth.com/analysis/how-the-strait-of-hormuz-disruption-exposed-southeast-asias-fragile-lng-strategy/

- A crisis through Hormuz, accessed March 25, 2026, https://www.jpost.com/jerusalem-report/article-890913

- Hormuz Crisis 2026: Energy Shock & Global Economic Fallout, accessed March 25, 2026, https://behorizon.org/the-economic-clock-of-war-the-geoeconomics-of-the-2026-hormuz-crisis/

- The Iran War is Causing Energy Chaos in Asia | Council on Foreign …, accessed March 25, 2026, https://www.cfr.org/articles/the-iran-war-is-causing-energy-chaos-in-asia

- Trump calls off Strait of Hormuz ultimatum as Iran receives U.S. message from mediators, accessed March 25, 2026, https://www.cbsnews.com/live-updates/iran-war-us-israel-trump-ultimatum-strait-of-hormuz/

- Which countries have strategic oil reserves – and how much? – Al Jazeera, accessed March 25, 2026, https://www.aljazeera.com/news/2026/3/23/which-countries-have-strategic-oil-reserves-and-how-much

- Indonesia Braces for Energy Shock as Hormuz Crisis Ripples Across Asia – Jakarta Daily, accessed March 25, 2026, https://www.jakartadaily.id/local/16216891707/indonesia-braces-for-energy-shock-as-hormuz-crisis-ripples-across-asia

- Tensions in the Middle East: Implications for Southeast Asia, accessed March 25, 2026, https://caseforsea.org/tensions-in-the-middle-east-implications-for-southeast-asia/

- The Iran War and U.S. Force Posture: Unintended Consequences …, accessed March 25, 2026, https://smallwarsjournal.com/2026/03/16/the-iran-war-and-u-s-force-posture-unintended-consequences/

- Hormuz is a trailer. Malacca is China’s real nightmare — and India knows it, accessed March 25, 2026, https://timesofindia.indiatimes.com/world/rest-of-world/hormuz-is-a-trailer-malacca-is-chinas-real-nightmare-and-india-knows-it/articleshow/129802348.cms

- East Asia’s Energy Exposure and Reactions to US-Israel-Iran Conflict, accessed March 25, 2026, https://www.ecssr.ae/en/research-products/reports/2/205254

- Strait of Hormuz Closure: Global Energy Crisis Risks – Discovery Alert, accessed March 25, 2026, https://discoveryalert.com.au/strait-hormuz-energy-chokepoint-2026-2/

- The refinery problem: A different kind of energy crisis in 2026, accessed March 25, 2026, https://www.firstlinks.com.au/the-refinery-problem-a-different-kind-of-energy-crisis-in-2026

- Iran Update Special Report, March 25, 2026 | ISW, accessed March 25, 2026, https://understandingwar.org/research/middle-east/iran-update-special-report-march-25-2026/

- Strait of Hormuz | International Crisis Group, accessed March 25, 2026, https://www.crisisgroup.org/trigger-list/iran-usisrael-trigger-list/flashpoints/strait-hormuz

- MIDDLE EAST LIVE 25 March: All eyes on Strait of Hormuz; war is ‘out of control’, UN chief warns, accessed March 25, 2026, https://news.un.org/en/story/2026/03/1167195

- March 25, 2026: Iran War Maritime Intelligence Daily – Windward, accessed March 25, 2026, https://windward.ai/blog/march-25-maritime-intelligence-daily/

- Maritime security update: Gulf Region / Strait of Hormuz and Red Sea – Skuld, accessed March 25, 2026, https://www.skuld.com/topics/port/port-news/asia/maritime-security-update-gulf-region–strait-of-hormuz-and-red-sea/

- Hormuz Disruptions and Asia’s Energy Resilience – Gulf International Forum, accessed March 25, 2026, https://gulfif.org/hormuz-disruptions-and-asias-energy-resilience/

- Experts: Vital to safeguard Malacca Strait | The Star, accessed March 25, 2026, https://www.thestar.com.my/news/nation/2026/03/12/experts-vital-to-safeguard-malacca-strait

- Maritime insurers cancel war risk cover in Gulf as Iran conflict disrupts shipping, accessed March 25, 2026, https://www.theguardian.com/business/2026/mar/02/maritime-insurers-war-risk-cover-gulf-iran-shipping-strait-of-hormuz

- The Maritime security landscape in the Persian Gulf, Strait of Hormuz and the Red Sea is changing by the hour – DWF, accessed March 25, 2026, https://dwfgroup.com/en/news-and-insights/insights/2026/3/the-maritime-security-landscape-in-the-persian-gulf

- Maritime Security in the MENA Region: Lessons from the Malacca Straits Patrol | MENA2050, accessed March 25, 2026, https://www.mena2050.org/news/maritime-security-in-the-mena-region%3A-lessons-from-the-malacca-straits-patrol

- Infrastructure of Insecurity: Deterring Maritime Incidents in the Malacca Straits, accessed March 25, 2026, https://www.iiss.org/research-paper/2026/02/infrastructure-of-insecurity-deterring-maritime-incidents-in-the-malacca-straits/

- Maritime Intelligence: An Overview – SpecialEurasia, accessed March 25, 2026, https://www.specialeurasia.com/2026/03/25/maritime-intelligence-overview/

- Shock and Resilience: ASEAN+3 and the Conflict in the Middle East, accessed March 25, 2026, https://amro-asia.org/shock-and-resilience-asean3-and-the-conflict-in-the-middle-east

- Indonesia’s Energy Support Measures | International Institute for Sustainable Development, accessed March 25, 2026, https://www.iisd.org/publications/digital-story/indonesia-energy-support-measures

- Oil Rally Sparks Risk of Subsidy Overrun in Indonesia, Indef Says – Jakarta Globe, accessed March 25, 2026, http://jakartaglobe.id/business/oil-rally-sparks-risk-of-subsidy-overrun-in-indonesia-indef-says

- Iran conflict disrupts oil and gas supply – and more energy stories | World Economic Forum, accessed March 25, 2026, https://www.weforum.org/stories/2026/03/iran-conflict-disrupts-oil-and-gas-supply-top-energy-stories-march-2026/

- Iran War at Sea: How the Conflict Is Disrupting Global Trade and Energy, accessed March 25, 2026, https://windward.ai/blog/iran-war-global-trade-and-energy-disruptions/

- Middle East conflict: Energy security risks and price shocks as market volatility hits supply chains, accessed March 25, 2026, https://www.offshore-energy.biz/middle-east-conflict-energy-security-risks-and-price-shocks-as-market-volatility-hits-supply-chains/

- It is unclear if LNG imports can guarantee Southeast Asia’s energy security, accessed March 25, 2026, https://zerocarbon-analytics.org/insights/briefings/it-is-unclear-if-lng-imports-can-guarantee-southeast-asias-energy-security/

- Hormuz closed: East Asia’s energy shock and strategic shift – ThinkChina, accessed March 25, 2026, https://www.thinkchina.sg/politics/hormuz-closed-east-asias-energy-shock-and-strategic-shift

- Middle East crisis: 6 ways Asia is tackling the energy impact | World …, accessed March 25, 2026, https://www.weforum.org/stories/2026/03/middle-east-crisis-6-things-asia-is-doing-to-manage-the-fallout/

- Top News Headlines In Indonesia, Philippines, Singapore & Thailand : March 11, 2026 – Bernama, accessed March 25, 2026, https://www.bernama.com/en/news.php?id=2532903

- RED THREAD: Hormuz shock hits Asia hardest – Euractiv, accessed March 25, 2026, https://www.euractiv.com/news/red-thread-hormuz-shock-hits-asia-hardest/

- Middle East conflict to have limited near-term impact on Southeast Asia power markets, but raises long-term energy security risks – Wood Mackenzie, accessed March 25, 2026, https://www.woodmac.com/press-releases/me-conflict-impact-on-SEA/

- Malaysia’s Prefchem cuts refinery output after shutting gasoline unit, accessed March 25, 2026, https://www.hydrocarbonprocessing.com/news/2026/02/malaysias-prefchem-cuts-refinery-output-after-shutting-gasoline-unit/

- Hormuz closure sends bunker prices to record levels – Splash247, accessed March 25, 2026, https://splash247.com/hormuz-closure-sends-bunker-prices-to-record-levels/

- AFPM ’26: US shipping, supply chains pressured as Middle East conflict raises costs, accessed March 25, 2026, https://www.icis.com/explore/resources/news/2026/03/18/11189903/afpm-26-us-shipping-supply-chains-pressured-as-middle-east-conflict-raises-costs

- Hormuz hangover to last ‘a couple of years’ with consumers paying the price, accessed March 25, 2026, https://www.lloydslist.com/LL1156714/Hormuz-hangover-to-last-a-couple-of-years-with-consumers-paying-the-price

- Hormuz Shutdown Drives Up Bunker Prices, With Broad Effects on Shipping, accessed March 25, 2026, https://maritime-executive.com/article/hormuz-shutdown-drives-up-bunker-prices-with-broad-effects-on-shipping

- How the War With Iran Is Impacting Economies in Asia – TIME, accessed March 25, 2026, https://time.com/article/2026/03/16/us-israel-iran-war-trump-asia-economy-oil-energy-inflation-recession/

- Iran War’s Energy Disruptions Pose Growing Threat to Global Economic Stability, accessed March 25, 2026, https://www.indrastra.com/2026/03/iran-wars-energy-disruptions-pose.html

- Indonesia B50 Biodiesel Mandate: Policy Impact Analysis, accessed March 25, 2026, https://discoveryalert.com.au/strategic-energy-shifts-southeast-asia-2026/

- Indonesia’s biodiesel push | Lowy Institute, accessed March 25, 2026, https://www.lowyinstitute.org/the-interpreter/indonesia-s-biodiesel-push

- B50 or B60: Stagnant Palm Oil Output Can Hamper Indonesia’s Biodiesel Dream, accessed March 25, 2026, https://jakartaglobe.id/business/b50-or-b60-stagnant-palm-oil-output-can-hamper-indonesias-biodiesel-dream

- PETRONAS expects mixed outcomes from war | The Star, accessed March 25, 2026, https://www.thestar.com.my/business/business-news/2026/03/13/petronas-expects-mixed-outcomes-from-war

- Transport strike erupts in Philippines to protest surging fuel costs – Xinhua, accessed March 25, 2026, https://english.news.cn/20260320/56b13369b98246fd876a0bb0ec1d1c4e/c.html

- Joint Statement on the Philippines-United States Bilateral Strategic Dialogue, accessed March 25, 2026, https://asean.usmission.gov/joint-statement-on-the-philippines-united-states-bilateral-strategic-dialogue/

- Philippines and Vietnam Rapidly Building Strategic Partnership | Council on Foreign Relations, accessed March 25, 2026, https://www.cfr.org/articles/philippines-and-vietnam-rapidly-building-strategic-partnership

- ASEAN Foreign Ministers’ Statement on the Situation in the Middle East, accessed March 25, 2026, https://asean.org/asean-foreign-ministers-statement-on-the-situation-in-the-middle-east-3/

- asean foreign ministers’ statement on the situation in the middle east 04 march 2026, accessed March 25, 2026, https://asean.org/wp-content/uploads/2026/03/1-page-ASEAN-Foreign-Ministers-Statement-on-the-Situation-in-the-Middle-East.pdf

- ASEAN Chair’s Statement on the Outcomes of the Special ASEAN Foreign Ministers’ Meeting on the Situation in the Middle East, accessed March 25, 2026, https://asean.org/asean-chairs-statement-on-the-outcomes-of-the-special-asean-foreign-ministers-meeting-on-the-situation-in-the-middle-east/

- ASEAN Chair’s Statement on the Outcomes of the Special ASEAN Foreign Ministers’ Meeting on the Situation in the Middle East, accessed March 25, 2026, https://asean2026.gov.ph/post/view/?title=asean-chair-s-statement-on-the-outcomes-of-the-special-asean-foreign-ministers-meeting-on-the-situation-in-the-middle-east

- pwc-semiconductor-and-beyond-2026-full-report.pdf, accessed March 25, 2026, https://www.pwc.com/gx/en/industries/technology/pwc-semiconductor-and-beyond-2026-full-report.pdf

- Vietnam steps up semiconductor development to fuel growth, accessed March 25, 2026, https://vntradetoca.org/en/vietnam-steps-up-semiconductor-development-to-fuel-growth/

- 412 million barrels will soon flood oil markets — will it matter? – Asia Times, accessed March 25, 2026, https://asiatimes.com/2026/03/412-million-barrels-will-soon-flood-oil-markets-will-it-matter/

- Strait of Hormuz shock: How a war at sea threatens the petrodollar order – The Cradle, accessed March 25, 2026, https://thecradle.co/articles/strait-of-hormuz-shock-how-a-war-at-sea-threatens-the-petrodollar-order