1. Executive Summary

The global commercial nuclear energy sector currently occupies a critical nexus of climate imperatives, national security, and complex techno-economic realities. As nation-states pursue rapid decarbonization alongside sovereign energy independence, nuclear power—uniquely capable of providing high-density, reliable baseload electricity without carbon emissions—is undergoing a profound strategic reassessment globally. This document provides an exhaustive intelligence and economic analysis of the worldwide commercial nuclear power fleet designed to provide electricity to national power grids. The analysis synthesizes operating statuses, power outputs, capital cost economics, life extension methodologies, and the geopolitical vulnerabilities inherent within the nuclear fuel cycle.

Currently, the global operating fleet consists of 415 commercial nuclear reactors, which collectively generate approximately 379,471 megawatts (MW) of net electrical capacity.1 These facilities provide nearly ten percent of global electricity and represent a quarter of all low-carbon power generation worldwide.3 However, the geographic distribution of this capability is undergoing a historic shift. While the United States and France maintain the oldest and largest fleets by capacity, the momentum for new construction has decisively moved eastward. Of the 78 reactors currently under construction globally, the vast majority are located in Asia—driven largely by the People’s Republic of China—and deployed internationally through aggressive export strategies by the Russian Federation.5

The economics of nuclear power present a stark international dichotomy. In state-directed economies, standardized build programs have successfully driven overnight construction costs down to approximately $2,341 per kilowatt (kW).7 Conversely, Western projects are plagued by first-of-a-kind premiums, regulatory bottlenecks, and a generational loss of supply chain expertise. This has led to immense budget overruns, exemplified by the United Kingdom’s Hinkley Point C project, which is now estimated to cost up to £48 billion.8 Consequently, Western nations are increasingly prioritizing the lifetime extension of existing assets—pushing operational limits to 60 or 80 years—and pursuing the unprecedented strategy of restarting decommissioned or mothballed reactors, such as the Palisades plant and Three Mile Island Unit 1 in the United States.10

Furthermore, this report investigates the significant geopolitical risks embedded in the nuclear supply chain. The global reliance on Russia’s State Atomic Energy Corporation (Rosatom) and its subsidiary Tenex for uranium conversion, enrichment, and High-Assay Low-Enriched Uranium (HALEU) presents an acute vulnerability.13 As the world navigates the transition to net-zero emissions, the future of nuclear power will depend not only on overcoming exorbitant capital costs and technical aging challenges but also on successfully decoupling critical supply chains from adversarial state actors.

2. The Global Operating Fleet: Capacity, Topography, and Performance

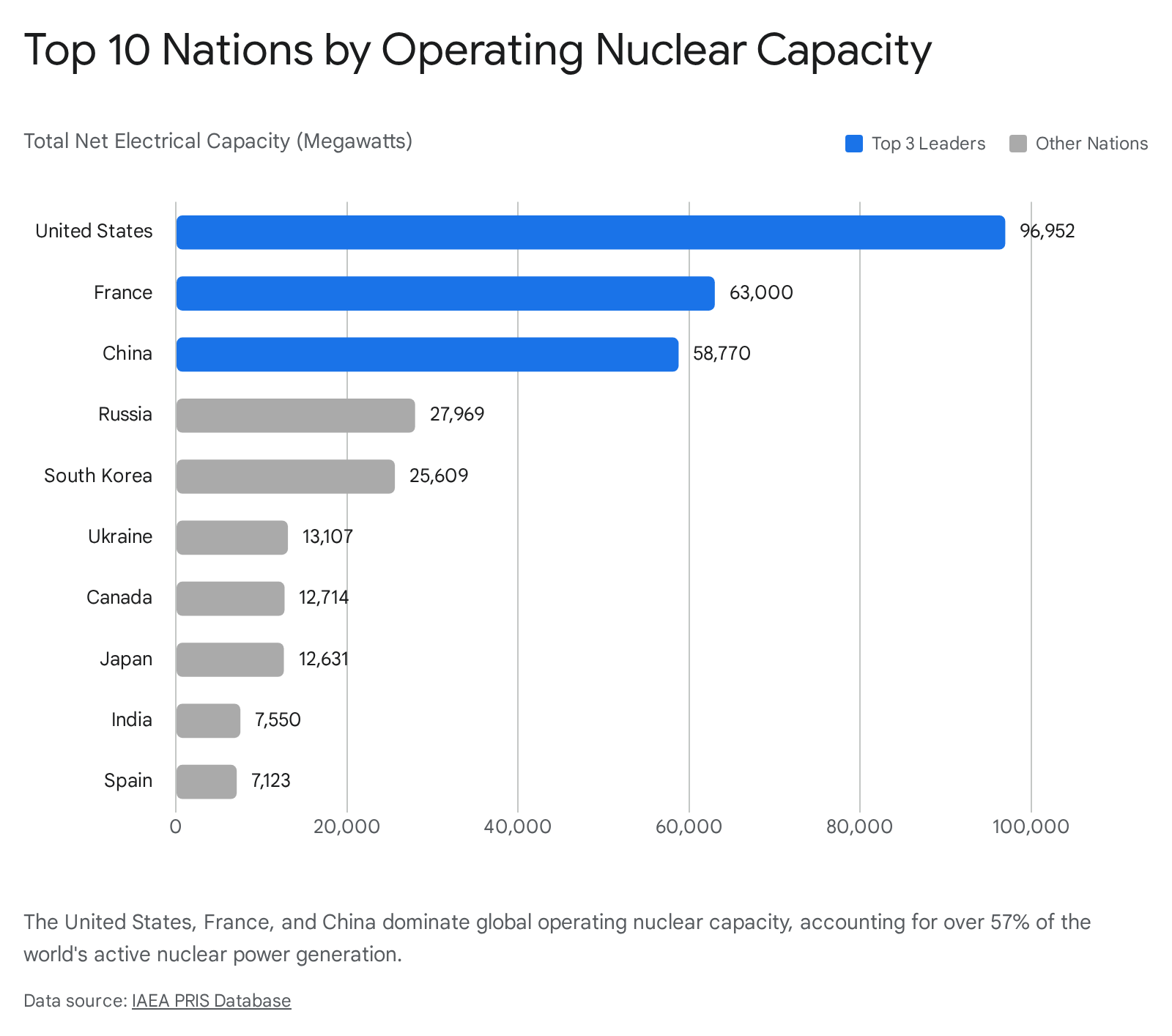

The International Atomic Energy Agency’s (IAEA) Power Reactor Information System (PRIS) database remains the most authoritative and comprehensive repository for global nuclear infrastructure data, tracking reactor status, performance, and energy availability since 1970.15 As of mid-2025, the world operates 415 nuclear reactors dedicated to supplying electricity to national grids, representing a total net electrical capacity of 379,471 MW.1

2.1 Geographic Distribution of Operating Capacity

The global distribution of nuclear power is highly concentrated among advanced industrial economies and rapidly developing nations. The United States maintains the largest operational fleet, though it is characterized by aging infrastructure and a historical dearth of recent deployments. China is rapidly closing this gap, maintaining an aggressive build schedule that outpaces all other nations combined. The table below provides a comprehensive breakdown of the world’s operational nuclear fleet by country, detailing the number of active reactors and their total net electrical capacity.2

| Country / Territory | Number of Operating Reactors | Total Net Electrical Capacity (MW) | Share of Global Capacity (%) |

| United States of America | 94 | 96,952 | 25.55 |

| France | 57 | 63,000 | 16.60 |

| China | 60 | 58,770 | 15.49 |

| Russia | 34 | 27,969 | 7.37 |

| Republic of Korea (South Korea) | 26 | 25,609 | 6.75 |

| Ukraine | 15 | 13,107 | 3.45 |

| Canada | 17 | 12,714 | 3.35 |

| Japan | 14 | 12,631 | 3.33 |

| India | 21 | 7,550 | 1.99 |

| Spain | 7 | 7,123 | 1.88 |

| Sweden | 6 | 7,008 | 1.85 |

| United Kingdom | 9 | 5,883 | 1.55 |

| United Arab Emirates | 4 | 5,348 | 1.41 |

| Finland | 5 | 4,369 | 1.15 |

| Czech Republic | 6 | 3,963 | 1.04 |

| Pakistan | 6 | 3,262 | 0.86 |

| Switzerland | 4 | 2,973 | 0.78 |

| Slovakia | 5 | 2,302 | 0.61 |

| Belarus | 2 | 2,220 | 0.59 |

| Belgium | 2 | 2,056 | 0.54 |

| Bulgaria | 2 | 2,006 | 0.53 |

| Hungary | 4 | 1,916 | 0.50 |

| Brazil | 2 | 1,884 | 0.50 |

| South Africa | 2 | 1,854 | 0.49 |

| Argentina | 3 | 1,641 | 0.43 |

| Mexico | 2 | 1,552 | 0.41 |

| Romania | 2 | 1,300 | 0.34 |

| Islamic Republic of Iran | 1 | 915 | 0.24 |

| Slovenia | 1 | 696 | 0.18 |

| Netherlands | 1 | 482 | 0.13 |

| Armenia | 1 | 416 | 0.11 |

| Total | 415 | 379,471 | 100.00 |

The proportion of total electricity demand met by nuclear power varies drastically by jurisdiction. In the United States, nuclear power supplied 781,979 gigawatt-hours (GWh) in 2024, representing approximately 18.2% of the nation’s total electricity production.17 This share has remained relatively stable over the past two decades, hovering between 18% and 20%.17 Conversely, France derives over 70% of its electrical power from its nuclear fleet, underscoring a distinct national energy security strategy formulated in the late twentieth century.18

2.2 Reactor Technology Topography

The technological foundation of the global fleet is overwhelmingly dominated by Light-Water Reactors (LWRs). Specifically, Pressurized Light-Water Moderated and Cooled Reactors (PWRs) form the absolute core of the industry standard. There are 308 operational PWR units worldwide, generating 297,631 MW of total capacity.1 The design preference for PWRs stems from their inherent physical stability, the critical separation of the primary radioactive coolant loop from the secondary steam generation loop, and decades of extensive historical operating data that inform modern safety and maintenance protocols.

Boiling Light-Water Cooled and Moderated Reactors (BWRs) comprise the second-largest technological contingent, with 43 reactors currently generating 44,720 MW.1 Pressurized Heavy-Water Moderated and Cooled Reactors (PHWRs), which are prominently utilized in Canada and India and often recognized internationally as CANDU-type designs, total 46 units providing 24,430 MW.1 The PHWR design allows for the use of unenriched natural uranium, circumventing the need for complex and strategically sensitive enrichment supply chains.

Legacy and experimental technologies hold a much smaller market share. The Light-Water Cooled, Graphite Moderated Reactor (LWGR, which includes the Soviet-era RBMK design) accounts for 7 operational units providing 6,475 MW.1 Gas-Cooled, Graphite Moderated Reactors (GCR) comprise 8 units generating 4,685 MW, while Fast Breeder Reactors (FBR) remain largely experimental or limited in commercial scope, with only two units operational globally, contributing 1,380 MW.1 Furthermore, there is currently one High Temperature Gas Cooled Reactor (HTGR) generating 150 MW.1

2.3 Operational Performance and Load Factors

Modern nuclear reactors operate with exceptional efficiency and uptime. The median capacity factor for the global fleet operates at nearly 88 percent.3 A review of the top-performing reactors by load factor in 2024 demonstrates that rigorous maintenance and operational excellence can yield load factors exceeding 100 percent of nominal nameplate capacity through uprating and optimized thermal efficiencies. Russian and American reactors heavily populate the highest performance tiers. For instance, Russia’s Balakovo 4 (a 950 MW VVER V-320 PWR) achieved a 108.60 load factor, closely followed by the United States’ Turkey Point 4 (an 821 MW PWR) at 106.40, and Russia’s Kalinin 2 at 106.10.5 Japan’s Takahama 3, a pressurized water reactor, demonstrated a 105.80 load factor, highlighting post-Fukushima operational resilience.5

In terms of absolute electricity generation, the newest generation of high-capacity reactors dominates. China’s Taishan 1 (an EPR-1750 PWR) is projected to generate 12.7 TWh in 2025, while South Korea’s Saeul 1 (an APR-1400 PWR) follows closely at 11.8 TWh, and the United States’ Palo Verde 1 at 11.7 TWh.5 Historically, cumulative generation records are held by aging but highly optimized Western plants, with the U.S. Peach Bottom 2 and 3 boiling water reactors leading global lifetime generation figures at nearly 400 TWh each.5

3. The Economics of Nuclear Energy: Capital Deployment and LCOE

The economic viability of commercial nuclear power is severely front-loaded, making it highly sensitive to macroeconomic financing conditions. Capital expenditures—encompassing the overnight construction cost (OCC), financing costs accrued during the lengthy multi-year build period, and project management—account for the vast majority of the Levelized Cost of Energy (LCOE) over the plant’s operational life. Effective modeling of global energy markets requires a nuanced understanding of how these costs fluctuate based on jurisdiction, regulatory environment, and supply chain maturity.19

3.1 Divergent Overnight Construction Costs

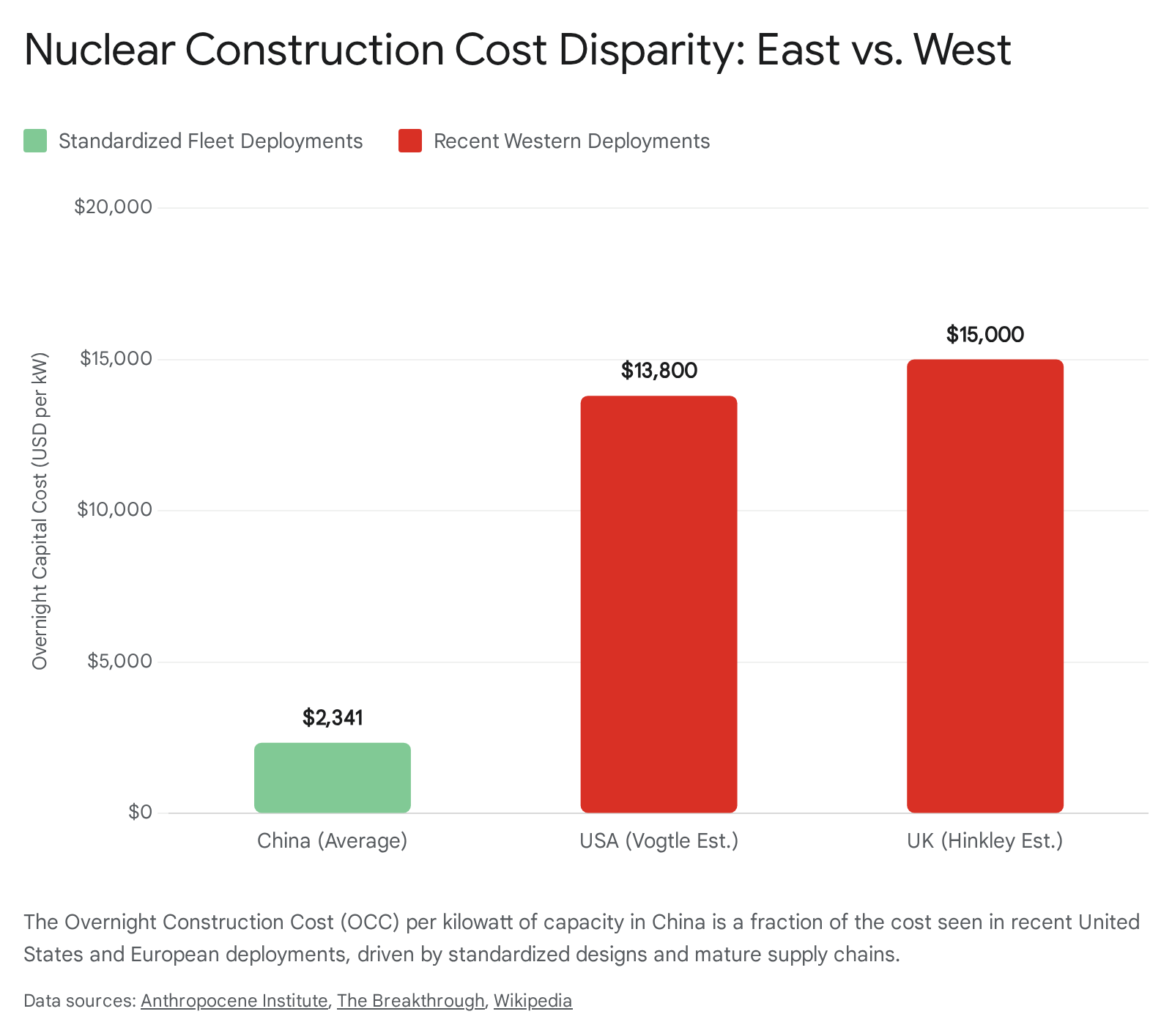

The overnight cost to build a nuclear reactor varies wildly depending on the regulatory environment, localized labor costs, and the degree of design standardization. A deep dive into Chinese nuclear economics reveals unparalleled cost efficiency driven by state planning. The total investment for the 55 operational reactors in China amounted to roughly 841 billion CNY, yielding a unit cost of 14,755 CNY/kW (approximately $2,230 USD/kW).7 When factoring in reactors currently under construction and those approved for near-term deployment, the estimated unit cost rises only slightly to 15,873 CNY/kW ($2,341 USD/kW).7 Furthermore, construction durations in China average an incredibly swift 74 months, significantly mitigating the accrual of financing interest.7 Chinese operating costs are equally optimized, estimated to range between $0.03 and $0.04 USD/kWh.7

By stark contrast, the atrophied nuclear supply chain in the West leads to crippling First-of-a-Kind (FOAK) premiums. Data regarding the AP1000 and European Pressurized Water Reactor (EPR) deployments suggest that slower concrete installation rates, stringent regulatory redesigns mid-construction, and the loss of experienced metallurgical tradespeople have exponentially driven up costs.20 Flowline chart analyses indicate that delays in Western projects are predominantly rooted in fundamentally slower civil engineering and concrete installation rates compared to South Korean and Chinese deployments.20

3.2 Discount Rates and Financial Engineering

Because nuclear megaprojects require billions in upfront capital and take up to a decade to yield initial revenue, the cost of capital—expressed through the discount rate or Weighted Average Cost of Capital (WACC)—is the primary determinant of the final Levelized Cost of Energy. At a 3% discount rate, which implies heavy state subsidization or sovereign loan guarantees, nuclear power is highly competitive with natural gas and coal globally. For instance, at a 3% discount rate, the estimated cost of nuclear energy in the United States is $43.9/MWh, while in China it is $49.9/MWh, and in Russia, it falls to an astonishing $27.4/MWh.21

However, at a 7% or 10% discount rate—which is highly typical of private equity or Western financial markets evaluating high-risk infrastructure projects—the LCOE nearly doubles. At a 7% discount rate, the U.S. LCOE rises to $71.3/MWh, and at 10%, it surges to $98.6/MWh.21 This financial reality renders private nuclear development uncompetitive in deregulated markets without heavy state subsidies or guaranteed strike prices. This dynamic necessitates financial mechanisms such as the Contract for Difference (CfD), utilized to secure the UK’s Hinkley Point C project and recently approved by the European Commission for Poland’s planned AP1000 units to guarantee revenue stability over 40 years.22

4. The Global Pipeline: Reactors Under Construction

The global construction pipeline reveals a pronounced macroeconomic and geopolitical shift. There are currently 78 nuclear reactors under construction worldwide, representing a total net capacity of 78,986 MWe.5 The locus of nuclear expansion is overwhelmingly concentrated in Asia and executed through Russian-led export projects. Over the last five years, of the 52 reactors that commenced construction globally, 25 were of Chinese design and 23 were of Russian origin.6

4.1 Detailed Status of Active Megaprojects

The table below outlines a comprehensive selection of the most critical reactors currently under construction globally, prioritizing those with recent grid connections, upcoming expected startup dates, and the newest generation of heavy-capacity builds.5

| Reactor Name | Location | Reactor Model | Net Capacity (MWe) | Expected Startup / Grid Connection |

| San’ao 1 | China | Hualong One (PWR) | 1117 | March 2026 |

| Taipingling 1 | China | Hualong One (PWR) | 1116 | February 2026 |

| Kursk 2-1 | Russia | VVER-TOI (PWR) | 1200 | December 2025 |

| Zhangzhou 2 | China | Hualong One (PWR) | 1126 | November 2025 |

| Rajasthan 7 | India | PHWR | 630 | March 2025 |

| Flamanville 3 | France | EPR (PWR) | 1630 | December 2024 |

| Zhangzhou 1 | China | Hualong One (PWR) | 1126 | November 2024 |

| Shidaowan Guohe One 1 | China | CAP1400 (PWR) | 1400 | October 2024 |

| Fangchenggang 4 | China | HPR1000 (PWR) | 1105 | April 2024 |

| Barakah 4 | United Arab Emirates | APR-1400 (PWR) | 1337 | March 2024 |

| Akkuyu 1 | Turkey | VVER-1200 (PWR) | 1114 | Late 2025 / 2026 |

| Rooppur 1 | Bangladesh | VVER-1200 (PWR) | 1200 | 2025 |

| Hinkley Point C (Unit 1) | United Kingdom | EPR (PWR) | 1630 | 2030 (Estimated) |

| El Dabaa 4 | Egypt | VVER-1200 (PWR) | 1200 | 2031 (Estimated) |

| Paks II-1 | Hungary | VVER-1200 (PWR) | 1100 | Under Construction |

4.2 Chinese Domestic Build and Standardization

China is executing the most aggressive and successful nuclear expansion program in human history. The nation’s strategy relies heavily on standardized domestic designs, primarily the Generation III+ Hualong One (HPR1000) and the CAP1400.5 By avoiding the bespoke, site-specific engineering changes that historically plague Western builds, China benefits from massive economies of scale and rapid learning curves. The Chinese pipeline includes a massive wave of new starts scheduled for late 2025 and early 2026, including Xuwei 1, Bailong 1, Lufeng 2, Ningde 6, San’ao 3, and Zhaoyuan 1, all boasting capacities exceeding 1100 MWe.5

4.3 Russian Exports and Geopolitical Integration

The Russian Federation, executed via its state-owned enterprise Rosatom, is the world’s undisputed leader in nuclear technology exports. Russia utilizes nuclear power plant construction as a primary tool of geopolitical statecraft, offering comprehensive financing, construction, and lifetime fuel supply packages to developing nations.18

- Akkuyu Nuclear Power Plant (Turkey): This project involves four VVER-1200 units totaling over 4,400 MWe.5 With an estimated cost of $24 to $25 billion, it is a flagship Build-Own-Operate model for Rosatom.24 The project has injected over $11 billion into the Turkish economy, and the first unit is expected to achieve full operational status in 2026.24

- El Dabaa (Egypt): Egypt is progressing with the construction of four 1.2 GWe VVER-1200 reactors in deep cooperation with Russia, with the facility expected to be fully operational by the end of 2031.26

- Rooppur (Bangladesh): Two VVER-1200 units are under construction with an estimated cost of $12.65 billion.28 The project is currently suffering from delays, resulting in significant daily interest penalties owed to Russia and pushing the Levelized Cost of Energy higher than initially modeled.29

4.4 Western Construction: Delays and Financial Hemorrhaging

In stark contrast to the rapid deployment in the East, the United States and Europe have faced severe, existential challenges in revitalizing their nuclear supply chains. The deployment of “Generation III+” reactors—such as the Westinghouse AP1000 and the French EPR—was originally intended to simplify construction through modularity and passive safety systems.31 Instead, these projects have been characterized by catastrophic schedule delays and cost inflation.

The Vogtle Units 3 and 4 in the United States took 15 years to build and cost $31 billion, approximately $17 billion over the initial budget, illustrating the extreme difficulty of executing first-of-a-kind designs with an inexperienced workforce.10 Similarly, the Hinkley Point C project in the United Kingdom, consisting of two EPR units, was originally estimated to cost £18 billion in 2015 prices with a 2025 completion date.8 Systemic project management failures, stringent regulatory interventions, and a loss of specialized trades have driven current forecasts to a staggering £35 billion in 2015 prices (approximately £48 billion in 2026 prices), with unit 1 delayed until at least 2030.8

5. Aging Fleets, Material Degradation, and Plant Life Extensions

The lack of new builds in the West over the past three decades has resulted in an increasingly geriatric nuclear fleet. As of 2023, the average age of an operating reactor globally was 31 years.32 The United States operates the oldest fleet (average age 41 years), followed closely by France (36 years).32 Consequently, utility companies and safety regulators are intensely focused on Long-Term Operation (LTO) through rigorous license extensions.

5.1 Regulatory Frameworks for Extension

In the United States, the Nuclear Regulatory Commission (NRC) originally licensed plants for 40 years of operation. To date, 88 of America’s 92 operational reactors have received initial 20-year extensions, pushing their operational life to 60 years.12 Driven by the Department of Energy’s Light Water Reactor Sustainability (LWRS) program, which has provided a decade of material research, utilities are now seeking Subsequent License Renewals (SLR) for an additional 20 years. This action would bring the total operational life of these assets to 80 years, effectively keeping a quarter of the U.S. fleet online beyond 2050.12

In France, operating licenses are not strictly time-limited at issuance but are subject to comprehensive decennial safety reviews by the Autorité de Sûreté Nucléaire (ASN).33 The “fourth periodic safety review” (PSR4) is currently evaluating the 900 MWe and 1300 MWe fleets for operation beyond their initial 40-year design life.34 The ASN mandates that extending operations must aim for the best modern safety standards, including resilience against climate change impacts. In August 2023, Tricastin 1 became the first French reactor approved to operate past 40 years, setting a precedent for the entire national fleet.35

5.2 Technical Risks: Embrittlement and Stress Corrosion Cracking

Extending reactor lifespans to 60 or 80 years is not merely an administrative hurdle; it requires navigating severe material degradation under extreme thermal, mechanical, and radiological stresses over decades.

- Neutron Embrittlement: Inside the Reactor Pressure Vessel (RPV)—the thick steel container holding the nuclear fuel—high-energy neutrons bombard the steel structure continuously.37 Over decades, these subatomic impacts alter the crystalline structure of the steel, significantly reducing its ductility and fracture toughness.37 This “embrittlement” is particularly critical in Pressurized Water Reactors. In an accident scenario known as Pressurized Thermal Shock (PTS), where cold emergency water is injected into a hot, pressurized vessel, the rapid thermal stress could potentially fracture the embrittled steel, compromising the primary containment barrier.37 Regulators enforce strict monitoring via Appendix H material surveillance programs to ensure the vessel steel retains adequate safety margins.37

- Intergranular Stress Corrosion Cracking (IGSCC): High operational stresses combined with a highly corrosive, high-temperature water environment cause critical internal metallic components to crack and fail, sometimes with little warning.38 Advanced metallurgical research indicates that nanoscale mismatches between adjacent crystals in polycrystalline alloys create weak regions that alter electronic properties, accelerating oxygen reactions and chemical attacks.38 Managing IGSCC requires continuous non-destructive evaluation, advanced noble chemical water chemistry controls, and the eventual, highly expensive replacement of massive components like steam generators.38

6. Permanently Shut Down and Phased-Out Reactors

Globally, over 200 commercial reactors have been permanently shut down. While the mean age of closure for units taken offline between 2020 and 2024 was just 43.2 years, the primary drivers for these closures are rarely absolute technical exhaustion.41 Instead, they are overwhelmingly driven by shifting political mandates and unfavorable localized economic conditions.32

6.1 Catastrophic Failures and Economic Closures

A subset of global reactors was permanently shuttered due to severe technical failures or catastrophic accidents. Notable examples include:

- Chernobyl 4 (Ukraine): Destroyed in April 1986 due to a fire and complete meltdown.42

- Three Mile Island 2 (USA): Shut down in March 1979 following a severe partial core melt.42

- Fukushima Daiichi 1-4 (Japan): Destroyed in 2011 by core melts resulting from cooling loss and subsequent hydrogen explosion damage following a tsunami.42

- Vandellos 1 (Spain): Shut down in mid-1990 following a severe turbine fire.42

- Bohunice A1 (Slovakia): Closed in 1977 due to core damage resulting from a fueling error.42

- St Lucens (Switzerland): Shut down in 1966 due to a core melt.42

- Monju (Japan): A prototype fast neutron reactor permanently closed in 2016 following persistent sodium leaks.42

In deregulated energy markets, particularly in the United States, nuclear plants have historically struggled to compete with cheap natural gas and subsidized renewable energy. Numerous fully functional U.S. plants—such as San Onofre 1, 2, and 3, Fort Calhoun, and Rancho Seco 1—were shuttered prematurely simply because they were operating at a financial loss.43

6.2 Policy-Driven Phase-Outs: Germany and Japan

Following the 1986 Chernobyl disaster and the 2011 Fukushima Daiichi accident, intense public opposition catalyzed aggressive, state-mandated phase-out policies in several technologically advanced nations.44

Germany historically generated a quarter of its electricity from 17 operational reactors.45 In the immediate aftermath of Fukushima, Angela Merkel’s government passed the 13th amendment to the Nuclear Power Act, forcing eight units to close immediately.45 The remaining units (including Brokdorf, Grohnde, Gundremmingen C, Emsland, Isar 2, and Neckarwestheim 2) were systematically phased out, culminating in the total eradication of German nuclear power on April 15, 2023.45

Similarly, Japan possesses 33 reactors classified as technically “operable,” yet the vast majority have remained in long-term outage since 2011 as they undergo grueling post-Fukushima safety retrofits and navigate highly contentious local political approvals for restart.41 The emissions impact of these political closures has been severe. Macroeconomic health studies conclude that retaining the German and Japanese fleets between 2011 and 2017 could have prevented the emission of 2,400 Megatons of carbon dioxide and averted 28,000 air pollution-induced deaths that resulted from the substitute burning of coal and natural gas.44

7. Cancelled and Never Completed Megaprojects

The history of the commercial nuclear industry is littered with partially built, multi-billion-dollar monuments to shifting geopolitical winds, financial collapse, and regulatory paralysis. Analyzing these abandoned megaprojects provides crucial risk intelligence for modern infrastructure planning. The table below highlights significant cancelled global nuclear projects, followed by detailed case analyses.

| Project Name | Location | Planned Capacity | Status | Year Cancelled / Suspended | Primary Reason for Cancellation |

| Juragua | Cuba | 2 x 440 MW | Abandoned | 1992 (Suspended), 2000 (Abandoned) | Soviet collapse, lack of funding, U.S. embargo 48 |

| Bellefonte | USA | 2 x 1256 MW | Cancelled | 1988 (Suspended), 2021 (Permits Expired) | Falling energy demand, massive debt, shifting economics 49 |

| Bataan | Philippines | 1 x 621 MW | Mothballed | 1986 | Political corruption allegations, post-Chernobyl safety fears 50 |

| Zarnowiec | Poland | 4 x 440 MW | Cancelled | 1990 | Post-Soviet economic changes, public opposition post-Chernobyl 51 |

| Stendal | Germany | 4 x 1000 MW | Cancelled | 1990/1991 | German reunification, economic restructuring 52 |

7.1 The Juragua Nuclear Power Plant (Cuba)

Initiated in 1976 as a premier symbol of Soviet-Cuban strategic cooperation, the Juragua plant was designed to house two VVER-440 V318 reactors, intended to supply over 15% of Cuba’s electricity and sever its reliance on imported oil.48 Construction commenced in 1983 under the supervision of Fidel Castro Díaz-Balart.48 By the time construction was suspended in 1992, the first reactor’s civil structure was estimated to be 90% to 97% complete, though only 37% of the mechanical equipment was actually installed.48

The immediate reason for failure was the collapse of the Soviet Union, which severed the economic lifeline funding the project.48 The Russian Federation demanded hard currency on commercial terms to finish the work, which the Cuban government could not afford—highlighted by its inability to pay Siemens $21 million for critical instrumentation and control equipment.48 Furthermore, the project was plagued by severe safety controversies. Defected Cuban technicians testified to the U.S. Congress that 10% to 15% of the 5,000 inspected civil welds were deeply defective, and that operators were being trained on inadequate simulators that did not reflect the actual reactor design.48 Attempts to restart the project in the late 1990s were blocked by the U.S. Helms-Burton Act, and in 2000, Vladimir Putin and Fidel Castro officially agreed to abandon the site.48 Today, Juragua remains a decaying, skeletal structure alongside the partially inhabited workers’ town, Ciudad Nuclear, with its primary turbine having been scavenged in 2004 to repair a fossil-fuel plant.48

7.2 The Bellefonte Nuclear Generating Station (USA)

Owned by the Tennessee Valley Authority (TVA), the Bellefonte project was envisioned in 1975 to house two massive Babcock & Wilcox pressurized water reactors.49 After sinking $6 billion into the project over a decade, the TVA suspended construction in 1988.49 At that time, Unit 1 was considered 88% complete and Unit 2 was 58% complete.49

The project fell victim to a combination of falling electricity demand, changing regulatory requirements following the Three Mile Island accident, and immense overarching financial burdens on the TVA.49 Over the subsequent decades, the TVA systematically stripped the plant of valuable components—selling off steam generators, massive pumps, and condenser tubes to serve as spares for other facilities.49 This asset recovery effort reduced the actual completion status of the units to roughly 55% and 35%, respectively.49 In 2016, Nuclear Development LLC attempted to purchase the site at auction for $111 million, intending to invest an additional $13 billion to finish the reactors.49 However, the TVA pulled out of the agreement, the courts ruled in the TVA’s favor, and the construction permits officially expired in October 2021, permanently terminating the site’s nuclear prospects.49

7.3 Bataan Nuclear Power Plant (Philippines)

Completed in 1984 at a cost exceeding $2 billion, the 621-MW Westinghouse PWR at Bataan is historically unique in that it was fully built but never fueled or commissioned for operation.50 The plant was abruptly mothballed due to immense public outcry over safety—specifically its proximity to geological fault lines and volcanoes—amplified by the global panic following the 1986 Chernobyl disaster.50 Furthermore, the project was deeply entangled in allegations of massive corruption under the dictatorship of Ferdinand Marcos Sr..50 For forty years, the plant has remained an expensive, non-producing monument, maintained solely on care-and-maintenance budgets.54

7.4 European Cancellations: Zarnowiec and Stendal

The collapse of the Eastern Bloc resulted in the immediate termination of several massive nuclear infrastructure projects.

- Zarnowiec (Poland): Construction began in 1982 on four VVER-440 reactors intended to be Poland’s first nuclear power station.51 The project was officially cancelled in September 1990 due to extreme economic instability in post-Soviet Poland, though the psychological impact and public opposition stemming from the Chernobyl disaster played a definitive role in the political decision.51 The unfinished remains sit abandoned, though the general geographic region is now being prepared for Poland’s modern AP1000 builds.55

- Stendal (Germany): Intended to be the largest nuclear power plant in central Europe with a planned output of 4,000 MW, construction on the VVER-1000 units halted in 1990 following German reunification.52 The custom-built reactor pressure vessels were cut up and scrapped, and the three completed cooling towers were demolished with explosives in 1999.52 The vast site, which once employed 13,000 workers, has since been converted into an industrial estate.52

8. The Feasibility and Economics of Restarting Dormant Plants

In a stunning reversal of historical energy trends, the intersection of aggressive net-zero emissions targets and the explosive electricity demand generated by artificial intelligence data centers has catalyzed serious efforts to resurrect permanently closed or mothballed nuclear power plants.10 Restarting a retired reactor is increasingly viewed by private capital as an economically superior, lower-risk alternative to navigating the extreme FOAK risks and multi-decade timelines of building new advanced reactors.10

8.1 The American Vanguard: Palisades and Three Mile Island

The Palisades plant in Michigan, shut down in May 2022 purely for economic reasons and subsequently sold to Holtec International for tear-down, is now the pioneer of the global restart movement.10 Supported by a massive $1.5 billion loan from the Department of Energy and strong state-level backing from the Michigan government, Holtec has pivoted entirely to relicensing the plant, with a projected restart timeline of at least three years.10

Similarly, Three Mile Island Unit 1 in Pennsylvania is under active evaluation for a restart.10 Unlike Unit 2, Unit 1 operated safely and efficiently as a highly reliable performer until its premature economic closure in 2019.10 Constellation Energy is actively negotiating with the state government and hyperscalers (such as Microsoft) to fund the restart via long-term, premium-priced Power Purchase Agreements (PPAs) designed specifically to supply carbon-free, 24/7 power to data centers.6

8.2 International Restart Feasibility: Bataan and Germany

Internationally, the feasibility of recommissioning dormant plants is gaining intense political traction. In the Philippines, the government is actively evaluating a restart of the 40-year-old Bataan plant.50 In 2024, the Department of Energy commissioned Korea Hydro & Nuclear Power (KHNP) to conduct a comprehensive, two-phase technical and economic feasibility study to determine if the 1980s-era structural and mechanical systems can be safely refurbished, upgraded, and brought online to meet the nation’s severe energy shortages.54

In Germany, despite the political finality of the April 2023 phase-out, the technical reality is that the recently closed reactors remain highly functional, world-class assets. The German nuclear technology association (KernD) assesses that up to six reactors (including Emsland, Isar 2, and Grohnde) could technically resume operation between 2028 and 2032 if the political will existed.46 Proponents argue that a restart would preserve 5,000 high-paying technical jobs and drastically cut the emissions currently generated by replacement coal and gas power.47 However, reversing the phase-out would require amending the Atomic Energy Act via a majority vote in the Bundestag—a move that remains politically fraught, despite gaining traction among industrial sectors facing crippling energy costs.47

8.3 Systemic Hurdles to Recommissioning

While economically advantageous compared to new greenfield builds, restarting a mothballed plant presents immense, unprecedented logistical challenges:

- Regulatory Precedent and Licensing: Reactor operating licenses are not simple certificates; they encompass thousands of pages of technical specifications, inspection intervals, and testing procedures.10 Re-licensing a dismantled plant requires proving the continuous operability and structural integrity of millions of aging components to safety regulators—a process with virtually no established regulatory precedent.10

- Human Capital Attrition: Specialized nuclear operators hold strict licenses specific to single reactor units.10 When plants close, the highly trained workforce disperses to other industries. Rebuilding, training, and certifying a new operational workforce to safely run a legacy reactor takes years and significant capital investment.10

- Deferred Maintenance and Supply Chains: Plants scheduled for retirement strategically cease major capital upgrades and preventative maintenance years in advance of their closure date to save money.10 The new operator inherits a massive, complex maintenance backlog. Furthermore, securing the specific, highly engineered nuclear fuel assemblies required to run the reactor is a multi-month, highly constrained procurement process.10

9. Geopolitical Risks and Supply Chain Vulnerabilities

The global push to expand and extend commercial nuclear energy is occurring within a deeply fractured and increasingly hostile geopolitical environment. The Western world’s nuclear supply chain has severely atrophied over the past thirty years, resulting in a dangerous, systemic dependency on the Russian Federation for the most critical elements of the nuclear fuel cycle.

9.1 The Rosatom Stranglehold on the Fuel Cycle

Russia’s Rosatom is not merely an exporter of physical reactors; it exerts hegemonic control over critical chokepoints in the global nuclear fuel supply chain. To produce functional nuclear fuel, raw natural uranium must be mined, milled into uranium-oxide (), converted into a gaseous state known as uranium-hexafluoride (), and then enriched via highly complex gas centrifuges into Low-Enriched Uranium (LEU).61Russia’s Rosatom is not merely an exporter of physical reactors; it exerts hegemonic control over critical chokepoints in the global nuclear fuel supply chain. To produce functional nuclear fuel, raw natural uranium must be mined, milled into uranium-oxide (), converted into a gaseous state known as uranium-hexafluoride (), and then enriched via highly complex gas centrifuges into Low-Enriched Uranium (LEU).61Russia’s Rosatom is not merely an exporter of physical reactors; it exerts hegemonic control over critical chokepoints in the global nuclear fuel supply chain. To produce functional nuclear fuel, raw natural uranium must be mined, milled into uranium-oxide (), converted into a gaseous state known as uranium-hexafluoride (), and then enriched via highly complex gas centrifuges into Low-Enriched Uranium (LEU).61

The statistics regarding this dependency are alarming. In 2023, the European Union relied on Russia for 23% of its natural uranium supply and an astonishing 27% of its conversion services (amounting to 3,543 tU).62 Similarly, the United States relies heavily on foreign enrichment; approximately 27% of the enriched uranium utilized by U.S. commercial reactors in recent years originated in Russia, which single-handedly controls roughly 44% of total global enrichment capacity.14

Furthermore, the next generation of advanced Small Modular Reactors (SMRs) requires a specialized fuel known as High-Assay Low-Enriched Uranium (HALEU)—which is enriched to between 5% and 20%.13 Currently, Rosatom’s subsidiary, Tenex, operates as the only commercial producer of HALEU in the world.13 This effective monopoly has severely paralyzed the deployment of advanced reactor designs in the West, as commercial developers and utilities cannot commit billions of dollars to reactor designs without a guaranteed fuel supply independent of Moscow.13

9.2 Western Decoupling Efforts and Sanctions

In response to the overt weaponization of energy supplies following the 2022 invasion of Ukraine, the United States and the European Union are attempting a rapid, highly expensive reconstruction of their domestic nuclear fuel cycles.

In May 2024, the United States enacted the Prohibiting Russian Uranium Imports Act (H.R. 1042), legally banning the import of Russian uranium products.64 However, recognizing the immediate, critical supply deficit this would cause for currently operating plants, the law permits a strategic waiver process through January 1, 2028, to prevent American reactors from shutting down due to fuel starvation while domestic capacity is slowly rebuilt.14 Concurrently, the U.S. Congress appropriated $2.72 billion to the Department of Energy to aggressively jumpstart domestic enrichment and HALEU production capabilities.13

In Europe, the REPowerEU roadmap mandates the phase-out of Russian energy dependencies.62 Western nuclear fuel conglomerates, including Orano in France, Cameco in Canada, and Urenco, are racing to expand their domestic conversion and enrichment facilities.63 However, entirely phasing out Russian nuclear dependency remains immensely difficult, particularly for Eastern European member states (such as Hungary and Slovakia) that operate Russian-designed VVER reactors.65 These specific reactor designs require highly customized Russian fuel assemblies, making a rapid switch to Western fuel fabricators a profound technical and safety challenge.61

10. Strategic Conclusions

The global commercial nuclear power industry currently operates under a paradigm defined by intense, systemic contradictions. On one hand, nuclear energy is increasingly recognized by international coalitions and energy economists as absolutely indispensable for achieving deep, rapid macroeconomic decarbonization while simultaneously ensuring baseload grid stability in the emerging era of hyperscale artificial intelligence computing. This stark realization has definitively halted decades of premature plant closures in the United States, prompted unprecedented, multi-billion-dollar moves to resurrect decommissioned reactors like Palisades and Three Mile Island, and spurred an aggressive, state-backed build-out of new capacity in the global East.

On the other hand, the Western industrial base has largely lost the institutional knowledge required to build large-scale nuclear infrastructure efficiently. The staggering capital costs, supply chain bottlenecks, and decade-long delays defining megaprojects like Vogtle in the United States and Hinkley Point C in the United Kingdom threaten the fundamental financial viability of new large-scale Light Water Reactors in deregulated, free-market economies. Consequently, the commercial momentum has shifted decisively to China and Russia. China is leveraging state financing, localized supply chains, and highly standardized designs to build reactors at a fraction of Western costs. Simultaneously, Russia utilizes Rosatom as a primary arm of geopolitical statecraft, locking developing nations into century-long technological, financial, and fuel dependencies through massive export projects in Egypt, Turkey, and Bangladesh.

For Western nations to successfully navigate this perilous strategic landscape, energy policy and capital deployment must remain fiercely dedicated to three interconnected pillars:

- Asset Preservation: Aggressively funding and facilitating the safe operational life extension of the existing, highly profitable LWR fleet to 60 and 80 years, recognizing these plants as irreplaceable strategic assets.

- Supply Chain Sovereignty: Executing a rapid, heavily subsidized reconstruction of domestic uranium conversion and enrichment capabilities to permanently break the Tenex and Rosatom monopolies, thereby securing the fuel cycle for both legacy and advanced reactors.

- Industrial Evolution: Transitioning future reactor construction away from bespoke, site-built megaprojects toward factory-manufactured, modular assembly designs to definitively solve the overnight capital cost crisis that currently paralyzes Western deployment.

Failure to execute decisively on these three fronts will not only jeopardize national climate commitments but will ultimately cede the future of global zero-carbon baseload energy—and the geopolitical leverage it provides—entirely to strategic adversaries.

Please share the link on Facebook, Forums, with colleagues, etc. Your support is much appreciated and if you have any feedback, please email us in**@*********ps.com. If you’d like to request a report or order a reprint, please click here for the corresponding page to open in new tab.

Sources Used

- Reactor status reports – In Operation & Suspended Operation – By Type – (https://pris.iaea.org)., accessed April 23, 2026, https://pris.iaea.org/pris/worldstatistics/operationalreactorsbytype.aspx

- PRIS – Reactor status reports – In Operation & Suspended Operation …, accessed April 23, 2026, https://pris.iaea.org/pris/WorldStatistics/WorldStatisticsLandingPage.aspx

- IAEA Releases Nuclear Power Data and Operating Experience for 2023, accessed April 23, 2026, https://www.iaea.org/newscenter/news/iaea-releases-nuclear-power-data-and-operating-experience-for-2023

- Nuclear Power in the World Today, accessed April 23, 2026, https://world-nuclear.org/information-library/current-and-future-generation/nuclear-power-in-the-world-today

- Reactor Database Global Dashboard – World Nuclear Association, accessed April 23, 2026, https://world-nuclear.org/nuclear-reactor-database/summary

- Executive Summary – The Path to a New Era for Nuclear Energy – Analysis – IEA, accessed April 23, 2026, https://www.iea.org/reports/the-path-to-a-new-era-for-nuclear-energy/executive-summary

- Nuclear Cost Analysis – Anthropocene Institute, accessed April 23, 2026, https://anthropoceneinstitute.com/research/nuclear-economics/

- Hinkley Point C nuclear power station – Wikipedia, accessed April 23, 2026, https://en.wikipedia.org/wiki/Hinkley_Point_C_nuclear_power_station

- Hinkley Point C nuclear plant delayed to 2030 as costs climb to £35bn – The Guardian, accessed April 23, 2026, https://www.theguardian.com/uk-news/2026/feb/20/hinkley-point-c-delayed-to-2030-as-costs-climb-to-35bn

- New Trend: Trying to Restart Retired… | The Breakthrough Institute, accessed April 23, 2026, https://thebreakthrough.org/journal/no-20-spring-2024/new-trend-trying-to-restart-retired-reactors

- Restarting Old Nuclear Reactors: Can It Be Done?, accessed April 23, 2026, https://extension.psu.edu/restarting-old-nuclear-reactors-can-it-be-done

- What’s the Lifespan for a Nuclear Reactor? Much Longer Than You Might Think, accessed April 23, 2026, https://www.energy.gov/ne/articles/whats-lifespan-nuclear-reactor-much-longer-you-might-think

- The New Nuclear Age: Why the World Is Rethinking Atomic Power | Goldman Sachs, accessed April 23, 2026, https://www.goldmansachs.com/insights/articles/new-nuclear-age-why-the-world-is-rethinking-atomic-power

- Securing energy independence: The US path to resilient enriched uranium supply chain, accessed April 23, 2026, https://www.atlanticcouncil.org/blogs/securing-energy-independence-the-us-path-to-resilient-enriched-uranium-supply-chain/

- Power Reactor Information System (PRIS) | IAEA, accessed April 23, 2026, https://www.iaea.org/resources/databases/power-reactor-information-system-pris

- The Database on Nuclear Power Reactors – (https://pris.iaea.org). – International Atomic Energy Agency, accessed April 23, 2026, https://pris.iaea.org/pris/home.aspx

- United States of America – PRIS – Country Details – International Atomic Energy Agency, accessed April 23, 2026, https://pris.iaea.org/pris/CountryStatistics/CountryDetails.aspx?current=US

- The Nuclear Renaissance in a Geopolitical Crossfire: Uranium’s Role in the Net-Zero Transition – JPT, accessed April 23, 2026, https://jpt.spe.org/twa/the-nuclear-renaissance-in-a-geopolitical-crossfire-uraniums-role-in-the-net-zero-transition

- Nuclear Energy Cost Estimates for Net Zero World Initiative, accessed April 23, 2026, https://www.energy.gov/sites/default/files/2024-10/NZW09%20Nuclear%20Energy%20Cost%20Estimates%20for%20Net%20Zero%20World%20Initiative.pdf

- Comparison of AP1000 and APR1400 construction processes and its implications for SMR deployment – Seoul National University, accessed April 23, 2026, https://snu.elsevierpure.com/en/publications/comparison-of-ap1000-and-apr1400-construction-processes-and-its-i/

- Economics of Nuclear Power, accessed April 23, 2026, https://world-nuclear.org/information-library/economic-aspects/economics-of-nuclear-power

- Nuclear Power in Poland, accessed April 23, 2026, https://world-nuclear.org/information-library/country-profiles/countries-o-s/poland

- Plans For New Reactors Worldwide – World Nuclear Association, accessed April 23, 2026, https://world-nuclear.org/information-library/current-and-future-generation/plans-for-new-reactors-worldwide

- Akkuyu Nuclear Power Plant – Wikipedia, accessed April 23, 2026, https://en.wikipedia.org/wiki/Akkuyu_Nuclear_Power_Plant

- Key Highlights from the Turkish Nuclear Market in 2025, accessed April 23, 2026, https://www.nuclearbusiness-platform.com/media/insights/key-highlights-from-the-turkish-nuclear-market-in-2025

- ROADMAPS TO NEW NUCLEAR 2025, accessed April 23, 2026, https://www.oecd-nea.org/upload/docs/application/pdf/2025-11/roadmaps_to_new_nuclear_-_brief_for_ministers_and_ceos.pdf

- Egypt – World Nuclear Performance Report, accessed April 23, 2026, https://world-nuclear.org/our-association/publications/world-nuclear-performance-report/egypt-world-nuclear-performance-report

- Rooppur Nuclear Power Plant – Wikipedia, accessed April 23, 2026, https://en.wikipedia.org/wiki/Rooppur_Nuclear_Power_Plant

- Rooppur Nuclear Power Plant: Who’s responsible for the delays, cost overruns and mismanagement? | Prothom Alo, accessed April 23, 2026, https://en.prothomalo.com/opinion/op-ed/fy3a91mkhi

- Cost modeling and policy insights for deploying two VVER-1200 reactors in the newcomer nuclear country of Bangladesh – ResearchGate, accessed April 23, 2026, https://www.researchgate.net/publication/400694246_Cost_modeling_and_policy_insights_for_deploying_two_VVER-1200_reactors_in_the_newcomer_nuclear_country_of_Bangladesh

- The Next Nuclear Renaissance? – Cato Institute, accessed April 23, 2026, https://www.cato.org/regulation/fall-2025/next-nuclear-renaissance

- The aging of the world’s nuclear reactors – Visualizing Energy, accessed April 23, 2026, https://visualizingenergy.org/age-of-nuclear-reactor-fleets-by-country/

- French 1300 MWe reactor fleet – Task 1, accessed April 23, 2026, https://www.umweltbundesamt.at/fileadmin/site/publikationen/rep0934.pdf

- ASNR: French Authority for Nuclear Safety and Radiation Protection, accessed April 23, 2026, https://regulation-oversight.asnr.fr/

- French regulator says 1300 MW units can operate beyond 40 years – World Nuclear News, accessed April 23, 2026, https://www.world-nuclear-news.org/articles/french-regulator-says-1300-mw-units-can-operate-beyond-40-years

- Nuclear Power in France, accessed April 23, 2026, https://world-nuclear.org/information-library/country-profiles/countries-a-f/france

- Backgrounder on Reactor Pressure Vessel Issues | Nuclear Regulatory Commission, accessed April 23, 2026, https://www.nrc.gov/reading-rm/doc-collections/fact-sheets/prv

- Stress corrosion cracking – MIT Energy Initiative, accessed April 23, 2026, https://energy.mit.edu/news/stress-corrosion-cracking/

- Emerging Issues of Corrosion in Nuclear Power Plants: The Case of Small Modular Reactors – MDPI, accessed April 23, 2026, https://www.mdpi.com/1996-1073/18/24/6376

- IAEA Nuclear Energy Series Stress Corrosion Cracking in Light Water Reactors: Good Practices and Lessons Learned, accessed April 23, 2026, https://www-pub.iaea.org/MTCD/Publications/PDF/P1522_web.pdf

- World Nuclear Industry Status Report 2025 (HTML version), accessed April 23, 2026, https://www.worldnuclearreport.org/World-Nuclear-Industry-Status-Report-2025-HTML-version

- Decommissioning Nuclear Facilities, accessed April 23, 2026, https://world-nuclear.org/information-library/nuclear-fuel-cycle/nuclear-waste/decommissioning-nuclear-facilities

- Nuclear Reactor Shutdown List – EIA, accessed April 23, 2026, https://www.eia.gov/nuclear/reactors/shutdown/

- Nuclear power phase-out – Wikipedia, accessed April 23, 2026, https://en.wikipedia.org/wiki/Nuclear_power_phase-out

- Nuclear Power in Germany, accessed April 23, 2026, https://world-nuclear.org/information-library/country-profiles/countries-g-n/germany

- German nuclear association calls for restart of reactors, accessed April 23, 2026, https://www.world-nuclear-news.org/articles/german-nuclear-association-calls-for-restart-of-reactors

- Restarting Germany’s Reactors: Feasibility and Schedule – Radiant Energy Group, accessed April 23, 2026, https://www.radiantenergygroup.com/reports/restarting-germanys-reactors-feasibility-and-schedule

- Juragua Nuclear Power Plant – Wikipedia, accessed April 23, 2026, https://en.wikipedia.org/wiki/Juragua_Nuclear_Power_Plant

- Bellefonte Nuclear Plant – Wikipedia, accessed April 23, 2026, https://en.wikipedia.org/wiki/Bellefonte_Nuclear_Plant

- Philippines / KHNP To Conduct Study On Revival Of Bataan Nuclear Plant, Say Reports, accessed April 23, 2026, https://www.nucnet.org/news/khnp-to-conduct-study-on-revival-of-bataan-nuclear-plant-say-reports-10-1-2024

- Żarnowiec Nuclear Power Plant – Wikipedia, accessed April 23, 2026, https://en.wikipedia.org/wiki/%C5%BBarnowiec_Nuclear_Power_Plant

- Stendal nuclear power plant – Wikipedia, accessed April 23, 2026, https://en.wikipedia.org/wiki/Stendal_nuclear_power_plant

- Bataan nuclear plant revival pushed amid oil crisis | Philstar.com, accessed April 23, 2026, https://www.philstar.com/business/2026/04/17/2521435/bataan-nuclear-plant-revival-pushed-amid-oil-crisis

- Bataan nuclear plant’s future hinges on new independent regulator – Asian Journal News, accessed April 23, 2026, https://asianjournal.com/philippines/metro-manila/bataan-nuclear-plants-future-hinges-on-new-independent-regulator/

- Poland’s nuclear folly, accessed April 23, 2026, https://beyondnuclearinternational.org/2021/09/20/polands-nuclear-folly/

- Only Cash to Blame for Halting Polish N-Plant Project – NucNet, accessed April 23, 2026, https://www.nucnet.org/news/only-cash-to-blame-for-halting-polish-n-plant-project

- Nuclear power plant in Żarnowiec after all? Pomeranian governor considers changing the location : r/europe – Reddit, accessed April 23, 2026, https://www.reddit.com/r/europe/comments/19915d1/nuclear_power_plant_in_%C5%BCarnowiec_after_all/

- Demolition mission – SWI swissinfo.ch, accessed April 23, 2026, https://www.swissinfo.ch/eng/banking-fintech/demolition-mission/33958712

- Nuclear Power in the Philippines, accessed April 23, 2026, https://world-nuclear.org/information-library/country-profiles/countries-o-s/philippines

- Is a German Nuclear Comeback Possible? – EuropeanRelations.com, accessed April 23, 2026, https://europeanrelations.com/is-a-german-nuclear-comeback-possible/

- Reducing Russian Involvement in Western Nuclear Power Markets, accessed April 23, 2026, https://www.energypolicy.columbia.edu/publications/reducing-russian-involvement-western-nuclear-power-markets/

- Roadmap towards ending Russian energy imports – European Union, accessed April 23, 2026, https://eur-lex.europa.eu/legal-content/EN/TXT/HTML/?uri=CELEX:52025DC0440

- Ending European Union imports of Russian uranium – Bruegel, accessed April 23, 2026, https://www.bruegel.org/sites/default/files/2025-04/ending-european-union-imports-of-russian-uranium-10820_0.pdf

- Prohibiting Imports of Uranium Products from the Russian Federation – State Department, accessed April 23, 2026, https://2021-2025.state.gov/prohibiting-imports-of-uranium-products-from-the-russian-federation/

- Beyond politics: Can the EU really phase out Russian nuclear fuel?, accessed April 23, 2026, https://www.enstrat.hu/en/blog/beyond-politics-can-the-eu-really-phase-out-russian-nuclear-fuel