1.0 Executive Summary

As of April 2, 2026, the global energy ecosystem and international maritime trade networks are navigating one of the most severe, synchronized supply disruptions in modern economic history. The ongoing geopolitical and military conflict between the United States, Israel, and the Islamic Republic of Iran—headlined by the aggressive U.S. military campaign designated “Operation Epic Fury”—has effectively paralyzed the Strait of Hormuz. This narrow, highly contested maritime corridor, historically responsible for the transit of approximately 20% of the world’s daily crude oil supply and a commensurate proportion of liquefied natural gas (LNG), remains functionally closed to standard commercial traffic. The operational environment is defined by intense military operations, asymmetric mine-laying tactics, and direct kinetic attacks on merchant vessels by Iranian forces, creating an unprecedented bottleneck of global hydrocarbon logistics.

For the Republic of the Philippines, an archipelago nation that imports approximately 98% of its crude oil requirements from the Middle East, this disruption constitutes a systemic macroeconomic vulnerability and an acute national security threat. In recognition of this extraordinary peril, the national government declared a State of National Energy Emergency via Executive Order No. 110. This declaration has catalyzed a whole-of-government approach aimed at securing alternative energy supplies, implementing early-stage rationing frameworks, and mitigating the compounding socioeconomic fallout that threatens to derail the nation’s post-2025 economic recovery trajectory.

This exhaustive intelligence and energy sector report provides a high-fidelity assessment of the current Philippine oil situation. It details the precise inventory levels across all fuel categories, which currently average 50.94 days of aggregate supply. This buffer is actively being defended through the emergency sovereign procurement of over one million barrels of diesel from alternative regional suppliers, augmented by private sector acquisitions of non-Middle Eastern crude. Furthermore, the report analyzes the unprecedented diplomatic maneuvering by the Philippine government, which recently secured a bilateral concession from Tehran granting “safe passage” to Philippine-bound oil tankers. However, the analysis demonstrates that the systemic friction of skyrocketing war-risk insurance premiums, widespread shipping delays, and the global repricing of the “war premium” on Brent and West Texas Intermediate (WTI) crude continues to heavily impact domestic fuel prices regardless of physical transit guarantees.

The cascading effects of this Middle Eastern crisis extend far beyond the localized gasoline pump. The disruption of global LNG and critical chemical fertilizer shipments through the Strait of Hormuz threatens to induce a secondary, devastating inflationary shock within the Philippine agricultural sector by late 2026. Consequently, the Bangko Sentral ng Pilipinas (BSP) is currently confronting a highly volatile stagflationary paradigm. Inflation projections suggest a breach of the 6.0% threshold in worst-case scenarios, necessitating an abrupt pivot toward monetary tightening. Concurrently, the domestic power sector faces acute, localized vulnerabilities heading into the peak summer demand months, particularly within the Visayas grid, where rising inter-island coal transportation costs threaten to trigger double-digit percentage hikes in baseline electricity rates.

To navigate this complex threat landscape, this assessment provides detailed weekly and monthly supply, demand, and pricing forecasts stretching from early April through June 2026. The analysis culminates in strategic, actionable recommendations for long-term energy security resilience, focusing on structural tax reforms, sovereign strategic petroleum reserves, and grid decentralization.

2.0 Geopolitical Theater: Operation Epic Fury and the Strait of Hormuz Blockade

To accurately forecast the Philippine energy trajectory, one must first dissect the physical and diplomatic realities of the primary conflict zone. The current crisis is not a standard supply-demand fluctuation; it is a profound geopolitical dislocation.

2.1 The Escalation of Hostilities and “Operation Epic Fury”

The contemporary crisis traces its immediate origins to February 28, 2026, when the United States and Israel initiated a series of highly coordinated, joint military strikes against the Islamic Republic of Iran.1 These strikes achieved significant strategic objectives, including the assassination of Iran’s Supreme Leader Ali Khamenei, which immediately plunged the region into a state of total war.1 In retaliation for the decapitation of its leadership, Iran executed a pre-planned strategy of asymmetrical maritime denial, specifically targeting merchant shipping to effectively close the Strait of Hormuz—the world’s most critical energy chokepoint.1

Recognizing the threat to global commerce, the United States Armed Forces launched a dedicated, multi-stage military campaign on March 19, 2026, dubbed “Operation Epic Fury.” This operation was explicitly designed to force the reopening of the strait by systematically neutralizing Iran’s regional naval dominance, drone manufacturing hubs, and coastal missile infrastructure.1 By the first week of April, Pentagon assessments indicated that Operation Epic Fury had degraded approximately 90% of Iran’s missile capacity and decimated the Iranian Revolutionary Guard Corps (IRGC) naval assets, marking the campaign as an unambiguous tactical military success.2

2.2 The April 2nd Strategic Inflection Point and U.S. Posture

Global energy markets experienced extreme whiplash in the opening days of April. On March 31, unconfirmed rumors of a diplomatic breakthrough and imminent de-escalation caused the geopolitical “war premium” on oil to briefly evaporate, sending Brent crude futures tumbling toward the psychological $100 per barrel mark.4 However, this market relief was entirely erased following a prime-time national address delivered by U.S. President Donald Trump on April 1, with reverberations fully quantified by April 2.2

During this address, the President confirmed that while the core strategic objectives of degrading Iran’s military apparatus were nearing completion, the U.S. military would unexpectedly extend its kinetic operations for an additional two to three weeks to strike Iranian infrastructure “extremely hard”.6 Critically, the President signaled a willingness to conclude U.S. military operations without securing the permanent, unconditional reopening of the Strait of Hormuz.6 He explicitly stated that countries heavily reliant on the strait “must take care of that passage” themselves, further threatening to strike Iranian power plants and oil infrastructure if a broader diplomatic deal was not reached.5

This represents a historic abdication of the traditional U.S. role as the absolute guarantor of maritime security and free navigation in the Persian Gulf. By shifting the burden of maritime security to import-dependent nations, the United States has forced countries like the Philippines into unprecedented unilateral diplomatic maneuvering.6 Furthermore, the President’s threats to potentially pull the U.S. out of the NATO alliance due to a lack of allied participation in the Iran conflict have deeply unsettled global institutional stability, increasing the perceived long-term risk of the Middle Eastern theater.6

2.3 The Physical Reality of the Blockade

The operational reality within the Strait of Hormuz remains bleak, regardless of the success of Operation Epic Fury’s aerial campaigns. As of late March, Iranian forces had carried out at least 24 confirmed attacks on commercial vessels, along with three near misses, resulting in sunken tugs, numerous abandoned merchant ships, and significant loss of life among international seafarers.1

Consequently, a massive logistical bottleneck has formed. More than 150 large commercial ships currently sit anchored in the Gulf of Oman and the Persian Gulf, unwilling or unable to risk transit.8 Data from the International Maritime Organization (IMO) and the Joint Maritime Information Center report that daily transits, which typically averaged around 138 vessels prior to the conflict, have dwindled to low double digits.7 Most operators have declared force majeure, as the strait is heavily mined and actively contested.7

The Iranian Parliament further complicated the legal framework of the waterway by passing the “Strait of Hormuz Management Plan” on March 30.10 This legislation asserts Iranian sovereignty over the international waterway, mandating that foreign nations negotiate directly with Tehran for passage and instituting a toll system for transit, while completely banning U.S., Israeli, and allied shipping.10 This unilateral attempt to rewrite the UN Convention on the Law of the Sea has drawn swift condemnation from the United Nations. Secretary-General António Guterres has warned that the denial of freedom of navigation is strangling the world’s poorest populations, specifically citing the impact on the Philippines, and has dispatched Personal Envoy Jean Arnault to attempt to mediate the crisis.11

3.0 Global Energy Architecture and Macro-Level Market Dynamics

The functional closure of the Strait of Hormuz has triggered what is rapidly being recognized as the most severe, multifaceted energy supply crisis in modern history, unwinding more than a year of accumulated global oil oversupply in a matter of mere weeks.12 The strait historically facilitates the transit of approximately 20 million barrels of oil per day, alongside 20% of the world’s LNG trade, making it the central aorta of the global hydrocarbon economy.12

3.1 Crude Oil Price Volatility and the Geopolitical “War Premium”

Prior to the outbreak of hostilities in late February, global oil markets were characterized by soft supply-demand fundamentals. Analysts at J.P. Morgan had projected that these fundamentals would result in Brent crude averaging around $60 per barrel throughout 2026.14 Similarly, the International Energy Agency (IEA) had noted that global observed oil stocks were at their highest levels since early 2021.15

The onset of the conflict, however, injected a massive, structural “war premium” into the market. Brent futures briefly surged to near $120 per barrel during the height of the March exchanges 15, before settling into a highly volatile, headline-driven range just above $100 per barrel following the extension of Operation Epic Fury in early April.2 West Texas Intermediate (WTI) crude mirrored this explosive price action, surging an unprecedented 58% over a 30-day period, reflecting a massive dislocation in the derivatives markets.2

The physical realities underpinning this price action are stark. Crude production losses in the Middle East are currently running at 11 million barrels per day, with Goldman Sachs forecasting that these losses could peak at a staggering 17 million barrels per day before any meaningful regional recovery materializes.13 The structural reality is that alternative pipeline routes bypassing the strait—specifically Saudi Arabia’s East-West pipeline to the Red Sea and the UAE’s Abu Dhabi Crude Oil Pipeline to the Arabian Sea—offer a combined maximum bypass capacity of only 3.5 to 5.5 million barrels per day.16 This covers barely a quarter of the volume Hormuz normally handles. Crucially, five major producing nations, including Iraq, Kuwait, Qatar, Bahrain, and Iran itself, possess absolute zero bypass infrastructure, leaving their entire export capacity stranded behind the blockade.16

Investment banks have entirely rewritten their 2026 macroeconomic outlooks. Goldman Sachs has aggressively raised its Q4 2026 base case for Brent to $71 per barrel, up from prior estimates.13 However, they warn that under a two-month disruption scenario, Brent could reliably reach $93 per barrel, with extreme escalation scenarios threatening to eclipse the all-time high prices recorded during the 2008 financial crisis.13 Crucially, financial analysts contend that even after the military conflict eventually concludes, the structural risk inherent to the Persian Gulf has been permanently repriced. A return to the pre-war energy economics of sub-$70 oil is considered highly unlikely in the near-to-medium term.13

3.2 The Hidden Crisis: LNG and Petrochemical Feedstocks

While crude oil dominates consumer headlines and political discourse, the blockade’s impact on Liquefied Natural Gas (LNG) is arguably more devastating to industrial supply chains and core inflation metrics. Qatar and the United Arab Emirates, which together supply roughly 20% of the global LNG trade (nearly 90% of which is directed to energy-hungry Asian markets), have had their maritime shipments almost entirely severed.16

Following attacks that damaged processing facilities, both QatarEnergy and the Kuwaiti government declared force majeure on all their respective LNG shipments in early March.16 This instantaneous removal of supply caused European natural gas prices to double in a matter of days, jumping from €30/MWh to above €60/MWh as global buyers scrambled for replacement cargoes.16 For the Philippines and the broader Asian manufacturing sector, this LNG crisis translates directly into a severe shortage of petrochemical feedstocks, specifically liquefied petroleum gas (LPG) and naphtha.16 Petrochemical plants are already being forced to cut production of essential polymers, which serve as the raw material for packaging, plastics, and a vast array of consumer goods, ensuring that the inflationary impacts of this war will bleed heavily into non-energy sectors.16

In response to these compounding factors, the IEA has significantly revised its demand forecasts. Widespread flight cancellations and large-scale industrial disruptions have led the agency to reduce its forecast for global oil demand growth in March and April by more than 1 million barrels per day on average, tempering the full-year 2026 growth estimate down to 640,000 barrels per day.15

4.0 Philippine Energy Vulnerability and Domestic Inventory Profile

The Republic of the Philippines stands as one of the most structurally vulnerable nations in the Asia-Pacific region to Persian Gulf disruptions. The nation imports an astonishing 98% of its crude oil requirements from the Middle East, leaving its transportation network, logistics sector, and power generation infrastructure uniquely exposed to the current blockade.17 Domestic crude production is virtually negligible, and energy consumption is overwhelmingly reliant on imported petroleum. As of early 2026, total national consumption is estimated to fluctuate between 473,000 and 486,600 barrels per day.18

4.1 Declaration of Emergency and Inventory Buffers

Recognizing the existential macroeconomic threat posed by the Strait of Hormuz closure, President Ferdinand R. Marcos Jr. signed Executive Order No. 110 on March 24, 2026. This order officially placed the Philippines under a state of national energy emergency—making it the first nation globally to invoke such statutory powers in direct response to the Iran war.20 The President has sought to manage public panic, assuring the populace that the country maintains a sufficient physical supply of crude oil to last until June 30, 2026, while differentiating between raw crude stocks held by refiners and the immediate availability of refined fuel products like diesel.19

Through rapid intervention, the Department of Energy (DOE) has managed to slightly improve the immediate refined fuel buffer. As of March 27, 2026, the national fuel inventory averaged 50.94 days of aggregate supply, representing a vital improvement from the precarious 45-day threshold previously reported by the agency.23

Table 1: Philippine National Fuel Inventory Profile (As of March 2026)

| Fuel Category | Estimated Days of Supply | Primary Domestic Utilization | Strategic Vulnerability Assessment |

| Jet Fuel | 62.69 days | Commercial aviation, domestic logistics | Low immediate physical risk. Enables carriers like Cebu Pacific to maintain schedules through June, though higher prices will force severe ticket surcharges.24 |

| Gasoline | ~59.00 days | Private transportation, light commercial | Moderate risk. Provides a nearly two-month buffer for replenishment procurement from Southeast Asian spot markets.24 |

| Fuel Oil | 57.27 days | Industrial manufacturing, maritime shipping | Moderate risk. Essential for inter-island shipping and heavy industrial baseloads.24 |

| Diesel | ~51.00 days | Heavy logistics, public transport, agriculture | High risk. The backbone of the Philippine economy. Thin margins expose public utility vehicles and supply chain logistics to immediate price shocks.24 |

| LPG | 34.02 days | Household cooking, petrochemical feedstock | Critical risk. Deeply exposed to the Qatari LNG blockade. Shortest supply runway threatens immediate household inflation.24 |

| Source: Philippine Department of Energy Public Briefings.24 |

4.2 Strategic Procurement and Alternative Sourcing Operations

To defend this fragile buffer, the DOE, operating in close coordination with the Philippine National Oil Company–Exploration Corp. (PNOC-EC), has executed an aggressive “oil diplomacy” campaign. The objective is to secure bridging supplies from alternative, non-Middle Eastern sources. The government activated a PHP 20-billion emergency fund, utilizing a whole-of-government approach to target the procurement of up to 2 million barrels of additional refined supply.27

A critical component of this mitigation strategy is a highly structured, four-phase delivery schedule of refined diesel specifically designed to stabilize the anticipated April supply shock 27:

- Late March 2026: Delivery of 142,000 barrels (22.57 million liters) sourced from Japan.27

- Early April 2026: Scheduled arrival of 300,000 barrels (47.7 million liters) from Malaysia and Singapore.27

- Mid-April 2026: Scheduled arrival of 300,000 barrels (47.7 million liters) from North Asia and India.27

- End April 2026: Scheduled arrival of 300,000 barrels (47.7 million liters) from Oman and Singapore.27

This aggregate sovereign procurement of approximately 1.04 million barrels of diesel serves as a vital tourniquet for the domestic logistics sector.29 Concurrently, private sector actors are mirroring these efforts; Petron Corporation, for instance, successfully procured 2.48 million barrels of Russian Urals crude, effectively securing its baseline refinery operations through June.30

However, given the nation’s high daily consumption rate of nearly half a million barrels, these combined volumes function strictly as supplementary emergency buffers rather than comprehensive baseline replacements.18 Furthermore, the emergency highlights a critical infrastructural deficit: because the Philippine government currently lacks sovereign strategic storage facilities, these emergency reserves must be distributed and housed within the commercial storage tanks of private domestic oil companies, complicating sovereign distribution protocols during a severe crisis.24

5.0 Diplomatic Backchannels and Maritime Security: The “Safe Passage” Concession

Faced with the explicit assertion from the United States that heavily reliant nations must independently secure their own passage through the contested Strait of Hormuz, the Philippine government initiated direct, high-level diplomatic backchannels with the Islamic Republic of Iran.

5.1 The Bilateral Safe Passage Agreement

Following emergency directives from Malacañang Palace, Foreign Secretary Theresa Lazaro engaged with Iranian Ambassador Yousef Esmaeil Zadeh to explicitly request that all Philippine-bound commercial vessels be officially designated as “non-hostile” entities by the Iranian military.31 Leveraging long-standing diplomatic and economic relations that date back to 1964—and emphasizing the fact that the Philippines is a non-belligerent entity completely uninvolved in Operation Epic Fury—Manila successfully secured a monumental geopolitical concession.31

On April 2, 2026, the Philippine government confirmed that Iran had formally pledged to allow the safe passage of oil shipments bound for the archipelago through the Strait of Hormuz.32 Tehran conveyed this official position in letters to the United Nations Security Council and the International Maritime Organization.31 This bilateral achievement mirrors similar localized agreements Iran has struck with Bangladesh, China, Russia, Pakistan, and India, effectively weaponizing access to the strait to reward neutral or friendly nations while punitively blockading U.S. and Israeli allies.33

5.2 The Paradox of “Safe” Passage and Financial Friction

While the diplomatic agreement theoretically shields Philippine-flagged or Philippine-bound vessels from kinetic strikes by the IRGC, it absolutely does not insulate the supply chain from the immense financial and logistical friction inherent to operating within an active war zone.

Firstly, vessels granted safe passage must still physically navigate through extremely congested, heavily mined waters while coordinating with Iranian naval assets, causing severe transit delays. The Iranian Parliament’s “Strait of Hormuz Management Plan” also implies that these vessels may be subjected to newly imposed transit tolls.10

Secondly, and more critically, global maritime insurance underwriters ultimately dictate the commercial viability of any transit. In the days immediately preceding the conflict, war-risk ship insurance premiums for transit through the strait skyrocketed from a baseline of 0.125% to between 0.2% and 0.4% of the ship’s total hull value.1 For a Very Large Crude Carrier (VLCC), this represents an instantaneous cost increase of a quarter of a million dollars per voyage.1 Even armed with an Iranian safe-conduct pass, Western insurance syndicates (such as those in London) may simply refuse to underwrite voyages into an active theater where the U.S. military is conducting daily airstrikes. This forces Philippine importers to rely on sub-optimal, high-cost alternative insurance markets, or to engage with the Iranian “Ghost Fleet”—a shadowy network of tankers operating without AIS transponders that often demand payment in Chinese yuan or cryptocurrency to evade Western financial sanctions.5 Thus, the “safe passage” guarantees physical security but entirely fails to mitigate the inflationary cost of the oil delivered.

6.0 Macroeconomic Contagion and Socioeconomic Impacts

The physical disruption of the global oil market is rapidly mutating into a broad-based, systemic macroeconomic crisis for the Philippines. Prior to the outbreak of the Iran war, the BSP’s Business Expectations Survey for February 2026 revealed that corporate confidence was surging, with the 12-month confidence index rising to 51.1% as businesses anticipated robust economic recovery.34 That optimism has been violently derailed by the reality of imported inflation.

6.1 The Inflationary Surge and Monetary Policy Pivot

The Department of Economy, Planning, and Development (DEPDev) projects that the ongoing oil shock will significantly stoke core and headline inflation, severely eroding consumer purchasing power and dragging full-year gross domestic product (GDP) growth down by an estimated 0.2% to 0.3%.35

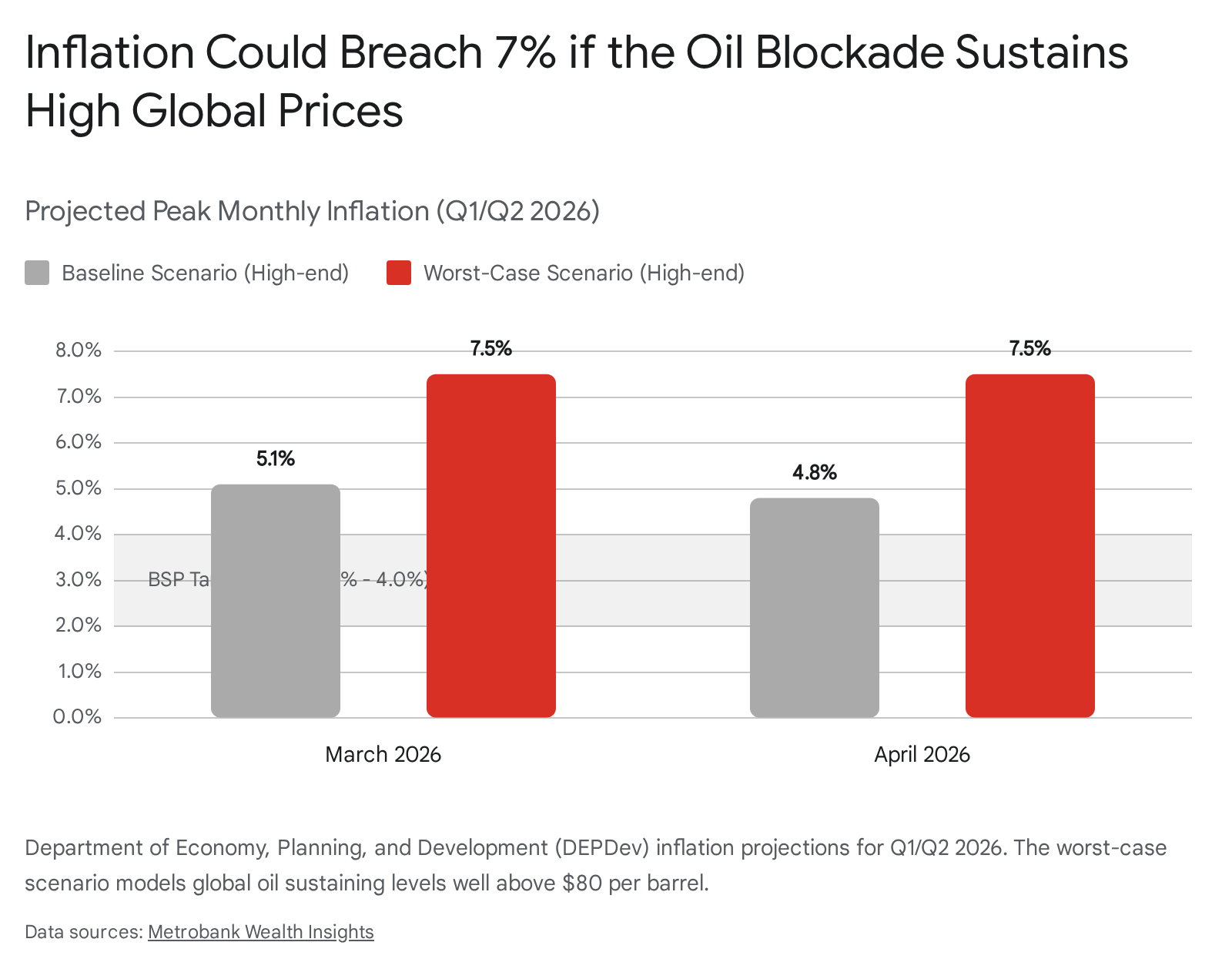

According to baseline scenarios presented to the House Energy Committee, March inflation is projected to accelerate to between 4.5% and 5.1%, with April printing between 4.5% and 4.8%.35 However, under a highly plausible worst-case scenario—where global oil prices sustain a level between $80 and $140 per barrel into the third quarter—Philippine inflation could violently spike to between 6.3% and 7.5% during the critical March-April window.35

This intense inflationary pressure has placed the Bangko Sentral ng Pilipinas (BSP) in a highly precarious position. The Monetary Board had been executing an easing cycle since August 2024, lowering the benchmark policy rate to a multi-year low of 4.25% by February 2026 to stimulate growth.36 However, Finance Secretary and Monetary Board member Frederick D. Go has publicly signaled that the BSP is likely to execute an abrupt pivot. The central bank is now actively considering a rate hike as early as its April 23, 2026, meeting.36 While monetary tightening is viewed as necessary to defend the Philippine peso against further depreciation and anchor runaway inflation expectations, it will inevitably increase domestic borrowing costs, thereby further choking economic momentum and corporate expansion.18

6.2 Domestic Fuel Hikes and the Transport Sector Crisis

At the retail level, the economic pain is immediate and severe. In March, domestic gasoline prices spiked to an average of $1.52 per liter, up substantially from $0.98 in February.37 Entering the first week of April, oil companies implemented massive, consecutive price hikes: diesel prices surged by an unprecedented PHP 12.50 to PHP 12.90 per liter, while gasoline rose by PHP 1.00 to PHP 2.90 per liter.38

To prevent a total operational collapse of the national public transportation network, the Land Transportation Franchising and Regulatory Board (LTFRB) approved provisional, yet substantial, fare increases averaging 19% across all modes of land transport.40 Minimum fares for traditional jeepneys were raised from PHP 13 to PHP 14, and modern jeepneys from PHP 15 to PHP 17, placing immediate strain on the daily budgets of working-class commuters.40 However, transport labor groups remain highly dissatisfied and are threatening strikes. They note that their original petitions were based on pre-crisis fuel prices of roughly PHP 55 per liter, whereas current diesel prices have easily breached the PHP 75 to PHP 80 threshold, rendering the approved fare hikes insufficient to cover daily operational costs.42

6.3 The Invisible Threats: Food Security and the OFW Economy

Two insidious, second-order macroeconomic effects loom over the Philippine economy, threatening to extend the crisis long after the military conflict concludes.

First, the Strait of Hormuz is not merely a hydrocarbon chokepoint; it is the single most critical bottleneck in the global agricultural supply chain. The strait handles 35% of the world’s urea exports, 30% of ammonia, 44% of seaborne sulfur, and 20% of phosphate fertilizers.8 The complete blockage of these essential chemical foundations of modern agriculture threatens a massive, delayed spike in global food prices. The Philippines, heavily reliant on imported fertilizers to maintain its domestic rice yields, will face a severe food inflation wave six to nine months post-crisis if the blockade is not broken, as soil amendments simply fail to arrive.8 This dynamic is already causing panic in the UK, where experts warn food price inflation could double; the Philippines is structurally far more vulnerable to such agricultural shocks.44

Second, the broader Middle East is home to approximately 2.41 million Overseas Filipino Workers (OFWs), whose remittances form a bedrock of the Philippine consumer economy.35 If the regional war metastasizes further, forcing the government to issue a total deployment ban or coordinate the mass repatriation of the estimated 550,000 workers located in immediate conflict zones, the economic fallout would be catastrophic. The DEPDev estimates the economy could lose between PHP 226.6 billion and PHP 232 billion, representing a devastating 65% drop in vital remittances from the region, which would severely degrade the country’s foreign exchange reserves and domestic consumption power.35

7.0 Power Generation and the Summer Electricity Outlook

Compounding the transport fuel crisis is a synchronized threat to the domestic power grid heading into the peak summer demand months of April through June 2026. The Institute for Climate and Sustainable Cities (ICSC) reports that while the overall megawatt power supply across the primary Luzon, Visayas, and Mindanao grids appears mathematically sufficient for the second quarter, the system’s operating margins are extraordinarily thin and structurally fragile.45

7.1 Regional Grid Vulnerabilities

The vulnerabilities of the Philippine electrical grid are highly regionalized, demanding specific operational responses:

- Luzon Grid: Power supply remains conditionally stable, though it is heavily reliant on the timely integration of over 2,000 megawatts (MW) of newly committed solar capacity, including Phase 1 of the MTerra solar project and the Bugallon project.46 Any delays in commissioning these renewables will immediately tighten margins.

- Mindanao Grid: Currently enjoys adequate baseload capacity and continues to export excess power to neighboring regions. However, its margins are projected to tighten considerably by late April as overall national demand surges.46

- Visayas Grid: Identified by the ICSC as the most critically vulnerable region in the archipelago. The Visayas grid currently suffers from structural negative operating margins, meaning local plant generation is intrinsically insufficient to meet regional peak demand.47 The region relies entirely on high-voltage direct current (HVDC) power imports from Luzon and Mindanao. Analysts warn that the Visayas is highly susceptible to triggering “yellow alerts”—official warnings that reserves have fallen below minimum safety levels, preceding rolling brownouts—by May 2026.46

7.2 The Cost Contagion in Coal Logistics

While the Philippines primarily relies on Indonesian coal rather than Middle Eastern oil for its baseload power generation—theoretically insulating the physical fuel supply from the Strait of Hormuz conflict—it is absolutely not immune to the financial contagion. Department of Energy Undersecretary Rowena Guevara confirmed that domestic electricity rates are expected to increase sharply, by 16% to 20%, heading into May.48

This severe rate hike is not driven by a shortage of coal, but almost entirely by the skyrocketing logistical costs of maritime shipping.48 The global repricing of bunker fuel and the displacement of bulk carriers globally due to the Middle East war have caused freight rates from Indonesia to the Philippines to surge. Consequently, Filipino consumers will suffer a devastating double blow: record-high public transport fares paired with double-digit percentage surges in their household electricity bills during the hottest, most energy-intensive time of the year.

8.0 Short-Term Forecast: Weekly Commentary (April 2026)

The following sequence outlines the projected developments and localized impacts across the Philippine energy sector for the next four weeks, predicated on the continuation of Operation Epic Fury and the deeply constrained, heavily bottlenecked reopening of maritime routes.

Week 1 (April 6 – April 12, 2026): Absorbing the “Epic Fury” Extension Shock

The global energy market and the Philippine domestic economy will spend the first week of April digesting President Trump’s sudden announcement extending kinetic military operations.

- Supply Dynamics: The Philippine national fuel inventory will begin to draw down from its 50.94-day buffer, as baseline domestic consumption outpaces the trickling arrivals of emergency regional diesel. The second tranche of the DOE’s emergency procurement—300,000 barrels of diesel from Malaysia and Singapore—is slated to arrive, providing targeted, temporary relief to essential commercial logistics corridors.27

- Pricing and Sentiment: Domestic pump prices will fully absorb the weight of the recent PHP 12.50/liter diesel hike.38 Public frustration and labor unrest will mount as the LTFRB’s newly implemented 19% transport fare hikes take full effect on working-class commuters, potentially sparking localized transport strikes.40

- Diplomatic Maneuvering: Expect intense, quiet backchannel coordination between the Philippine Department of Foreign Affairs, the PNOC, and Iranian maritime authorities to operationalize the “safe passage” pledge. Philippine refiners will likely engage in emergency, round-the-clock negotiations with Asian and Middle Eastern insurers to bypass the exorbitant war-risk premiums demanded by London-based syndicates.

Week 2 (April 13 – April 19, 2026): Macroeconomic Reality and Logistics Strain

As the conflict enters the latter half of April, secondary economic indicators will begin flashing red across the Philippine economy.

- Macroeconomics: The DEPDev will likely release preliminary March inflation prints, confirming a decisive breach of the BSP’s 4.0% target ceiling.35 Retailers of fast-moving consumer goods (FMCG) will begin aggressively passing the increased logistics, transport, and petrochemical packaging costs onto the consumer, broadening inflation well beyond the energy sector.

- Supply Dynamics: The third tranche of emergency procurement—300,000 barrels of diesel from North Asia and India—is scheduled to arrive.27 However, localized hoarding behavior in the provinces, driven by panic, may create artificial dry-outs and stockouts at independent, non-major brand filling stations.

- Power Sector: Coal transport costs will finalize their upward adjustment for the quarter. Major distribution utilities (such as Meralco) will likely file petitions with the Energy Regulatory Commission for severe rate adjustments to be applied to the upcoming May billing cycles.

Week 3 (April 20 – April 26, 2026): The Monetary Policy Pivot

This week will be defined by severe institutional reactions to the sustained crisis.

- Macroeconomics: The Bangko Sentral ng Pilipinas (BSP) will hold its pivotal, highly anticipated Monetary Board meeting on April 23.36 Given the sustained elevation of global oil prices, rising core inflation, and the depreciating peso, the BSP is highly likely to reverse its easing cycle. A minimum 25-basis-point rate hike is expected to defend the currency and attempt to anchor runaway inflation expectations.36

- Supply Dynamics: Liquefied Petroleum Gas (LPG) stocks, which currently sit at the nation’s lowest inventory level (34.02 days), will become a focal point of intense concern. As global petrochemical feedstocks remain exceptionally tight due to the Qatari LNG blockade, household cooking gas prices will likely experience a severe upward adjustment.16

- Power Sector: As seasonal temperatures rise, peak daytime power demand will surge. The Visayas grid will experience its tightest operating margins of the year, pushing the system dangerously close to its first official yellow alerts of the dry season.46

Week 4 (April 27 – May 3, 2026): The Pivot Toward Normalization

If the U.S. military timeline holds, Operation Epic Fury should conclude its primary kinetic phase toward the end of this week, initiating a highly volatile transition period.

- Supply Dynamics: The final emergency delivery of 300,000 barrels of diesel from Oman and Singapore will arrive.27 Despite this, the domestic inventory buffer will likely have eroded from 51 days down to the low 40s, placing immense, immediate pressure on the successful, safe passage of incoming Middle Eastern crude shipments.

- Geopolitics: The Strait of Hormuz will begin a chaotic, largely uncoordinated reopening process. However, the immense backlog of over 150 anchored vessels will take several weeks, if not months, to fully clear.8 Iran’s safe passage guarantees for Philippine ships will be tested in real-time as these vessels attempt to navigate heavily congested and potentially mined corridors.

- Pricing: Global crude markets may exhibit a sudden, sharp downward correction as the geopolitical “war premium” deflates upon the formal cessation of U.S. airstrikes. However, this relief will not immediately reflect at domestic Philippine gasoline pumps due to the inherent 30-to-45-day lag in inventory repricing and the smoothing effect of local pricing formulas.

9.0 Medium-Term Forecast: Monthly Commentary (May – June 2026)

Month 1: May 2026 – The Crucible of Domestic Friction

While geopolitical hostilities in the Persian Gulf may begin to cool, May will represent the absolute peak of localized domestic economic pain for the Philippine populace.

- Power Sector Stress: May will test the physical limits of the Philippine electrical grid. As forecasted by the ICSC, the Visayas grid will almost certainly trigger multiple yellow alerts due to negative operating margins, constrained inter-island HVDC imports, and peak summer air-conditioning demand.46 Consumers nationwide will be hit with the full realization of the projected 16% to 20% electricity rate hikes in their monthly bills.48

- Legislative Intervention: The crushing, simultaneous weight of transport fare hikes and electricity inflation will likely force the national government’s hand. The House Ways and Means Committee’s proposal to suspend excise taxes on fuel products is highly likely to be enacted under emergency powers.35 While the Department of Finance notes this will cost the government roughly PHP 43.3 billion in foregone revenue over a three-month period (and up to PHP 136 billion if extended), it is viewed as a necessary macroeconomic circuit breaker to pull baseline inflation back down toward the 4.0% threshold and prevent widespread civil unrest.35

- Global Logistics: The Strait of Hormuz backlog will slowly, methodically clear. Philippine-bound vessels, utilizing their safe passage diplomatic cover, will begin regular arrivals. This will ease the acute supply panic and begin the slow, capital-intensive process of rebuilding domestic inventories back toward the 60-day strategic target.

Month 2: June 2026 – Structural Repricing and the Second Wave

June marks the critical transition from acute crisis management to confronting the new structural reality of the global economy.

- Supply Security: President Marcos’s early-crisis assurance that crude stocks are sufficient until June 30 will be fulfilled. This success will be primarily attributed to the emergency diesel bridging strategies executed in April, the procurement of Russian Urals by private refiners, and the successful navigation of the Strait via bilateral diplomatic safe passage.21

- The New Pricing Paradigm: Global oil markets will emphatically not return to pre-February 2026 levels. The structural risk of the Persian Gulf has been permanently repriced by global investment banks, establishing a new, significantly higher floor for Brent crude.13 Consequently, Philippine base fuel prices will remain elevated, acting as a permanent drag on GDP growth.

- The Agricultural Second Wave: By June, the catastrophic disruption of fertilizer shipments (urea, ammonia, sulfur) that occurred in March and April will begin to manifest physically in global agricultural yields.8 The Philippines will face severe upward pressure on domestic food prices, particularly rice, as global grain harvests shrink. This will trigger a second, distinct wave of inflation that will challenge the BSP and the national government throughout the second half of 2026, ensuring the economic fallout of the Strait of Hormuz crisis endures well into 2027.

10.0 Strategic Recommendations for National Energy Security Resilience

The 2026 Strait of Hormuz crisis has brutally exposed the systemic, structural vulnerabilities of the Philippine energy sector and its over-reliance on imported, single-source hydrocarbons. To successfully transition the nation from a posture of reactive crisis management to one of long-term strategic resilience, the following initiatives must be prioritized by policymakers:

1. Institutionalize and Accelerate the Sovereign Strategic Petroleum Reserve (SPR): The current crisis highlighted a profound logistical and sovereign failure: the Philippine government lacks its own sovereign storage infrastructure. Consequently, it was forced to rely on the commercial storage tanks of private oil companies to house the emergency procured reserves, complicating sovereign distribution protocols.24 The Philippine National Oil Company (PNOC) must aggressively accelerate its 2026-2028 Strategic Plan to construct state-owned, physically secure, and geographically distributed fuel depots.49 These facilities must be capable of holding a minimum 90-day sovereign reserve of refined diesel, aviation fuel, and LPG, entirely decoupled from private commercial inventories, ensuring the state has direct, unencumbered access to energy during geopolitical blockades.

2. Enact Automatic, Conditional Fuel Excise Tax Suspension Frameworks: To prevent future inflationary spirals from paralyzing the economy, the legislature should transition away from the current system of ad hoc, heavily debated emergency tax suspensions. Congress must codify an automatic, trigger-based statutory framework for the suspension of fuel excise taxes. This mechanism should activate immediately the moment global Brent crude sustains a price above a pre-determined threshold (e.g., $90 per barrel) for a rolling 14-day period. While the Department of Finance notes this risks widening the fiscal deficit, an automatic trigger acts as an immediate macroeconomic circuit breaker, protecting consumer spending power, anchoring inflation expectations, and preempting transport sector strikes before they materialize.35

3. Accelerate Inter-Grid Connectivity and Decentralized Renewable Baseloads: The acute, localized vulnerability of the Visayas grid stems from insufficient local generation and an over-reliance on constrained inter-island HVDC imports from Luzon and Mindanao.47 To mitigate this, the Department of Energy must aggressively fast-track the integration of committed regional renewable energy projects. As highlighted by the World Bank, the Philippines possesses massive, untapped renewable potential.50 The government must incentivize the rapid deployment of utility-scale solar paired with Battery Energy Storage Systems (BESS) directly within the Visayas.46 This localized generation will reduce the grid’s exposure to imported Indonesian coal and the associated maritime shipping cost volatility that currently drives up electricity rates during global shipping crises.

4. Diversify Agricultural Input Supply Chains: Recognizing that global energy chokepoints are intrinsically linked to food security chokepoints, the Department of Agriculture must immediately orchestrate a diversification of its sourcing for urea, ammonia, and phosphate fertilizers, shifting procurement away from the heavily concentrated Persian Gulf.8 Securing long-term, binding supply contracts with North American, North Asian, or establishing domestic synthetic fertilizer production capacity is imperative to insulate the Philippine food basket from future Middle Eastern conflicts and ensure stable crop yields.

11.0 Appendix: Analytical Framework and Source Aggregation

This intelligence assessment was constructed utilizing an exhaustive synthesis of high-fidelity Open Source Intelligence (OSINT), authoritative financial reporting, and sovereign government data available as of April 2, 2026. The methodology relies on a multi-disciplinary analytical framework combining geopolitical event tracking, macroeconomic modeling, and energy supply chain logistics analysis.

Data regarding global oil market movements, structural pricing forecasts, and the physical status of maritime chokepoints were aggregated from leading multinational financial institutions (including Goldman Sachs, J.P. Morgan, and Morgan Stanley) alongside international monitoring bodies (such as the International Energy Agency and the Joint Maritime Information Center).

Domestic Philippine data—including exact inventory levels, emergency procurement volumes, regional grid vulnerabilities, and macroeconomic projections—was sourced directly from official statements and reports by the Department of Energy (DOE), the Bangko Sentral ng Pilipinas (BSP), the Department of Economy, Planning, and Development (DEPDev), and the Institute for Climate and Sustainable Cities (ICSC).

Rigorous analytical methodology was applied to differentiate between the physical flows of raw crude and refined product supply chains. Specific attention was directed toward identifying and modeling second and third-order systemic effects, such as the direct correlation between LNG blockades, regional fertilizer shortages, and subsequent domestic food inflation trajectories. Scenario modeling (Baseline versus Worst-Case) was utilized to provide nuanced, actionable forecasts regarding monetary policy reactions and consumer socioeconomic impacts. Visualizations were purposefully selected to highlight critical data divergences and vulnerabilities, ensuring seamless integration into standardized reporting systems.

Please share the link on Facebook, Forums, with colleagues, etc. Your support is much appreciated and if you have any feedback, please email us in**@*********ps.com. If you’d like to request a report or order a reprint, please click here for the corresponding page to open in new tab.

Sources Used

- 2026 Strait of Hormuz crisis – Wikipedia, accessed April 2, 2026, https://en.wikipedia.org/wiki/2026_Strait_of_Hormuz_crisis

- Crude Chaos: WTI Surges 58% as Trump Extends ‘Operation Epic Fury’ Against Iran, accessed April 2, 2026, http://markets.chroniclejournal.com/chroniclejournal/article/marketminute-2026-4-2-crude-chaos-wti-surges-58-as-trump-extends-operation-epic-fury-against-iran

- Inside Trump’s Search for a Way Out of the Iran War, accessed April 2, 2026, https://time.com/article/2026/04/02/trump-iran-off-ramp/

- Crude Awakening: Brent Slides Toward $100 as Iran De-escalation Deflates the ‘War Premium’, accessed April 2, 2026, https://markets.financialcontent.com/stocks/article/marketminute-2026-4-1-crude-awakening-brent-slides-toward-100-as-iran-de-escalation-deflates-the-war-premium

- Trump Repeats Threats in First Iran War Address, accessed April 2, 2026, https://www.cfr.org/articles/trump-repeats-threats-in-first-iran-war-address

- Iran war’s “core strategic objectives are nearing completion,” Trump says, accessed April 2, 2026, https://www.cbsnews.com/live-updates/iran-war-trump-nato-tehran-threatens-us-tech-companies-strait-of-hormuz/

- Iran War Shipping Update – April 2, 2026, accessed April 2, 2026, https://www.unitedagainstnucleariran.com/blog/iran-war-shipping-update-april-2-2026

- The Blogs: The Chokepoint: If the Strait of Hormuz Stays Shut, Famine Follows, accessed April 2, 2026, https://blogs.timesofisrael.com/the-chokepoint-if-the-strait-of-hormuz-stays-shut-famine-follows/

- Governments Declare Emergency Energy Policies in Response to Iran War, accessed April 2, 2026, https://www.cfr.org/articles/governments-declare-emergency-energy-policies-in-response-to-iran-war

- Iran Update Special Report, March 31, 2026 | ISW, accessed April 2, 2026, https://understandingwar.org/research/middle-east/iran-update-special-report-march-31-2026/

- Secretary-General’s remarks at Press Encounter on the Middle East – the United Nations, accessed April 2, 2026, https://www.un.org/sg/en/content/sg/press-events/2026-04-02/secretary-generals-remarks-press-encounter-the-middle-east

- Are We Approaching an Unprecedented Energy Crisis?, accessed April 2, 2026, https://thedispatch.com/newsletter/dispatch-energy/iran-war-energy-crisis-hormuz/?utm_source=google-news&utm_medium=syndication

- Goldman Sachs reset oil price forecast for the rest of 2026 – TheStreet, accessed April 2, 2026, https://www.thestreet.com/investing/goldman-sachs-reset-oil-price-forecast-for-the-rest-of-2026

- Oil Price Forecast for 2026 | J.P. Morgan Global Research, accessed April 2, 2026, https://www.jpmorgan.com/insights/global-research/commodities/oil-prices

- Oil Market Report – March 2026 – Analysis – IEA, accessed April 2, 2026, https://www.iea.org/reports/oil-market-report-march-2026

- How Much of the World’s Shipping & Oil Goes Through the Strait of Hormuz? 2025 vs 2026 Percentages of Global Supply | Speed Commerce, accessed April 2, 2026, https://www.speedcommerce.com/insights/how-much-of-the-worlds-shipping-goes-through-the-strait-of-hormuz/

- Gov’t urged: Ask Iran to let PH-bound oil tankers pass – News, accessed April 2, 2026, https://newsinfo.inquirer.net/2202995/govt-urged-ask-iran-to-let-ph-bound-oil-tankers-pass

- Oil price shock raises inflation and policy risks in the Philippines | articles | ING THINK, accessed April 2, 2026, https://think.ing.com/articles/oil-price-shock-raises-inflation-and-policy-risks-in-philippines/

- Philippines: Crude oil supply enough to last until June 30, 2026 — says president, accessed April 2, 2026, https://gulfnews.com/business/energy/philippines-crude-oil-supply-to-last-until-june-30-says-marcos-1.500488056

- 2026 Philippine energy crisis – Wikipedia, accessed April 2, 2026, https://en.wikipedia.org/wiki/2026_Philippine_energy_crisis

- Marcos: PH has enough crude oil until June 30, 2026 | GMA News Online, accessed April 2, 2026, https://www.gmanetwork.com/news/topstories/nation/981581/marcos-ph-has-enough-crude-oil-until-june-30-2026/story/

- Marcos: PH crude oil supply enough until June 30 – Manila Bulletin, accessed April 2, 2026, https://mb.com.ph/2026/03/27/marcos-ph-crude-oil-supply-enough-until-june-30

- WATCH: DOE gives updates on PH oil inventory, energy capacity amid Middle East crisis | ANC, accessed April 2, 2026, https://www.youtube.com/watch?v=N89moOUK3Nk

- DOE: PH’s current fuel inventory good for 50.94 days | ABS-CBN News, accessed April 2, 2026, https://www.abs-cbn.com/news/business/2026/3/30/doe-ph-s-current-fuel-inventory-good-for-50-94-days-2223

- PH locks in over a million barrels of diesel | Business 360 | March 30, 2026 – YouTube, accessed April 2, 2026, https://www.youtube.com/watch?v=ruBsf2pn6U0

- Senator calls for early fuel rationing to extend supply, accessed April 2, 2026, https://www.pna.gov.ph/articles/1272239

- DOE: 165.7M Liters of diesel secured through April to strengthen …, accessed April 2, 2026, https://pia.gov.ph/press-release/doe-165-7m-liters-of-diesel-secured-through-april-to-strengthen-national-fuel-supply/

- DOE Launches Strategic Fuel Program, Targets Up to 2M- Barrels Additional Supply, accessed April 2, 2026, https://doe.gov.ph/articles/3380921–doe-launches-strategic-fuel-program-targets-up-to-2m-barrels-additional-supply?title=DOE%20Launches%20Strategic%20Fuel%20Program,%20Targets%20Up%20to%202M-%20Barrels%20Additional%20Supply

- DOE secures 1.04 million barrels of diesel to stabilize April fuel supply, accessed April 2, 2026, https://insiderph.com/doe-secures-104-million-barrels-of-diesel-to-stabilize-april-fuel-supply

- Philippines’ fuel supply extended to nearly 51 days – Philstar.com, accessed April 2, 2026, https://www.philstar.com/headlines/2026/03/31/2518087/philippines-fuel-supply-extended-nearly-51-days

- PH to negotiate safe Strait of Hormuz passage with Iran – Global News, accessed April 2, 2026, https://globalnation.inquirer.net/316385/ph-to-negotiate-safe-hormuz-passage-with-iran

- Iran-Israel war LIVE: De-escalation, return to diplomacy, dialogue …, accessed April 2, 2026, https://www.thehindu.com/news/international/donald-trump-addresses-nation-on-iran-israel-war-live-updates-world-news/article70813995.ece

- Iran’s security council approves 6 Bangladeshi fuel ships to pass Strait of Hormuz, accessed April 2, 2026, https://www.aa.com.tr/en/energy/general/iran-s-security-council-approves-6-bangladeshi-fuel-ships-to-pass-strait-of-hormuz/56053

- Philippines’ businesses hoped to turn the corner in 2026. Then oil prices spiked overnight, accessed April 2, 2026, https://www.businesstimes.com.sg/international/asean/philippines-businesses-hoped-turn-corner-2026-then-oil-prices-spiked-overnight

- Oil shock to bring inflation above 4% | Metrobank Wealth Insights, accessed April 2, 2026, https://wealthinsights.metrobank.com.ph/bworldonline/oil-shock-to-bring-inflation-above-4/

- Go: April rate hike likely amid oil shock – BusinessWorld Online, accessed April 2, 2026, https://www.bworldonline.com/top-stories/2026/03/18/737152/go-april-rate-hike-likely-amid-oil-shock/

- Philippines Gasoline Prices – Trading Economics, accessed April 2, 2026, https://tradingeconomics.com/philippines/gasoline-prices

- OIL PRICE WATCH as of April 1, 2026, accessed April 2, 2026, https://newsinfo.inquirer.net/2204807/oil-price-watch-as-of-april-1-2026

- Oil firms to implement another round of fuel price hike, accessed April 2, 2026, https://www.pna.gov.ph/articles/1272092

- LTFRB announces PUV fare hikes for land transport – Philippine News Agency, accessed April 2, 2026, https://www.pna.gov.ph/articles/1271201

- LTFRB approves fare increase for provincial buses, releases updated fare guide – ABS-CBN, accessed April 2, 2026, https://www.abs-cbn.com/news/business/2026/3/15/ltfrb-approves-fare-increase-for-provincial-buses-releases-updated-fare-guide-1828

- Buses, jeepneys, airport cabs, TNVS get fare hike – News – Inquirer.net, accessed April 2, 2026, https://newsinfo.inquirer.net/2197419/buses-jeepneys-airport-cabs-tnvs-get-fare-hike

- ‘We just asked for a peso’: Transport groups slam fare hike suspension | Philstar.com, accessed April 2, 2026, https://www.philstar.com/headlines/2026/03/19/2515409/we-just-asked-peso-transport-groups-slam-fare-hike-suspension

- How could strait of Hormuz closure affect UK food and medicine supplies?, accessed April 2, 2026, https://www.theguardian.com/world/2026/apr/02/strait-of-hormuz-iran-closure-uk-food-medicine-supplies

- Philippine power supply for Q2 2026 remains sufficient, but thin reserves leave grid at risk amid demand surge and plant outages, accessed April 2, 2026, https://icsc.ngo/philippine-power-supply-for-q2-2026-remains-sufficient-but-thin-reserves-leave-grid-at-risk-amid-demand-surge-and-plant-outages/

- Electricity supply looks ‘sufficient’ for summer months–ICSC, accessed April 2, 2026, https://business.inquirer.net/581497/local-electricity-supply-looks-sufficient-for-summer-months-icsc

- PH power outlook for April to June 2026 manageable but fragile — ICSC – GMA Network, accessed April 2, 2026, https://www.gmanetwork.com/news/money/economy/981195/ph-power-outlook-april-june-2026/story/

- Rise in power rates could be as high as 16%, may be felt by April – DOE | ANC – YouTube, accessed April 2, 2026, https://www.youtube.com/watch?v=BL2vokpNNcU

- PNOC Lays Out Strategic Priorities and Financial Plans for 2026-2028, accessed April 2, 2026, https://www.pnoc.com.ph/pnoc-lays-out-strategic-priorities-and-financial-plans-for-2026-2028/

- The Iran War Is Reshaping Asia’s Energy Security Strategies, accessed April 2, 2026, https://www.cfr.org/articles/the-iran-war-is-reshaping-asias-energy-security-strategies