1. Executive Summary

The first quarter of 2026 has presented the United States firearms industry with a highly complex matrix of macroeconomic headwinds, shifting consumer demand profiles, and aggressive corporate consolidation. Following a period of historically elevated demand during the pandemic and the immediate post pandemic years, the domestic industry is currently navigating a distinct and painful normalization phase. This phase is characterized by persistent domestic inflation, supply chain adjustments, and an environment where retail profitability remains highly elusive despite localized pockets of revenue growth.1 Within this contracting economic environment, corporate strategic maneuvers have accelerated at an unprecedented rate, moving the industry toward rapid global consolidation driven by foreign capital.

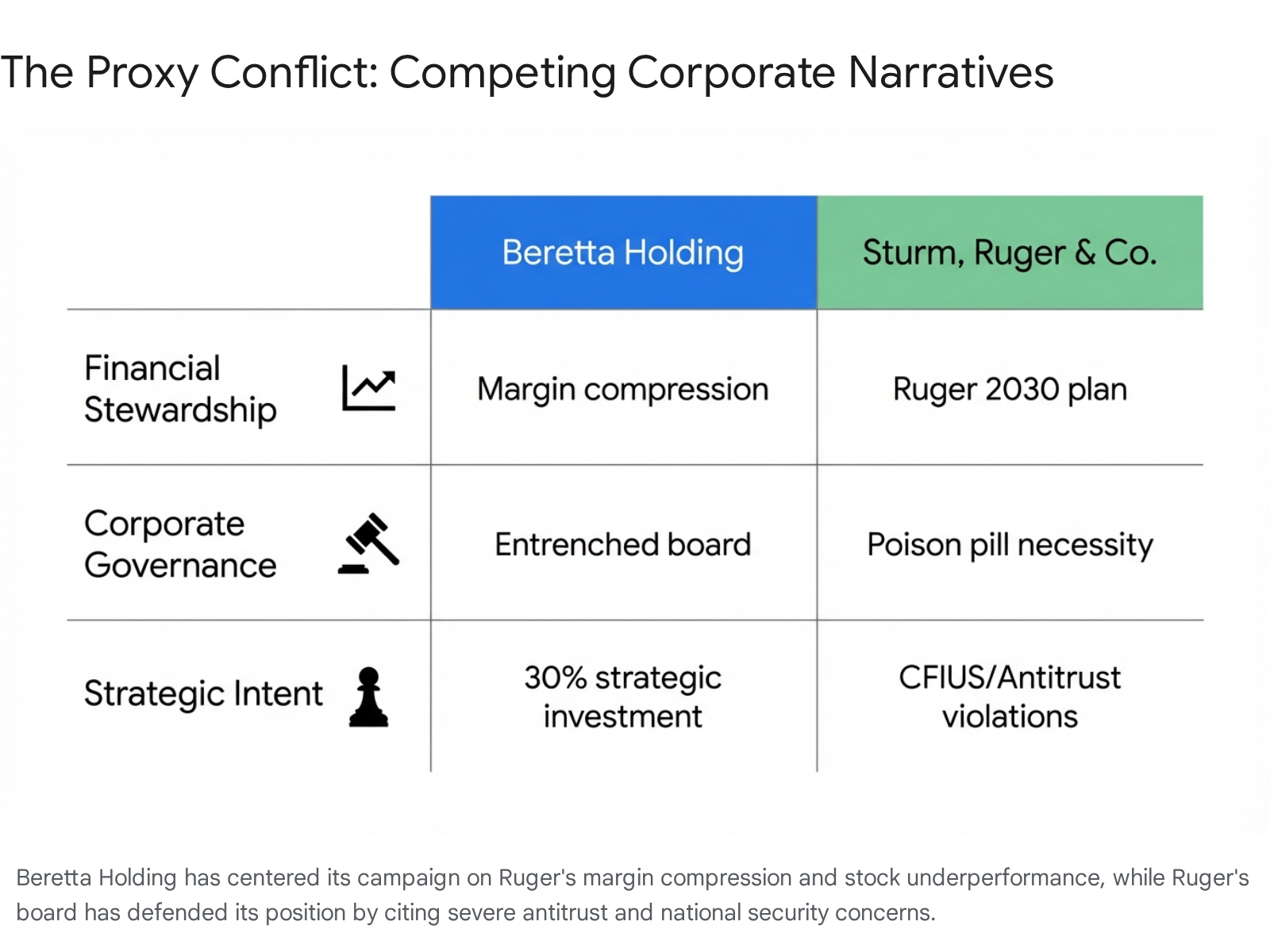

The most significant development defining the first quarter of 2026 is the hostile proxy contest initiated by the Luxembourg based Beretta Holding S.A. against the American manufacturer Sturm, Ruger and Company, Inc. Beretta has launched an aggressive, multi faceted campaign to secure a 30 percent ownership stake through a premium tender offer alongside a proxy fight to install four independent directors on the Ruger board.3 This conflict highlights deep operational disagreements regarding profit margin compression, capital allocation strategies, and overall strategic direction within the firearms industry.3 Furthermore, it has ignited a fierce debate concerning national security, antitrust regulations, and the preservation of domestic independence in the United States small arms manufacturing base.6

Simultaneously, the broader industry reflects these exact tensions and operational difficulties. Major entities such as Smith and Wesson Brands have reported notable revenue contractions and net losses, while highly publicized retail platforms like GrabAGun have struggled with systemic unprofitability following their public offerings.2 The influx of foreign capital is notably not limited to the Beretta and Ruger dispute, as evidenced by the Czechoslovak Group acquiring the ammunition division of Vista Outdoor in a multi billion dollar transaction that has fundamentally reshaped the American sporting goods market.8 This report provides an exhaustive, data driven analysis of the financial state of the firearms industry in the first quarter of 2026, evaluating the economic drivers of this unprecedented consolidation, the operational mechanics of the Beretta proxy fight, and the resulting shifts in consumer and institutional investor sentiment.

2. Macroeconomic Environment and Supply Chain Dynamics

2.1 The Post Pandemic Normalization and Inflationary Pressures

The financial architecture of the firearms industry in early 2026 is defined by a return to baseline demand following years of abnormal, panic driven growth, compounded by severe macroeconomic stressors. In 2025, total industry sales for firearms and weapons manufacturing reached 11.6 billion dollars.10 While this figure appears robust, historical context reveals that over the past three years, the industry has only grown at an annualized rate of 1.6 percent.10 This top line revenue stagnation masks a highly strained operational environment for the 380 companies operating within the domestic manufacturing space.10

The industry has been forced to absorb an estimated 280 million dollars in tariff related costs, while the producer price index growth for 2025 stood at a punishing 5.3 percent.10 These inflationary pressures on raw materials, particularly steel, aluminum, and advanced polymers, have significantly increased the cost of goods sold for domestic manufacturers. Concurrently, these same macroeconomic pressures have directly impacted discretionary consumer spending. Potential buyers are facing higher baseline living costs, leading to a deferment of durable goods purchases, including sporting arms, optics, and ammunition.1 Financial analysts and industry executives consistently characterize the 2026 outlook as a flat to down market environment, acknowledging that the underlying cultural interest in firearms remains strong but is currently severely constrained by tightened household budgets, depleted pandemic savings, and elevated interest rates.12

2.2 Discrepancies Between Background Checks and Retail Sales

Historically, the firearms industry has relied heavily on the Federal Bureau of Investigation’s National Instant Criminal Background Check System to gauge consumer demand and forecast inventory needs. However, data from late 2025 and the first quarter of 2026 has proven that raw background check data can be an imprecise and often misleading proxy for actual retail health. While adjusted background checks declined by 4.1 percent in 2025 and saw further declines of roughly 4.2 percent year over year in early 2026 12, actual retail unit sales experienced a much sharper and more painful contraction.

According to retail analytics provided by RetailBI, new firearm unit sales declined by 9.6 percent year over year in the first quarter of 2025, with total revenue dropping by 11.5 percent.12 Handguns, rifles, and shotguns all faced significant downward pressure at the retail counter.12 This divergence occurs because background checks do not account for used firearm transfers, concealed carry permit applications, or multiple firearm purchases conducted on a single background check.14

Consequently, manufacturers and wholesale distributors who based their production schedules solely on historical background check volumes found themselves struggling with massive excess inventory. This overproduction has led to heavy promotional discounting across the retail sector, triggering the subsequent gross margin compression that is currently plaguing public firearms companies.1

| Demand Indicator Metric | Late 2025 to Early 2026 Variance | Primary Driver of Metric | Strategic Implication for Manufacturers |

| Adjusted NICS Background Checks | Decreased 4.1% to 4.2% | Overall market traffic, permit checks, used transfers. | Mild indicator of cooling foot traffic. |

| Retail Unit Sales (New Firearms) | Decreased 9.6% | Actual consumer purchases of newly manufactured inventory. | Strong indicator of saturated demand and inventory backlog. |

| Retail Revenue (New Firearms) | Decreased 11.5% | Pricing power and consumer willingness to purchase premium models. | Indicates required promotional discounting to move product. |

| NFA Item Background Checks | Increased 167% | Consumer interest in heavily regulated suppressors and short barreled rifles. | Highlights a shift toward enthusiast accessories over base firearms. |

Interestingly, the market for National Firearms Act regulated items has seen a unique and explosive surge. In February 2026, background checks for sound suppressors and short barreled rifles increased by 167 percent compared to the previous year, totaling 209,023 individual checks.15 This isolated growth sector suggests that while the broader market for standard consumer firearms is saturated, dedicated enthusiasts are actively reallocating their discretionary spending toward highly regulated, premium accessories, presenting a rare growth opportunity in an otherwise contracting market.

2.3 Structural Vulnerabilities in the United States Supply Chain

To fully understand the financial pressures on individual companies, one must examine the structure of the United States firearm supply chain. The industry functions through a highly regulated network overseen by the Bureau of Alcohol, Tobacco, Firearms and Explosives.2 Manufacturers typically produce firearms and sell them to large wholesale distributors, who then distribute the inventory to a massive network of licensed dealers.2 In fiscal year 2024, the United States hosted over 128,000 Federal Firearms Licensees, which included 47,776 dedicated retail gun dealers, 6,149 pawnbrokers, and 20,578 specialized manufacturers.2

Even in online or direct to consumer sales models, the end consumer is legally required to pick up the firearm from a local Federal Firearms Licensee to undergo the mandatory background check.2 This required physical touchpoint means that online retailers still rely heavily on the goodwill and operational efficiency of independent brick and mortar stores. When consumer demand falls, independent dealers reduce their wholesale orders to preserve cash flow, causing inventory to rapidly back up into distributor warehouses, which ultimately forces manufacturers to halt production lines and absorb the holding costs. This exact bullwhip effect is the primary cause of the margin deterioration seen across the industry in the first quarter of 2026.

3. The Struggle for Retail Profitability: The GrabAGun Case Study

The macroeconomic challenges facing the retail tier of the supply chain are perfectly encapsulated by the recent financial trajectory of GrabAGun, a prominent online firearm retailer backed by high profile political figures including Donald Trump Jr. and Omeed Malik.2 The company completed its initial public offering in July 2025 under the ticker symbol PEW, originally marketed aggressively as the “Amazon of guns” and positioned as a technology forward platform poised to dominate the digital transformation of online firearm sales.2

Despite generating an impressive 14.1 percent increase in net revenue for the fourth quarter of 2025, totaling 29.6 million dollars, the company reported an operating loss of 0.4 million dollars for the quarter and a full fiscal year net loss of 2.5 million dollars.2 This rapid transition from pre market profitability to public unprofitability was primarily driven by the massive overhead expenses associated with operating as a public entity, including extensive stock based compensation and compliance costs.2 The public equity markets reacted swiftly to this fundamental financial weakness. Investors grew highly skeptical that the company possessed real shareholder value beyond its Second Amendment political rhetoric, resulting in a dramatic and sustained collapse of the stock price, which fell over 71 percent from its debut price shortly after the initial public offering.2

In response to these intense financial struggles and the immediate need to rebuild shareholder value, GrabAGun leadership pivoted aggressively toward a high margin, business to business to consumer model known as PEW Logistics.2 Chief Executive Officer Marc Nemati described this initiative as a first of a kind industry infrastructure provider and direct to consumer fulfillment platform.2 This white label e-commerce platform allows firearm manufacturers, such as KelTec and Derya, to sell directly to consumers online while utilizing GrabAGun’s proprietary, nationwide network of transfer dealers.2

By placing a transfer dealer within 15 miles of 97 percent of the United States population, PEW Logistics attempts to eliminate the structural friction of online gun sales.2 More importantly, the platform solves the industry wide problem of referral leakage, where manufacturers lose sales because consumers navigate away from their corporate websites to find third party retailers with better pricing or more accurate inventory data.2 PEW Logistics provides manufacturers with granular, first party data regarding consumer demographics and purchase patterns, operating on a software style revenue share model that GrabAGun management hopes will yield a structurally higher margin profile than their core retail business.2 Early metrics are promising, with the platform processing over 500 orders and generating 400,000 dollars in gross merchandise value in its first thirty days.2

Furthermore, the retailer became the first major platform in the industry to accept cryptocurrency payments in December 2025.2 This was a highly calculated strategy to capture a younger, digitally native demographic that expects frictionless mobile transactions and often prefers the anonymity and decentralization offered by digital assets.2 GrabAGun noted that mobile engagement accounted for 72 percent of their traffic and 64 percent of their revenue in 2025, underscoring the necessity of this digital pivot.2 However, despite these technological advancements, the company’s struggle to translate top line revenue into positive net income remains a glaring warning sign for the broader retail sector.

4. Manufacturer Margin Compression and Global Consolidation

The manufacturing tier of the firearm supply chain is experiencing financial distress identical to the retail sector, though the scale of capital involved is vastly larger. Manufacturers are currently caught in a vice between rising input costs due to inflation and increased selling expenses required to stimulate stagnant consumer demand.

4.1 Margin Contraction at Smith and Wesson Brands

Smith and Wesson Brands, the closest public peer to Ruger, reported financial results that illustrate the severity of the current market contraction. For its first fiscal quarter of 2026, which ended on July 31, 2025 due to their offset corporate calendar, the company reported a net sales figure of 85.1 million dollars.7 This represented a 3.7 percent decrease from the comparable quarter in the prior year.7 This decline in top line revenue cascaded devastatingly down the income statement, resulting in a net loss of 3.4 million dollars, or a loss of eight cents per share.7

Management explicitly cited compressed margins, lower overall revenue, and higher interest expenses as the primary drivers of this unprofitability.7 To combat the sales slump, the company had to engage in heavy promotional activities. As a result, Chief Financial Officer Deana McPherson projected that operating expenses would rise by 20 percent in the subsequent quarter due to profit sharing obligations, promotional activities, sales initiatives, and the costly launch of the new Smith and Wesson Academy.7

| Smith and Wesson Financial Metric | Fiscal Q1 2026 Result | Year Over Year Variance |

| Net Sales | 85.1 million dollars | Decreased 3.7 percent |

| Net Income | Negative 3.4 million dollars | Transitioned to Net Loss |

| Earnings Per Share | Negative 0.08 dollars | Transitioned to Loss Per Share |

| Adjusted EBITDA | 8.0 million dollars | Significant Contraction |

| New Product Sales Contribution | 37.3 percent of total sales | Highlighted as key growth driver |

Interestingly, Smith and Wesson reported that their handgun shipments actually increased by just over 35 percent year over year during this quarter, even while national adjusted background checks were down 2.4 percent.7 This discrepancy highlights the aggressive tactics manufacturers are using to push inventory into the wholesale channel, offering extended payment terms and bulk discounts to distributors just to keep factory lines running, which ultimately sacrifices profit margins for volume. The fact that new products accounted for 37.3 percent of sales indicates that consumers are only willing to spend money on genuine innovation, completely ignoring legacy product lines.7

4.2 The European Capital Influx and the Vista Outdoor Acquisition

The financial vulnerability of domestic manufacturers has created a highly fertile environment for global consolidation. Foreign conglomerates, particularly those based in Europe with centuries of accumulated capital and deep ties to continental defense ministries, are aggressively purchasing American market share at depressed valuations.

The ongoing conflict in Eastern Europe, specifically the Russia and Ukraine war, has fundamentally altered the global defense economy. Following the invasion, NATO member states massively expanded their defense budgets, pouring billions of dollars into military procurement and ammunition acquisition.16 The United States Department of Defense alone awarded hundreds of millions of dollars in contracts for weapons and equipment destined for Ukraine.17 This massive influx of government spending enriched European defense contractors, providing them with massive capital surpluses just as American commercial firearm companies began to falter.17

These European entities are now utilizing their wartime capital to acquire domestic American commercial assets. The United States civilian market remains the most lucrative consumer firearms market globally, and by acquiring domestic manufacturing facilities, foreign entities bypass import restrictions and secure a permanent, insulated foothold in the American supply chain.18

This trend is starkly illuminated by the Czechoslovak Group, a massive defense and industrial holding company based in Prague. In a definitive agreement structured throughout 2024 and advancing through early 2025, the Czechoslovak Group acquired the sporting products division of Vista Outdoor, known as The Kinetic Group.8 The Kinetic Group controls a massive portion of the American ammunition market, including iconic brands such as Federal, CCI, Speer, and Remington Ammunition.

The transaction valuation was repeatedly increased due to competitive bidding, ultimately reaching a staggering enterprise value of 2.225 billion dollars.9 This transaction represents the absolute largest acquisition in the history of the Czech defense industry and effectively transfers ownership of the backbone of American civilian ammunition production to foreign control.8

Concurrently, Vista Outdoor entered into an agreement to sell its remaining outdoor recreation brands, operating under the Revelyst umbrella, to the global alternative investment firm Strategic Value Partners for 1.125 billion dollars.9 The combined transactions, totaling an enterprise value of 3.35 billion dollars, effectively dissolved a major, publicly traded American corporate entity, replacing it with foreign ownership and private equity structures.9 This massive wave of foreign consolidation serves as the critical macroeconomic and strategic backdrop for the most aggressive corporate maneuver of 2026, the hostile proxy war between Beretta and Ruger.

5. The Sturm, Ruger and Company Financial Landscape

To properly analyze the proxy fight initiated by Beretta, one must first dissect the detailed financial health and strategic posture of Sturm, Ruger and Company. Ruger stands as one of the few remaining publicly traded, strictly independent American firearms manufacturers. However, its recent financial disclosures have revealed significant operational challenges that invited activist intervention.

5.1 Fiscal Year 2025 Performance Data

On March 2, 2026, Ruger released its full year financial results for 2025, revealing a complex picture of relatively robust top line sales masking severe bottom line deterioration. The company achieved full year net sales of 546.1 million dollars, which actually represented a 1.9 percent increase over the 535.6 million dollars generated in the prior year of 2024.2 The fourth quarter of 2025 alone saw net sales reach 151.1 million dollars, up 3.6 percent from the corresponding period.2

Despite these positive revenue metrics, Ruger reported a Generally Accepted Accounting Principles net loss of 4.39 million dollars for the year, translating to a diluted loss of 27 cents per share.2 This marked a dramatic and alarming reversal from the diluted earnings of 1.77 dollars per share achieved in 2024.2 The company recorded an overall operating loss of 12.29 million dollars, fueled heavily by 93.45 million dollars in operating expenses.2

| Sturm, Ruger and Company Metric | Full Year 2025 Result | 2024 Comparative Result | Year Over Year Variance |

| Total Net Sales | 546.1 million dollars | 535.6 million dollars | Increased 1.9 percent |

| GAAP Net Income | Negative 4.39 million dollars | Positive earnings | Transition to Net Loss |

| Diluted Earnings Per Share | Negative 0.27 dollars | Positive 1.77 dollars | Decreased 2.04 dollars per share |

| Adjusted Diluted EPS | Positive 0.84 dollars | Positive 1.86 dollars | Decreased 1.02 dollars per share |

| Cash Generated from Operations | 54.3 million dollars | Not explicitly stated | Indicates strong underlying cash flow |

Management attributed this sudden unprofitability to a combination of persistent inflationary pressures, lower consumer discretionary spending, and several significant one time financial impacts designed to restructure the business for future growth. These one time costs heavily penalized the 2025 income statement. They included severe expenses related to inventory rationalization costing 63 cents per share, product line reduction and SKU elimination costing 24 cents per share, organizational realignment costing 12 cents per share, and the legal costs associated with adopting a stockholder rights plan to defend against Beretta, which cost 4 cents per share.2 When adjusted to remove these extraordinary items, the diluted earnings for 2025 were 84 cents per share, which still represented a steep decline from the adjusted 1.86 dollars per share in 2024.2

5.2 The Ruger 2030 Strategic Initiative and Product Innovation

Recognizing the urgent need to correct this downward financial trajectory and defend against hostile narratives, Chief Executive Officer Todd Seyfert and the board of directors initiated a comprehensive strategic overhaul dubbed the Ruger 2030 plan.2 This five year initiative intentionally focuses on expanding operating margins through disciplined cost alignment, achieving massive structural efficiency across manufacturing plants, and aggressively pushing new product innovation.1

The company is committing heavy capital to execute this turnaround. In 2025, Ruger invested 30.8 million dollars in capital expenditures.2 A significant portion of this capital, specifically 15.01 million dollars, was directed toward the acquisition of manufacturing assets from Anderson Manufacturing in Hebron, Kentucky.2 This strategic acquisition allows Ruger to rapidly expand its production capacity for modern sporting rifles, parts, and accessories, which yield higher profit margins than legacy firearms.2

Product innovation remains the absolute cornerstone of the company’s growth strategy. During the fourth quarter of 2025 alone, Ruger launched an astounding 65 new product models.2 This included three entirely new firearm platforms, namely the Glenfield by Ruger rifle, the Red Label III shotgun, and the highly anticipated Harrier rifle.2 The strategy is currently validating itself at the cash register, as sales of new products introduced within the last two years generated 173 million dollars, accounting for 33 percent of all firearm sales in 2025.2

Furthermore, despite the reported operating losses, the company maintained a highly robust balance sheet to weather the proxy storm. Ruger holds zero debt, maintains 92.5 million dollars in total liquidity, and successfully reduced net inventories from 76.4 million dollars down to 42.8 million dollars by year end.2 Demonstrating confidence to shareholders, the board continued to return capital by declaring a quarterly dividend equated to 40 percent of net income, returning a total of 36.2 million dollars to shareholders through dividends and stock buybacks throughout 2025.2

6. Beretta Holding’s Hostile Proxy Campaign

Sensing acute vulnerability in Ruger’s recent margin compression and localized stock price underperformance, Beretta Holding S.A. launched a highly aggressive and exceptionally rare hostile takeover attempt. The American firearms industry is generally characterized by a gentlemanly, collaborative atmosphere among competing manufacturers, making this very public corporate warfare virtually unprecedented in modern history.19

6.1 The Stealth Accumulation and the Premium Tender Offer

The conflict began quietly in the fall of 2025 when Beretta stealthily accumulated a massive position in Ruger stock on the open market, deliberately avoiding private negotiations until a significant holding was established. By September 22, 2025, Beretta was forced to file regulatory documents with the Securities and Exchange Commission revealing an initial 7.7 percent ownership stake.2 This stake rapidly grew to 9.0 percent, and eventually settled at 9.95 percent, totaling 1,587,000 shares of Ruger common stock.2 As the largest single shareholder, Beretta then demanded an audience with the Ruger board, seeking broad commercial collaboration, discounted stock purchases, and disproportionate board representation.6

When private negotiations fractured due to what Ruger described as extreme demands, Beretta escalated the situation dramatically. On March 25, 2026, Beretta submitted a formal letter to the Ruger board proposing an all cash partial tender offer.4 The aggressive offer sought to acquire up to an additional 20.05 percent of Ruger’s currently outstanding shares, which would elevate Beretta’s total beneficial ownership to precisely 30 percent.4

To entice institutional shareholders, Beretta offered 44.80 dollars per share in cash.4 This represented a highly lucrative 20 percent premium over the volume weighted average price of Ruger stock during the preceding 60 trading days ending on March 24, 2026.4 Beretta publicly framed this maneuver not as a hostile corporate takeover, but as a strategic minority investment designed to rescue a failing American institution.4 In its public communications, Beretta argued emphatically that a 30 percent beneficial ownership stake does not amount to de facto corporate control, but rather provides the necessary shareholder leverage to partner with Ruger and implement Beretta’s five centuries of operational and engineering expertise to fix broken production lines.4

6.2 The “Reload Ruger” Campaign and Board Nominations

To force the tender offer through the reluctant Ruger board, Beretta initiated a brutal proxy fight designed to fundamentally alter the composition of the Ruger board of directors at the upcoming 2026 Annual Meeting of Stockholders. Beretta launched a dedicated website, aptly named Reload Ruger, to bypass corporate management and speak directly to retail and institutional investors.2

Through formal letters to shareholders and Securities and Exchange Commission filings via a WHITE universal proxy card, Beretta formally nominated four independent candidates, namely William F. Detwiler, Mark DeYoung, Fredrick DiSanto, and Michael Christodolou, to replace incumbent members.2 Beretta’s campaign strategy relies on harshly criticizing the financial stewardship and personal accountability of the incumbent Ruger board.

The dissident group highlighted three catastrophic failures of the current leadership to sway institutional voters 3:

- Sustained Share Price Underperformance: Beretta pointed out that Ruger consistently trailed its closest public peer, Smith and Wesson, and broader market indices, despite operating in the exact same macroeconomic and regulatory environment.

- Rapid Operational Deterioration: Beretta heavily publicized Ruger’s recent financial collapse, noting a 23 percent gross margin compression, a 30 percent operating margin compression, and a staggering 103 percent decline in net income since the highs of 2021.3 They emphasized that operating income plummeted from a 52 million dollar profit in 2023 to a 12 million dollar loss in 2025.23

- Significant Lack of Financial Alignment: Beretta ruthlessly criticized the entrenched nature of the Ruger board, noting that certain legacy directors held a combined 65 years of tenure but owned approximately 1 percent of the company’s total shares.3 Despite delivering a negative 13.81 percent total shareholder return during their recent tenure, these specific directors collected over 5.7 million dollars in aggregate compensation.2

Beretta formally requested an immediate exemption from Ruger’s corporate defenses to proceed with the tender offer, setting a deadline for board approval that the Ruger executives swiftly and publicly rejected.26

7. Ruger Corporate Defense Strategies and National Security Implications

Faced with an existential threat to its legacy and corporate independence, the Ruger board of directors, led by Chairman Michael Callahan and Chief Executive Officer Todd Seyfert, initiated a robust, multi tiered corporate defense strategy designed to delay Beretta and rally domestic shareholders.

7.1 The Implementation of the Stockholder Rights Plan

The primary structural defense executed by the board was the immediate adoption of a limited duration stockholder rights plan, widely known in corporate finance as a poison pill, on October 14, 2025.2 The board implemented this mechanism precisely to halt Beretta’s creeping takeover via unannounced open market stock accumulation, granting management the necessary time to formulate a strategic response.2

The rights plan stipulated that if any entity acquired 10 percent or more of Ruger’s common stock without prior board approval, a massive dilution trigger event would occur.2 Upon triggering this threshold, all existing shareholders, strictly excluding the hostile acquiring entity, would receive the right to purchase additional shares of Ruger common stock at a massive 50 percent discount to the current market price.2 This mechanism effectively threatens to dilute Beretta’s holdings so severely that further accumulation becomes mathematically and economically unviable. Beretta’s current ownership of 9.95 percent rests intentionally just a fraction of a percent below this critical trigger threshold, proving the effectiveness of the deterrent.2

7.2 National Security and Antitrust Legal Arguments

Ruger’s most potent defense extends far beyond financial mechanics and directly into the realm of federal regulatory law. The board categorically rejected Beretta’s request for an exemption to the poison pill, arguing that Beretta’s demands for a 25 to 30 percent ownership stake and disproportionate board representation would create severe and immediate legal liabilities for the company.6

Specifically, Ruger leadership argued publicly that granting such immense voting power to a foreign competitor would trigger a mandatory, high scrutiny review by the Committee on Foreign Investment in the United States.6 The Committee on Foreign Investment in the United States is an interagency committee tasked with reviewing foreign direct investment in domestic companies to determine potential threats to national security. Because Ruger manufactures small arms that are absolutely critical to domestic law enforcement agencies and civilian defense infrastructure, surrendering effective operational control to a Luxembourg based entity with deep European military ties implicates highly sensitive supply chain security issues.6

Furthermore, Ruger accused Beretta of attempting to violate United States antitrust laws. During private negotiations prior to the public proxy fight, Beretta allegedly demanded the right to appoint an active member of its own management team directly to the Ruger board of directors.6 Placing an active executive of a direct competitor onto the board of an American manufacturer constitutes a blatant violation of federal antitrust statutes designed to prevent corporate collusion, price fixing, and the monopolization of market sectors. Ruger utilized these legal realities to paint Beretta’s tender offer as legally reckless and strategically untenable.

7.3 Public Relations and the CAMO GREEN Proxy Offensive

To counter Beretta’s digital offensive, Ruger launched its own highly aggressive shareholder defense platform. The company established a dedicated website to disseminate proxy materials, highlighting the historical success of the company, including a massive total shareholder return of over 1,100 percent since 2006, which vastly outperformed industry peers.2

Ruger aggressively contested Beretta’s narrative of being a benevolent savior, revealing that Beretta had initially attempted to purchase Ruger stock directly from the company at a 15 percent discount in a private placement before resorting to hostile open market purchases when rebuffed.6 Ruger framed Beretta’s actions not as those of a concerned shareholder seeking to improve margins, but as a predatory foreign competitor attempting to buy an iconic American legacy brand at a temporarily depressed valuation.6 To ensure clarity at the voting booth and avoid confusion with Beretta’s materials, Ruger urged all shareholders to completely reject Beretta’s WHITE proxy card and exclusively use the company endorsed CAMO GREEN proxy card to vote for the incumbent nine member board slate.2

8. Institutional Governance and Proxy Advisory Shifts

While retail consumer sentiment dictates future revenue potential, the immediate outcome of the proxy war will be decided by massive institutional asset managers and specialized proxy advisory firms. The financial structure of Ruger’s ownership ensures that a few key financial entities will ultimately determine the fate of the 2026 Annual Meeting.

8.1 The Power of Passive Asset Managers

Following Beretta Holding, the largest shareholders of Ruger stock are institutional investment giants. BlackRock Incorporated holds an 8.2 percent stake, the Vanguard Group holds 5.7 percent, and Renaissance Technologies holds 4.8 percent.19 Because individual retail investors notoriously exhibit incredibly low voter turnout in corporate elections, these three institutions possess the consolidated voting power necessary to unilaterally swing the election toward either the incumbent management or the Beretta dissidents.19

8.2 Strategic Shifts in Proxy Advisory Services

The voting decisions of these asset managers are historically heavily influenced by proxy advisory firms, predominantly Institutional Shareholder Services and Glass Lewis. However, the 2026 proxy season is occurring amidst a massive structural shift in how these advisory firms evaluate corporate governance.

Following intense federal regulatory scrutiny and executive orders aimed at curbing the influence of environmental, social, and governance initiatives, massive institutional investors have explicitly changed their mandates to focus purely on financial value and operational performance.31 As a direct result, Glass Lewis and Institutional Shareholder Services are transitioning away from broad benchmark policies and toward client specific voting frameworks that prioritize raw margin improvement.31

This industry wide shift heavily favors Beretta’s argument. Because proxy advisors are now strictly evaluating pure financial metrics rather than social continuity, Beretta’s emphasis on Ruger’s 30 percent operating margin compression and negative net income will resonate powerfully with analysts.3 Ruger’s defense cannot rely merely on qualitative arguments regarding corporate heritage or American independence, it must mathematically prove that the Ruger 2030 strategic plan will generate superior long term capital returns compared to Beretta’s immediate, risk free 44.80 dollar per share cash tender offer.31

Financial equity analysts remain deeply divided on the ultimate outcome, though the broader market signals a belief in Ruger’s underlying, long term value. Following the announcement of the proxy fight and the tender offer, analysts at Lake Street confidently raised their price target for Ruger stock to 43.00 dollars, while other competing analysts maintain targets as high as 48.00 dollars, indicating a firm belief that the company remains fundamentally undervalued whether it successfully remains independent or ultimately succumbs to the acquisition.33

9. Consumer Sentiment and Retail Market Reactions

In the commercial firearms industry, consumer brand loyalty is intensely passionate and uniquely intertwined with concepts of American patriotism, constitutional rights, and mechanical heritage. The corporate battle between Beretta and Ruger has spilled violently over into consumer forums, revealing deep anxieties regarding foreign influence over domestic arms production.

9.1 The Cultural Divide in Firearm Manufacturing

Extensive analysis of online communities, including highly active forums such as Reddit’s r/ruger and r/Beretta boards, indicates a remarkably strong consumer backlash against the takeover attempt.36 The resistance is rooted not just in nationalism, but in fundamentally different manufacturing philosophies. American firearms companies, epitomized perfectly by Ruger, typically operate with a grassroots philosophy, prioritizing rapid adaptation to consumer feedback, platform modularity, and an overarching respect for the civilian Second Amendment culture.21

Conversely, European heritage brands like Beretta, which traces its corporate lineage back to 1526, often employ a rigid, top down engineering approach.21 European business models historically prioritize international prestige, aesthetic tradition, and massive government military contracts over rapid, agile civilian market adaptation.21 Consumers recognize this divide and fear the importation of European corporate culture into an American brand.

9.2 The Imminent Threat of Brand Alienation

Consumers have expressed profound concern that if Beretta successfully infiltrates the Ruger boardroom, the distinctly American character of Ruger’s product lines will be permanently compromised. Industry analysts warn explicitly that a Beretta takeover could catastrophically alienate Ruger’s incredibly loyal customer base.21 Enthusiasts fear the discontinuation of classic, highly affordable American designs in favor of expensive, European styled sporting arms that do not resonate with the domestic market.

This sentiment is explicitly clear in consumer commentary, with brand loyalists threatening organized boycotts. As one highly upvoted commentator noted, if the hostile takeover succeeds, they would permanently cease purchasing from the combined entity, stating they would never send a penny their way.36 While corporate executives often assume that customers remain indifferent to ownership changes as long as product quality persists, the unique ideological and political nature of the American firearms market makes this a highly volatile assumption.19 A successful proxy victory for Beretta could result in a devastating pyrrhic victory if the core consumer base actively rejects the new corporate regime and refuses to purchase the newly managed products.

10. Conclusion

The first quarter of 2026 has mercilessly exposed the structural vulnerabilities deeply embedded within the United States firearms industry. Crushed between the immovable economic forces of macroeconomic inflation, punishing tariffs, and rapidly softening consumer demand, domestic manufacturers and retailers are experiencing severe margin compression and systemic unprofitability. This financial weakness has catalyzed an unprecedented wave of global consolidation, threatening the independence of the American small arms supply chain as European entities flush with defense capital acquire domestic assets.

The hostile proxy contest between Beretta Holding and Sturm, Ruger and Company serves as the ultimate, high stakes culmination of these pressures. Beretta’s aggressive attempt to force a 30 percent ownership stake through a premium tender offer exploits Ruger’s recent financial deterioration and leverages the shifting priorities of institutional proxy advisors. However, Ruger’s fierce defense, utilizing poison pills and citing severe national security and antitrust implications, ensures that this conflict will fundamentally redefine corporate governance norms within the defense sector. Ultimately, the resolution of this proxy war will not only dictate the financial future of one of America’s largest and most iconic gunmakers, but will also set a permanent precedent for how foreign capital interacts with domestic security infrastructure and highly ideological consumer markets in the years to come.

11. Appendix: Analytical Framework and Data Aggregation

The comprehensive analysis presented in this report was constructed utilizing a rigorous aggregation of public financial disclosures, regulatory filings, and specialized market intelligence reports generated during the first quarter of 2026. Financial metrics regarding Sturm, Ruger and Company, Smith and Wesson Brands, and GrabAGun were extracted directly from quarterly earnings call transcripts, Form 8-K filings, and annual reports submitted to the Securities and Exchange Commission.

Critical data concerning the proxy contest, including tender offer valuations, shareholder rights plan mechanics, and board nominee slates, were sourced directly from Schedule 13D amendments, PRE14A preliminary proxy statements, and definitive additional materials filed independently by both Beretta Holding S.A. and Sturm, Ruger and Company. Macroeconomic data, including tariff impact estimates and Producer Price Index growth, were integrated from specialized market research providers such as Kentley Insights and the Stockholm International Peace Research Institute.

Retail demand metrics were verified using adjusted National Instant Criminal Background Check System data cross referenced alongside specialized point of sale analytics provided by RetailBI, ensuring a highly accurate view of true consumer demand. Consumer sentiment analysis was derived from extensive qualitative reviews of industry specific digital forums, specifically Reddit, and editorial publications. All financial figures presented within this document are in United States Dollars unless otherwise specified.

Note: Vendor Sources listed are not an endorsement of any given vendor. It is our software reporting a product page given the direction to list products that are between the minimum and average sales price when last scanned.

Please share the link on Facebook, Forums, with colleagues, etc. Your support is much appreciated and if you have any feedback, please email us in**@*********ps.com. If you’d like to request a report or order a reprint, please click here for the corresponding page to open in new tab.

Works cited

- Ruger outlines 2026 plan to sustain growth and expand margins while boosting innovation, accessed April 10, 2026, https://seekingalpha.com/news/4559912-ruger-outlines-2026-plan-to-sustain-growth-and-expand-margins-while-boosting-innovation

- Gun Industry Q1 2026 Financial Update, accessed April 10, 2026, https://smokinggun.org/gun-industry-q1-2026-financial-update/

- Beretta Holding Sends Letter to Ruger Shareholders Highlighting …, accessed April 10, 2026, https://seekingalpha.com/pr/20444506-beretta-holding-sends-letter-to-ruger-shareholders-highlighting-the-urgent-need-for-boardroom

- Beretta Holding Sends Letter to the Ruger Board of Directors Regarding All-Cash, Premium Partial Tender Offer | Nasdaq, accessed April 10, 2026, https://www.nasdaq.com/press-release/beretta-holding-sends-letter-ruger-board-directors-regarding-all-cash-premium-partial

- Beretta Holding (NYSE) pushes four nominees for Ruger board; owns 9.95% – Stock Titan, accessed April 10, 2026, https://www.stocktitan.net/sec-filings/RGR/prec14a-sturm-ruger-co-inc-preliminary-contested-proxy-statement-492b4d0d5a2b.html

- Ruger 2026 Proxy, accessed April 10, 2026, https://ruger.com/micros/proxy2026/?p=news_20260309

- Smith & Wesson (SWBI) Q1 2026 Earnings Transcript | The Motley Fool, accessed April 10, 2026, https://www.fool.com/earnings/call-transcripts/2025/09/05/smith-wesson-swbi-q1-2026-earnings-transcript/

- Czechoslovak Group to acquire Vista Outdoor’s sporting products – CSG, accessed April 10, 2026, https://czechoslovakgroup.com/en/news/the-czechoslovak-group-enters-into-definitive-agreement-to-acquire-vista-outdoor-s-sporting

- Vista Outdoor Enters Into Definitive Agreement with SVP to Sell Revelyst for $1.125 Billion; Delivers an Estimated $45 Per Share in Cash in Combination with CSG Transaction, accessed April 10, 2026, https://investors.vistaoutdoor.com/Investors/news/news-details/2024/Vista-Outdoor-Enters-Into-Definitive-Agreement-with-SVP-to-Sell-Revelyst-for-1.125-Billion-Delivers-an-Estimated-45-Per-Share-in-Cash-in-Combination-with-CSG-Transaction/default.aspx

- Firearms & Weapons Manufacturing – 2026 U.S. Market Research Report with Updated Recession Risk, Forecasts, & Tariff Analysis, accessed April 10, 2026, https://www.marketresearch.com/Kentley-Insights-v4035/Firearms-Weapons-Manufacturing-Research-Updated-44157868/

- Economic Outlook U.S. Q2 2026: Curb Your Enthusiasm – S&P Global, accessed April 10, 2026, https://www.spglobal.com/ratings/en/regulatory/article/economic-outlook-us-q2-2026-curb-your-enthusiasm-s101676533

- U.S. Firearms Industry Today Report 2025, accessed April 10, 2026, https://shootingindustry.com/discover/u-s-firearms-industry-today-report-2025/

- Beretta Proposes Partial Tender Offer for Ruger Shares | Intellectia.AI, accessed April 10, 2026, https://intellectia.ai/news/etf/beretta-proposes-partial-tender-offer-for-ruger-shares

- RetailBI Firearm Sales Index: January 2026 – The Outdoor Wire, accessed April 10, 2026, https://www.theoutdoorwire.com/releases/2026/02/retailbi-firearm-sales-index-january-2026

- NSSF-Adjusted NICS Background Checks for February 2026 – The Outdoor Wire, accessed April 10, 2026, https://www.theoutdoorwire.com/releases/2026/03/nssf-adjusted-nics-background-checks-for-february-2026

- The US Guns and Ammunition Market Research Report: Forecast (2024-2030), accessed April 10, 2026, https://www.marknteladvisors.com/research-library/us-guns-ammunition-market.html

- Handgun Market Size, Share, Trends | Growth Statistics [2034] – Fortune Business Insights, accessed April 10, 2026, https://www.fortunebusinessinsights.com/handgun-market-108876

- Shooting Market Growth Analysis, Dynamics, Key Players and Innovations, Outlook and Forecast 2025-2032, accessed April 10, 2026, https://www.intelmarketresearch.com/shooting-market-15064

- Beretta Quietly Became the Largest Shareholder of Ruger. Now the …, accessed April 10, 2026, https://www.outdoorlife.com/guns/beretta-holding-ruger-takeover/

- Sturm, Ruger & Company, Inc. Reports Fourth Quarter and Full-Year 2025 Results, accessed April 10, 2026, https://ruger.com/corporate/PDF/ER-2026-03-02.pdf

- Gun Fight: Why Beretta and Ruger Are Suddenly at Odds – GUNS Magazine, accessed April 10, 2026, https://gunsmagazine.com/podcast/berertta-vs-ruger/

- Beretta Holding (NYSE: RGR holder) eyes premium tender offer for more Sturm Ruger shares – Stock Titan, accessed April 10, 2026, https://www.stocktitan.net/sec-filings/RGR/schedule-13d-a-sturm-ruger-co-inc-amended-major-shareholder-report-5bd3608d5b7f.html

- Beretta Holding Responds to Ruger’s Blatantly False and Misleading Statements | RGR Stock News, accessed April 10, 2026, https://www.stocktitan.net/news/RGR/beretta-holding-responds-to-ruger-s-blatantly-false-and-misleading-iei5zw5l0gwh.html

- Beretta Holding criticizes Sturm, Ruger board over tender offer rejection – Investing.com, accessed April 10, 2026, https://www.investing.com/news/company-news/beretta-holding-criticizes-sturm-ruger-board-over-tender-offer-rejection-93CH-4590720

- Beretta Holding clarifies position on Ruger investment proposal, accessed April 10, 2026, https://uk.investing.com/news/company-news/beretta-holding-clarifies-position-on-ruger-investment-proposal-93CH-4551072

- Beretta Holding (NYSE: RGR) proposes $44.80 partial tender offer and proxy campaign, accessed April 10, 2026, https://www.stocktitan.net/sec-filings/RGR/dfan14a-sturm-ruger-co-inc-sec-filing-bd83c918db07.html

- Sturm, Ruger to Meet with Beretta, Rejects Poison Pill Exemption, accessed April 10, 2026, https://sgbonline.com/strum-ruger-to-meet-with-beretta-rejects-poison-pill-exemption/

- Ruger 2026 Proxy, accessed April 10, 2026, https://ruger.com/proxy2026

- Ruger Sets the Record Straight on Competitor Beretta’s Attempt to Seize Control of Ruger, accessed April 10, 2026, https://www.nasdaq.com/press-release/ruger-sets-record-straight-competitor-berettas-attempt-seize-control-ruger-2026-03-09

- Ruger (NYSE: RGR) Board Urges Votes as Beretta Holds 9.95% Stake, accessed April 10, 2026, https://www.stocktitan.net/sec-filings/RGR/prec14a-sturm-ruger-co-inc-preliminary-contested-proxy-statement-bb981d0a7bae.html

- Key considerations for the 2026 annual reporting and proxy season part II: Proxy statements, accessed April 10, 2026, https://www.whitecase.com/insight-alert/key-considerations-2026-annual-reporting-and-proxy-season-part-ii-proxy-statements

- Executive Order Targeting ISS and Glass Lewis: Impact on the 2026 Proxy Season and Beyond – The Harvard Law School Forum on Corporate Governance, accessed April 10, 2026, https://corpgov.law.harvard.edu/2026/01/06/executive-order-targeting-iss-and-glass-lewis-impact-on-the-2026-proxy-season-and-beyond/

- What is the current Price Target and Forecast for Sturm, Ruger & Company (RGR), accessed April 10, 2026, https://www.zacks.com/stock/research/RGR/price-target-stock-forecast

- RGR Stock Forecast 2026 – Ruger Price Targets & Predictions – Ticker Nerd, accessed April 10, 2026, https://tickernerd.com/stock/rgr-forecast/

- Sturm Ruger & Co (RGR): Analyst Raises Price Target, Maintains B – GuruFocus, accessed April 10, 2026, https://www.gurufocus.com/news/8674333/sturm-ruger-co-rgr-analyst-raises-price-target-maintains-buy-rating-rgr-stock-news?mobile=true

- Ruger being bought out by Berreta – Reddit, accessed April 10, 2026, https://www.reddit.com/r/ruger/comments/1seepu5/ruger_being_bought_out_by_berreta/

- Beretta v. Ruger is happening : https://www.ft.com/content/fb15917c-6290-453f-b834-1be061b97800 : r/Beretta – Reddit, accessed April 10, 2026, https://www.reddit.com/r/Beretta/comments/1qc7x5o/beretta_v_ruger_is_happening/