1.0 Executive Summary

The global supply chain for Rare Earth Elements (REEs) represents one of the most critical vulnerabilities in modern industrial and defense architectures. These seventeen elements, which include the fifteen lanthanides along with scandium and yttrium, form the requisite foundation for advanced permanent magnets, high-performance electronics, precision guided munitions, and renewable energy infrastructure. The current strategic landscape is characterized by a severe structural imbalance. While the physical deposits of these minerals are distributed globally across various continents, the industrial capacity to refine, process, and manufacture them into usable components is overwhelmingly monopolized by the People’s Republic of China. This monopoly does not stem from a sheer geological advantage. Instead, it is the deliberate result of decades of coordinated state-sponsored industrial policy, predatory pricing methodologies, and the aggressive consolidation of midstream processing capabilities.

Despite periodic public announcements detailing the discovery of massive new rare earth deposits in North America, the Arctic, and other allied territories, the strategic dependency remains unbroken. The primary barrier is not upstream mineral scarcity but rather a severe deficiency in midstream processing capability, commonly referred to as the missing midstream problem. Transforming raw mined ore into separated, high-purity rare earth oxides requires complex hydrometallurgical processing, advanced solvent extraction techniques, and massive capital expenditures that are difficult to sustain in free-market economies subject to aggressive foreign price manipulation. Furthermore, stringent environmental regulations in Western nations increase operational costs significantly, creating an economic environment where raw domestic deposits frequently fail to achieve commercial viability.

This report provides an objective and detailed analysis of the current state of the rare earth market, the underlying structural causes of Western dependency, and the specific reasons why raw geological discoveries consistently fail to alter the balance of power. Finally, the report delineates ten strategic development options necessary to break this dependency. These pathways require a synchronized approach utilizing advanced financial instruments, plurilateral trade agreements, advanced material sciences, and highly innovative extraction technologies. The objective is to transition from a reactive posture into a proactive industrial strategy that secures the supply chains essential for national defense and economic continuity over the coming decades.

2.0 The Current State of the Rare Earth Element Market

To understand the severity of the dependency problem, one must first analyze the current state of the rare earth market and the fundamental reliance of critical infrastructure on these materials. The strategic importance of REEs is derived from their unique magnetic, luminescent, and electrochemical properties, which make them currently irreplaceable in modern technological paradigms.

2.1 Criticality to Defense and Advanced Technologies

The defense industrial base is uniquely reliant on secure access to high-purity rare earth elements. Neodymium, praseodymium, dysprosium, and terbium are critical for the production of Neodymium Iron Boron (NdFeB) permanent magnets. These specialized magnets are essential components in the electric motors, targeting systems, and advanced sensors deployed across air, sea, and land platforms.1

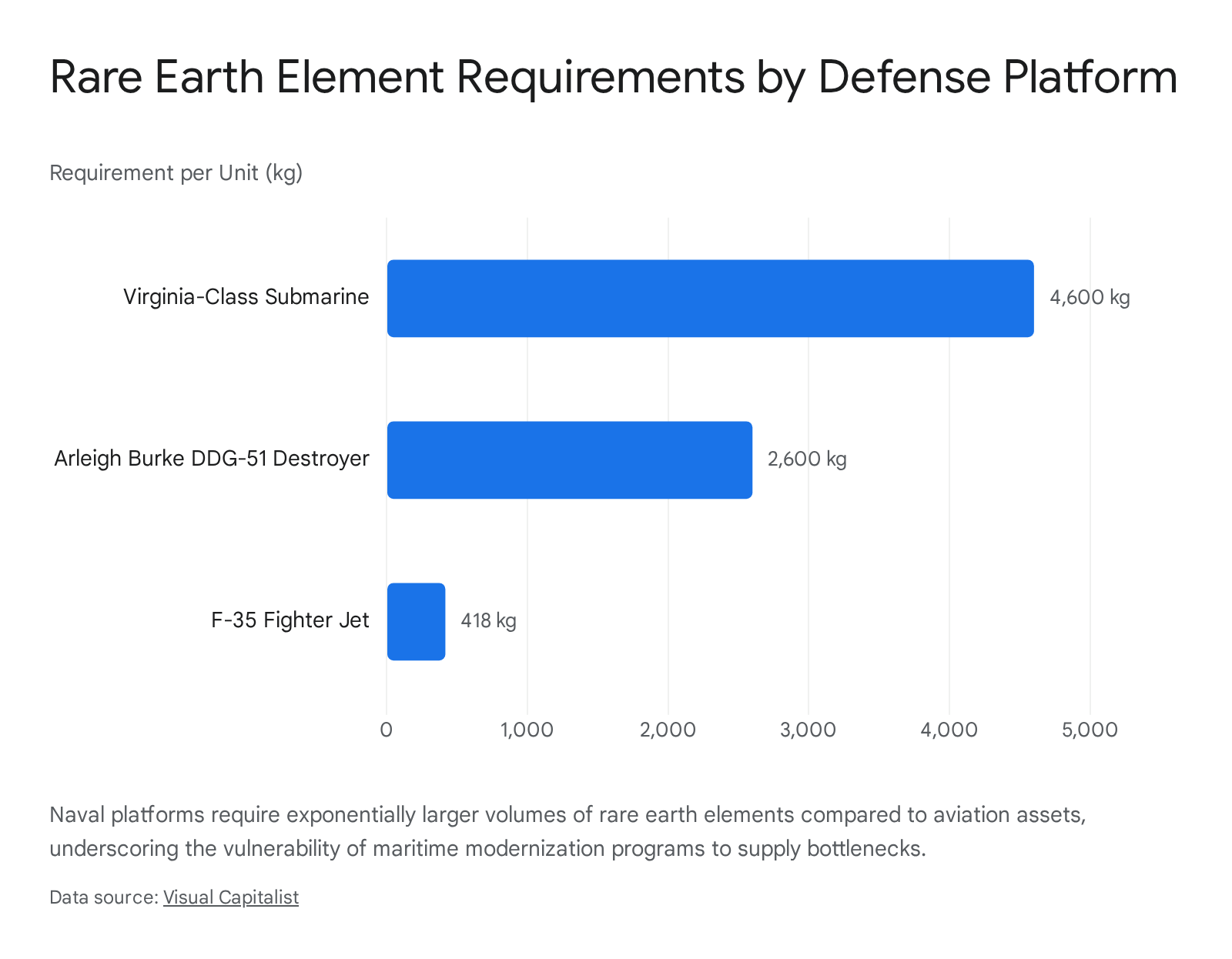

The volume of REEs required for major military platforms illustrates the scale of the vulnerability. A single F-35 Lightning II fighter jet requires approximately 418 kilograms of rare earth materials to function, supporting guided missile systems, radar, and laser targeting technologies used to determine targets.2 The requirement scales drastically for naval platforms. An Arleigh Burke-class DDG-51 destroyer requires approximately 2,600 kilograms of REEs for advanced radar systems, missile guidance, and sophisticated propulsion mechanisms.2 The Virginia-class nuclear-powered attack submarine requires an estimated 4,600 kilograms to support its drive motors, sonar suites, and Tomahawk cruise missile vertical launch systems.2

Furthermore, individual munitions rely heavily on these elements. The BGM-109 Tomahawk Land Attack Missile utilizes REEs in its guidance systems and control actuators.4 Given the high consumption rate of these munitions in sustained conflict scenarios, the ability to rapidly replenish stockpiles is a direct function of supply chain resilience. An interruption in the supply of heavy rare earths, such as dysprosium and terbium, would immediately constrain the production of these platforms. This constraint would thereby degrade the operational readiness of the armed forces and nullify established strategic deterrence architectures.3 Strategic logic dictates that as maritime theaters become increasingly contested, the demand for precision long-range strike capabilities will surge, exacerbating the pressure on already fragile mineral supply lines.5

The following table summarizes the material dependencies of key strategic defense assets, displaying the kilogram weight of rare earths required per unit alongside their primary applications.

| Defense Platform | Rare Earth Element Requirement per Unit (kg) | Primary Technological Applications |

| F-35 Lightning II Fighter Jet | 418 | Guided missiles, laser targeting, radar arrays |

| Arleigh Burke DDG-51 Destroyer | 2,600 | Advanced radar systems, missile guidance, propulsion |

| Virginia-Class Attack Submarine | 4,600 | Drive motors, Tomahawk missile launch systems, sonar |

2.2 Global Distribution of Reserves versus Refining Capacity

The fundamental vulnerability in the rare earth supply chain is not absolute geological scarcity, but rather the severe geographical concentration of processing infrastructure. The global distribution of raw rare earth reserves remains concentrated, but multiple nations possess deposits sufficient to support domestic industries if processing capabilities existed. According to data provided by the International Energy Agency regarding critical mineral outlooks, China accounts for roughly half of the world’s known reserves. This equates to approximately 44 million tonnes of rare earth oxide equivalent, representing 49 percent of the global total.7 Brazil holds a notable 21 million tonnes, representing 23 percent of the global share, while India possesses 7.2 million tonnes.7 Australia, Russia, and Vietnam hold deposits ranging from 3 to 6 million tonnes each, and the United States accounts for approximately 2 percent of total known reserves.7

However, measuring reserves provides an incomplete picture of market dominance. The true measure of geopolitical leverage lies in the capacity to refine and convert these raw resources into high-purity industrial materials. In this sector, China’s dominance is nearly absolute. China accounted for approximately 60 percent of global mined production in recent years, but it commands a staggering 90 to 91 percent of global refining capacity for key rare earth elements.3 Between 2020 and 2024, the geographic concentration of refining increased across nearly all critical minerals.10 For rare earths, this concentration is expected to grow further.12 As a stark point of comparison, the only rare earth processing facility outside of Asia and Oceania is located in Estonia, which refined a mere 368 metric tons in 2024, equating to just 0.6 percent of global output.13

The following table contrasts the distribution of geological reserves against the distribution of midstream refining capacity, illustrating the structural imbalance that defines the current geopolitical crisis.

| Nation / Region | Estimated Share of Global Reserves (%) | Estimated Share of Global Refining Capacity (%) |

| China | 49.0% | 90.0% – 91.0% |

| Brazil | 23.0% | Negligible |

| India | 8.0% | Minimal |

| United States | 2.0% | < 5.0% |

| Europe (Estonia) | < 1.0% | 0.6% |

This massive disparity underscores a key vulnerability identified by global sourcing professionals. While raw resources are geographically widespread, the sophisticated industrial capacity to refine them is entirely localized within the borders of a primary strategic competitor.

3.0 The Source of the Dependency Problem: The Missing Midstream

The core of the United States dependency problem lies securely in the “missing midstream.” The midstream encompasses the highly complex, transformative processing steps required to convert upstream extraction, such as concentrated mineral ores, into separated, high-purity rare earth oxides and metals suitable for downstream manufacturing.8 A nation can possess vast upstream mining operations, but without midstream processing facilities, it remains entirely dependent on foreign powers to render those raw materials useful for technology and defense sectors.

3.1 The Chemical and Technical Complexity of Solvent Extraction

Unlike traditional commodity metals such as copper, iron, or zinc, which can be extracted through relatively standard pyrometallurgical smelting processes, rare earth elements present unique chemical challenges rooted deeply in their atomic structure. All fifteen lanthanides exhibit a phenomenon known as lanthanide contraction. This phenomenon results in nearly identical ionic radii across the entire group of elements.14 Because these elements are chemically indistinguishable in many industrial contexts, separating them from one another requires extreme precision and highly complex hydrometallurgical techniques.8

The primary industrial method utilized to achieve this separation is solvent extraction. This hydrometallurgical process involves dissolving the rare earth mineral concentrates into a liquid solution through an initial leaching step, and then passing that solution through a prolonged sequence of organic solvents.8 These solvents selectively bond with specific rare earth metals, gradually pulling them out of the combined solution. Because the chemical differences between the target elements are exceptionally minute, this process must be repeated continuously through dozens of discrete stages to achieve the 99.9 percent purity levels demanded by high-tech defense and electronics manufacturers.8

Separating light rare earth elements, such as neodymium and praseodymium, typically requires six to eight distinct processing phases.14 Isolating heavy rare earth elements, such as dysprosium and terbium, necessitates an even more grueling twelve to fifteen discrete separation stages.14 This exponential increase in processing complexity requires massive industrial footprints and highly specialized technical expertise. Every distinct mineral deposit requires a unique processing solution, adding layers of difficulty to any domestic capacity expansion strategy.8

Currently, the United States faces a severe and noticeable scarcity of professionals with direct, applied experience in designing, optimizing, and scaling these specific midstream techniques.8 This dearth of domestic engineering expertise directly impacts the ability of nascent American companies to pinpoint systemic inefficiencies, accurately estimate project timelines, minimize operational costs, and effectively train a new generation of hires.8 China, conversely, has spent the last several decades aggressively refining its solvent extraction processes and holds unmatched technical know-how, creating a formidable and highly protected barrier to entry for prospective Western competitors attempting to enter the midstream market.3

3.2 Capital Expenditure and Environmental Compliance Disparities

The capital expenditure required to establish and scale rare earth processing facilities is exorbitant, further discouraging private equity investment in Western nations. Environmental regulations and associated compliance risks play a major role in escalating these costs. Solvent extraction is a highly chemical-intensive process that generates significant quantities of hazardous waste, including acidic wastewater and, depending heavily on the specific geological feedstock, potentially radioactive byproducts such as thorium and uranium.15

Historically, Chinese producers absorbed these environmental externalities by operating with minimal regulatory oversight and highly permissive environmental standards. This structural advantage originally allowed Chinese state-backed firms to drastically undercut global competitors, effectively forcing American and Western mines out of business in the late 1990s and early 2000s.15 The resulting environmental degradation in southern China’s rare earth refining hubs has been catastrophic, prompting the Chinese Ministry of Industry and Information Technology to estimate clean-up costs at roughly $5.5 billion for illegal mining sites alone.15

In stark contrast, modern processing facilities operating in the United States, Europe, or Australia must integrate highly advanced waste management, water treatment systems, and radiation containment protocols into their baseline capital expenditures. Relocating the refining and manufacturing of rare earth ores to countries with stricter environmental regulations and greater public concerns about contamination makes the production of usable elements substantially more expensive.15

This requirement radically alters the economic viability of Western midstream projects. For example, the Australian firm Lynas Rare Earths is currently constructing a dedicated rare earth refinery in Texas to service the United States defense sector. While initially projected at $400 million, the facility construction costs recently surged to an estimated $575 million, representing a hike of more than 40 percent.13 These cost overruns were driven largely by unanticipated complexities regarding the treatment of wastewater and the stringent requirements of local regulatory compliance.13 Such escalating capital requirements act as a powerful deterrent to private investment, forcing critical mineral supply chains to rely heavily on intermittent government subsidies to complete strategic infrastructure.

4.0 Chinese Market Manipulation and Weaponization of Supply Chains

The third fundamental barrier preventing the United States from breaking its rare earth dependency is the systemic and deliberate manipulation of global commodity markets by foreign state actors. Chinese state-backed entities do not operate strictly on traditional free-market principles focused on maximizing quarterly profit margins for independent shareholders. Instead, they pursue market dominance to maximize long-term geopolitical advantage and strategic leverage.16

4.1 State-Sponsored Consolidation and Predatory Pricing

Supported extensively by direct state subsidies and coordinated tightly by the China Rare Earth Industry Association, Chinese enterprises engage in calculated predatory pricing strategies designed to deliberately crash the market value of rare earth oxides whenever competing Western projects near commercial viability.17 The Chinese rare earth sector recently underwent a massive structural reorganization, consolidating production under state-owned behemoths like the China Rare Earth Group.19 This highly centralized structure equips state officials with enhanced mechanisms to seamlessly enforce production quotas, manage strategic reserves, and manipulate global pricing in a manner directly beneficial to their national priorities.19

When global prices fall below the necessary breakeven point for Western producers, who are already burdened by higher operational costs and environmental compliance mandates, private financing quickly evaporates. Private investors and financial institutions correctly identify that without a guaranteed price floor or strict tariff protections, capital injected into Western midstream processing projects will be lost to state-subsidized Chinese undercutting.20 This structural market failure ensures that even if an American company solves the immense technical and environmental challenges of solvent extraction, they remain continuously vulnerable to targeted economic warfare. The strategy is highly effective, as demonstrated by previous bankruptcies of American producers like Molycorp in the mid-2010s.3

4.2 Extraterritorial Export Controls and Regulatory Encirclement

China has frequently demonstrated its willingness to weaponize its monopoly to achieve political objectives. In 2010, the nation abruptly restricted rare earth exports to Japan over a maritime fishing trawler dispute, providing a stark warning regarding the vulnerability of allied supply chains.3 More recently, in 2023, China imposed a comprehensive global ban on the export of specific technologies used for rare earth processing and separation, directly aiming to obstruct the development of midstream capabilities outside its own borders.3

This strategy escalated dramatically in late 2025. On October 9, 2025, the Chinese Ministry of Commerce unveiled sweeping new measures that radically tightened export controls on sensitive materials and technologies.21 Through Ministry of Commerce Notification No. 61 and No. 62, China established unprecedented extraterritorial export controls on rare earth items.21 These regulations incorporated a Chinese version of the de minimis rule and a foreign direct product rule.21

Under these new frameworks, foreign manufacturers operating entirely outside of China are required to obtain specific Chinese government approval to export dual-use items, notably semiconductor and artificial intelligence-related devices, if those goods contain permanent magnet materials incorporating Chinese-origin rare earths at or above a remarkably low 0.1 percent value threshold.22 Furthermore, the regulations adopted a novel 50 percent rule, which imposes presumptive license denials for exports to subsidiaries, branches, and affiliates that are 50 percent or more owned by entities listed on China’s export control watchlists.21 This aggressive regulatory expansion indicates a deliberate strategy to encircle foreign manufacturing sectors, complicating global counterparty diligence and maintaining absolute sovereign leverage over advanced high-tech production supply chains.21

5.0 The Paradox of Raw Deposits: Why Discoveries Do Not Break Dependency

The general public, policy makers, and non-specialist media frequently misinterpret the discovery of new rare earth deposits as an immediate and complete solution to the dependency crisis. Press releases detailing massive geological finds in the United States, Nordic regions, and allied territories generate substantial optimism, but these discoveries rarely translate into operational supply chain resilience. The disparity between physically locating a deposit and achieving true market independence is vast, hindered by extreme economic, logistical, and political realities.

5.1 Economic Viability and Grade Challenges in the United States

A prime example of this phenomenon is the Halleck Creek deposit located in the United States. Recent technical reports proudly indicate that the deposit contains an estimated 7.5 million tonnes of total rare earth oxides, a volume that is undeniably significant on a geological scale.25 However, the physical presence of the mineral trapped within the bedrock does not guarantee economic viability.

Mining operations must extract ore at a grade and scale that comfortably covers the immense upfront capital costs of blasting, crushing, transportation, and eventual chemical separation. If the global market price for rare earth elements is artificially suppressed by Chinese overproduction and predatory pricing, only the absolute highest-grade ores make economic sense to extract.25 The technical reports regarding domestic discoveries are frequently silent on how economic viability can be maintained in a suppressed market environment.25 Consequently, lower-grade portions of these vast deposits, regardless of their total theoretical volume, become economically stranded assets. Without access to a domestic midstream processing hub capable of processing the ore cost-effectively, American mining companies are ironically forced to ship their newly concentrated ore directly to China for refinement, thereby reinforcing the exact dependency the domestic mine was originally intended to alleviate.

5.2 Arctic Logistics and Political Risk in Greenland

Greenland holds some of the world’s most significant undeveloped rare earth reserves, estimated at roughly 36 million tonnes, with 1.5 million tonnes currently considered proven and economically viable for near-term extraction.26 The Kvanefjeld project and the neighboring Tanbreez project are frequently cited in geopolitical discussions as powerful potential alternatives to Chinese supply dominance. However, developing mega-projects in the Arctic presents profound logistical, environmental, and political challenges that routinely derail progress.

The massive Kvanefjeld deposit sits within an exceptionally complex political framework. The geological formations contain significant accumulations of rare earth oxides, but these critical minerals are geologically co-located with substantial uranium and thorium content.28 Following sustained opposition from local communities deeply concerned about potential radioactive contamination and severe environmental degradation, the Greenlandic government officially reinstated a strict ban on uranium mining in 2021.27 This sudden legislative action immediately stalled the development of the Kvanefjeld project, resulting in complex, protracted legal disputes and halting the flow of vital international capital required for development.28

While the rival Tanbreez project possesses a different geological profile with significantly less radioactive material, it faces the harsh logistical realities of Arctic development.29 Establishing a massive mining operation in an area with virtually no pre-existing infrastructure requires constructing specialized heavy-haul roads, deep-water ports capable of handling bulk carriers, independent power generation facilities, and insulated housing for specialized labor in a deeply hostile climate.30 These extreme upfront infrastructure costs make the project highly sensitive to price volatility. Competing effectively against state-backed Chinese investment in such environments demands credible alternatives, such as competitive financing structures and patient statecraft, which standard private markets are naturally hesitant to provide without robust government guarantees.27

5.3 The Misconception of Icelandic Rare Earth Reserves

There is frequent, widespread confusion in popular media and certain analytical circles regarding rare earth potential in the Nordic regions, often conflating the massive geological hard-rock deposits of Greenland with the geothermal landscape of Iceland.31 It is imperative to clarify that Iceland possesses an abundance of geothermal and hydropower energy sources, but it has absolutely no proven traditional mineral fuel or metallic mineral reserves, and its conventional mining sector is virtually nonexistent.33 Visual data aggregators have previously published flawed graphics attributing large rare earth reserves to Iceland by mistakenly conflating different datasets or misinterpreting geological surveys.34

However, innovation is occurring within the Icelandic territory. Companies such as St-Georges Eco-Mining, operating through its subsidiary Iceland Resources, are actively pioneering research into extracting critical metals directly from geothermal effluent.35 This highly unconventional initiative seeks to identify and extract metals from the mineral-rich muds and fluids discharged by geothermal power plants.35 While these novel, secondary-resource extraction methods present fascinating long-term sustainability opportunities and align perfectly with circular economy principles, they are currently in the developmental and research licensing phase. They cannot immediately scale to meet the thousands of tonnes of separated heavy rare earths required annually by the global heavy manufacturing and defense sectors. Therefore, citing Iceland as a near-term solution to the rare earth crisis is factually incorrect.

6.0 Ten Strategic Development Options to Break the Dependency

Breaking the deep structural dependency on Chinese rare earth processing requires a comprehensive, whole-of-government approach that flawlessly integrates aggressive market intervention, rapid technological innovation, and nuanced plurilateral diplomacy. The following ten strategic development options outline a highly viable, multifaceted pathway to achieving total supply chain security for the United States and its allies.

6.1 Deployment of Defense Production Act Title III Capital

Because traditional private capital markets are inherently adverse to the long development timelines, environmental liabilities, and extreme price volatility of the rare earth midstream sector, direct federal intervention is absolutely required to capitalize the necessary infrastructure. Title III of the Defense Production Act (DPA) provides the executive branch with the unique authority to issue direct grants, low-interest loans, and binding purchase commitments to secure domestic industrial capabilities deemed essential for national defense.36

The targeted deployment of DPA funds has recently demonstrated significant success in accelerating critical infrastructure development. Notable examples include the Department of Defense utilizing DPA authorities to execute a massive $400 million equity investment and issue a $150 million loan package to definitively establish heavy rare earth separation capacity at MP Materials in California.37 Concurrently, the Pentagon established a protective price floor of $110 per kilogram for neodymium-praseodymium oxide for this specific facility.37 Furthermore, a $5.1 million award was granted to REEcycle to advance the commercial-scale recovery of heavy rare earths directly from electronic waste.1 Expanding these highly targeted financial injections is critical to crossing the developmental “valley of death,” enabling domestic companies to successfully scale pilot processing plants into full, globally competitive commercial operations.

6.2 Establishment of Commercial Strategic Reserves via Project Vault

While the United States maintains a robust National Defense Stockpile, its mandate is primarily military and its reserves are strictly controlled. Supply chain disruptions in the broader commercial sector also pose severe threats to overarching economic security. The establishment of an original equipment manufacturer driven strategic commercial reserve is a paramount necessity.

Initiatives such as Project Vault, which is backed by a historic $10 billion loan from the Export-Import Bank of the United States, provide a highly effective template for this capability.20 By utilizing public financing matched seamlessly with private capital commitments, manufacturers can pre-fund the procurement and physical storage of processed critical minerals within domestic borders before crises occur. This strategic buffer prevents catastrophic production halts during sudden supply shocks and creates a guaranteed, highly stable demand signal that catalyzes domestic midstream processing investments. Crucially, the model allows OEMs to rotate inventory annually while maintaining readiness, and they cover the storage and interest costs, ensuring the system operates without relying heavily on direct taxpayer subsidies.20

6.3 Implementation of Enforceable Price Floors and Preferential Trading Blocs

To effectively counter the state-sponsored market manipulation and aggressive predatory pricing executed by foreign adversaries, the United States and its trusted allies must immediately establish robust market-stabilizing mechanisms. A highly effective strategic option involves the creation of enforceable price floors for processed critical minerals. Utilizing frameworks such as Section 232 investigations, the government can implement minimum import prices to actively shield domestic producers from the artificial dumping of underpriced foreign minerals designed to disincentivize Western investments.20

Furthermore, establishing a preferential trading bloc among allied nations would allow for the creation of internal reference prices based on fair market value, ethical labor practices, and high environmental standards. Within this protected economic zone, prices for refined rare earths would remain strictly constant regardless of external Chinese production surges.20 These benchmarks would operate as binding price floors, reinforced by adjustable tariffs, preserving pricing integrity and ensuring that long-term capital investments in Western mining and processing projects remain economically viable.20

6.4 Leveraging the 45X Advanced Manufacturing Production Tax Credit

Financial independence requires ongoing operational support to remain competitive globally, not just massive upfront capital injections. The Section 45X Advanced Manufacturing Production Credit, significantly enhanced by recent legislative updates, provides a continuous, highly effective subsidy to directly offset the higher operational costs of domestic mineral processing. The credit offers a substantial 10 percent incentive on the production costs of fifty specifically designated critical minerals, provided they are processed or refined to specified, stringent purity levels within the physical borders of the United States.40

Crucially, the integrity of this generous tax credit must be fiercely protected from foreign exploitation. Legislation such as the Omnibus legislation establishes strict classifications for Foreign Entities of Concern, ensuring that Chinese military companies, banned battery manufacturers, and entities subject to export controls are entirely barred from accessing these specific production tax credits starting in 2026.40 By strictly barring entities with deep ties to adversary nations from accessing the 45X credits, the United States ensures that taxpayer funds strictly benefit secure, independent supply chains, thereby neutralizing insidious attempts by foreign monopolies to subsidize their own operations on American soil.40

6.5 Advancing Plurilateral Coordination through FORGE and Friendshoring

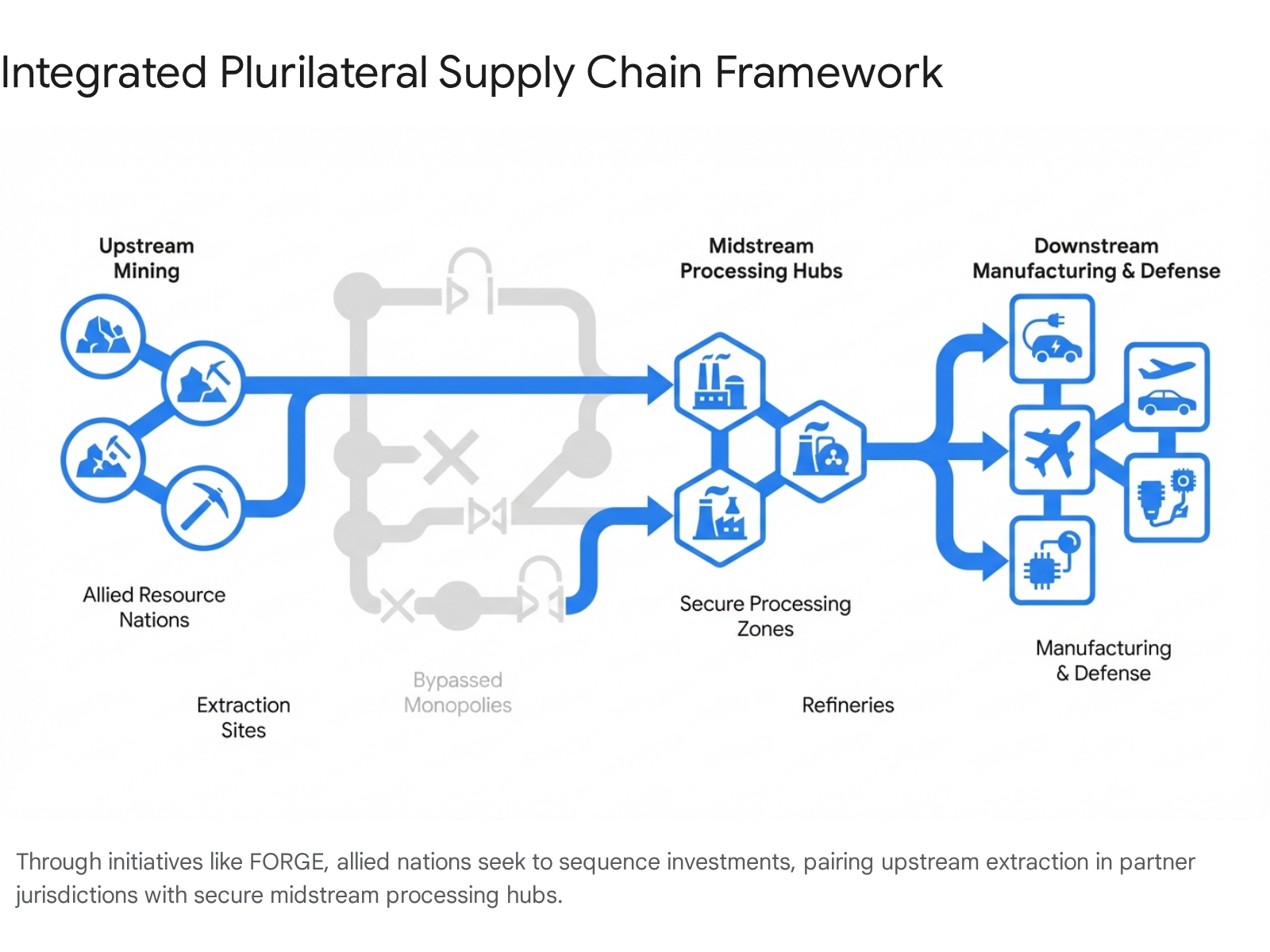

No single nation, regardless of its economic output, currently possesses the financial resources or technical capabilities to independently outpace the entrenched Chinese rare earth monopoly.3 The United States must actively engage in “friendshoring,” which involves sourcing raw materials and coordinating processing infrastructure strictly with a cohesive group of nations that share democratic values, military alliances, and long-term security interests.42

The recent strategic transition from the Minerals Security Partnership to the highly integrated Forum on Resource Geostrategic Engagement represents a critical maturation of this plurilateral strategy.20 FORGE, chaired by the Republic of Korea through June 2026 and comprising 17 member nations, actively facilitates deep policy alignment and sophisticated cross-border project coordination.20 This alliance enables a globally integrated approach where raw ore can be extracted in a resource-rich allied nation, such as Australia or Canada, and shipped seamlessly to a secure, technologically advanced processing hub in the United States. By aligning regulatory frameworks, export controls, and financing tools across borders, the allied bloc can achieve the collective economic scale necessary to influence global markets and counter destabilizing pricing practices.20 Programs like the Pax Silica initiative further integrate these supply chains with the future demands of artificial intelligence and advanced computing.20

6.6 Streamlining Permitting and Regulatory Frameworks for Domestic Projects

The sheer speed of industrial deployment is a critical metric of modern national security. In the United States, bringing a new primary mine or complex processing facility from initial discovery to commercial production currently averages seventeen years, suffocated largely by redundant regulatory environmental reviews and extensive, protracted litigation.43 This sluggish pace deeply deters private investment and severely delays supply chain independence.

The federal government must aggressively prioritize streamlining the permitting processes for critical mineral extraction and midstream processing projects on federal lands. This strategy involves narrowing jurisdictional veto points, limiting state-led interventions that conflict with national defense priorities, and centralizing the overarching environmental review processes.44 To ensure that rapid industrial deployment does not result in severe environmental degradation or compromise ethical standards, these streamlined frameworks should be paired with mandatory, rigorous third-party audits.45 These independent audits would verify that operating companies adhere to strict environmental, social, and governance commitments, carefully balancing the desperate need for speed with responsible ecological stewardship.45

6.7 Engineering Alternative Magnet Technologies

The most decisive and permanent method to break a severe supply chain dependency is to engineer the dependency out of the system entirely through material science innovation. Investing heavily in research to develop completely rare-earth-free alternatives for high-performance permanent magnets is a high-leverage strategic option that completely bypasses the Chinese monopoly.

Considerable, highly promising progress is currently being made in the rapid development of Iron-Nitride and Tetrataenite magnets.46 Companies like Niron Magnetics, operating with support from the Department of Energy and major automotive manufacturers like Stellantis, are pioneering the full commercialization of Iron-Nitride technology.48 This groundbreaking approach utilizes highly abundant, domestically sourced commodity iron ore and atmospheric nitrogen to produce high-performance magnets suitable for electric vehicles and industrial motors.48 Because this unique technology bypasses the lanthanide series entirely, it requires absolutely no complex chemical separation facilities or environmentally hazardous solvent extraction methods. Federal procurement preferences, targeted tax incentives, and research grants must aggressively target these alternative technologies to rapidly transition downstream commercial and defense consumers away from vulnerable rare earth architectures.49

6.8 Deploying Advanced Non-Traditional Extraction Technologies

In critical applications where true rare earths are strictly required by the laws of physics, the processing methodology itself must be radically modernized. The industry must transition swiftly away from legacy, environmentally hazardous solvent extraction toward highly advanced, high-efficiency elemental separation technologies.

Robust research and development programs are currently yielding promising results in several vital areas. Bio-mining, which utilizes specifically engineered microbes, offers a highly sustainable alternative to conventional hydrometallurgy. By leveraging microbially mediated leaching processes and biosorption, biological systems can expertly extract and differentiate specific metal ions from complex ores with significantly reduced chemical volume and lower energy requirements.50 Additionally, the application of chelation-assisted electrodialysis and the utilization of novel ion-imprinted nanocomposite membranes are revolutionizing the precision of elemental separation.53 These cutting-edge technologies utilize electric fields and selectively structured physical barriers to isolate target elements based on extremely subtle differences in molecular charge density.54 This approach potentially allows Western processors to achieve the required 99.9 percent purity levels with a drastically smaller environmental footprint and lower continuous operating costs.

6.9 Mandating Urban Mining and Extended Producer Responsibility

The current global recycling rate for rare earth elements remains abysmally low, resting below one percent of total supply.7 This is largely due to the severe technical and logistical difficulties of recovering microscopic amounts of material deeply embedded within highly complex, end-of-life electronic assemblies.7 Tapping into this massive, ever-growing secondary resource, commonly termed urban mining, provides a highly strategic, low-impact method of securing critical heavy rare earths like dysprosium and terbium.

To make urban mining truly economically viable on an industrial scale, vast logistical scalability is required. This can be achieved definitively through the strict implementation of Extended Producer Responsibility regulations across developed economies.56 These legislative frameworks would legally require manufacturers of consumer electronics, hard drives, and electric vehicles to fully fund or directly manage the end-of-life collection, disassembly, and recycling of their products.56 This policy guarantees a steady, high-volume, reliable feedstock of discarded motors and batteries to domestic recycling facilities, fundamentally solving the logistical bottleneck that currently prevents large-scale rare earth recycling operations from achieving baseline profitability.9

6.10 Commercializing Extraction from Unconventional Secondary Feedstocks

Finally, reducing dependency requires looking creatively beyond traditional hard-rock mining and extracting rare earths directly from vast, pre-existing industrial waste streams. Unconventional feedstocks, such as coal fly ash, acid mine drainage, aluminum refining byproducts, and oil and gas produced wastewater, contain low-level but extractable concentrations of highly valuable critical minerals.52

The strategic advantage of secondary feedstock extraction is remarkably two-fold. First, it completely avoids the immense upfront capital costs, heavy carbon emissions, and multi-year permitting delays intrinsically associated with discovering and opening a virgin primary mine. Second, it contributes directly to environmental remediation by removing hazardous, leachable metals from existing, problematic industrial waste sites. Government research programs, such as the Department of Energy initiatives focused on critical mineral recovery, are currently demonstrating that highly optimized liquid-liquid solvent extraction processes can successfully achieve rare earth recovery yields greater than 90 percent directly from coal byproducts.58 Expanding these proven technologies to a full commercial scale provides a highly secure, entirely domestic supply of rare earths while simultaneously cleaning up legacy industrial sites across the nation.

7.0 Strategic Conclusion

The severe strategic vulnerability resulting from the United States dependency on the People’s Republic of China for refined rare earth elements is a profound, multifaceted national security challenge. It is a dependency methodically engineered through decades of highly targeted industrial policy, the ruthless monopolization of complex midstream processing technologies, and a demonstrated willingness to utilize predatory pricing to deter free-market competition. The repeated public announcements of vast geological deposits located in North America and the Arctic, while factually and geologically accurate, continuously fail to alter this overarching geopolitical dynamic because the true choke point resides entirely in the processing phase, not the extraction phase.

Breaking this dependency permanently demands a fundamental paradigm shift from passive free-market reliance to a highly proactive, muscular industrial strategy. The ten strategic development options outlined in this report provide the necessary structural architecture for total decoupling. By intelligently utilizing financial instruments like Project Vault and the Defense Production Act to forcefully capitalize the missing midstream, establishing strict price floors to protect nascent domestic industries, and coordinating globally via robust plurilateral forums like FORGE, the United States and its trusted allies can successfully reconstruct the supply chain. Furthermore, aggressive, sustained investments in alternative magnet technologies, advanced biological and electrochemical extraction methods, and mandated urban mining logistics will fundamentally alter the material demands of the future economy. Execution of these synchronized strategies is an absolute imperative; the continuation of this processing dependency poses unacceptable, existential risks to both economic sovereignty and long-term military readiness.

Please share the link on Facebook, Forums, with colleagues, etc. Your support is much appreciated and if you have any feedback, please email us in**@*********ps.com. If you’d like to request a report or order a reprint, please click here for the corresponding page to open in new tab.

Sources Used

- Department of Defense Awards $5.1 Million to Recover Rare Earth Elements From Recycled Electronic Waste, accessed April 14, 2026, https://www.war.gov/News/Releases/Release/Article/4033048/department-of-defense-awards-51-million-to-recover-rare-earth-elements-from-rec/

- How Rare Earths Power US Defense – Elements by Visual Capitalist, accessed April 14, 2026, https://elements.visualcapitalist.com/visualizing-how-rare-earths-power-u-s-defense/

- Developing Rare Earth Processing Hubs: An Analytical Approach, accessed April 14, 2026, https://www.csis.org/analysis/developing-rare-earth-processing-hubs-analytical-approach

- Tomahawk missile – Wikipedia, accessed April 14, 2026, https://en.wikipedia.org/wiki/Tomahawk_missile

- The U.S. Navy’s Self-Inflicted Tomahawk Cruise Missile Shortage – National Security Journal, accessed April 14, 2026, https://nationalsecurityjournal.org/the-u-s-navys-self-inflicted-tomahawk-cruise-missile-shortage/

- What Can Trump’s Budget Buy the Navy? Exploring Options and Trade-Offs – CSIS, accessed April 14, 2026, https://www.csis.org/analysis/what-can-trumps-budget-buy-navy-exploring-options-and-trade-offs

- Chart: Where Are the World’s Rare Earths? – Statista, accessed April 14, 2026, https://www.statista.com/chart/33754/countries-with-the-largest-known-rare-earths-reserves/

- The Missing Midstream – Bipartisan Policy Center, accessed April 14, 2026, https://bipartisanpolicy.org/wp-content/uploads/2024/05/BPC_The-Missing-Midstream-Report_May-2024.pdf

- RARE EARTHS: Fledgling rare earths recycling sector offers non-China supply | S&P Global, accessed April 14, 2026, https://www.spglobal.com/market-intelligence/en/news-insights/articles/2026/4/rare-earths-fledgling-rare-earths-recycling-sector-offers-non-china-supply-100009207

- Executive summary – Global Critical Minerals Outlook 2025 – Analysis – IEA, accessed April 14, 2026, https://www.iea.org/reports/global-critical-minerals-outlook-2025/executive-summary

- Global Critical Minerals Outlook 2025, accessed April 14, 2026, https://iea.blob.core.windows.net/assets/ef5e9b70-3374-4caa-ba9d-19c72253bfc4/GlobalCriticalMineralsOutlook2025.pdf

- Regional snapshots – Global Critical Minerals Outlook 2025 – Analysis – IEA, accessed April 14, 2026, https://www.iea.org/reports/global-critical-minerals-outlook-2025/regional-snapshots

- Critical Minerals, Rare Earth Elements, and the Challenges Ahead for the United States, accessed April 14, 2026, https://globalaffairs.org/research/report/critical-minerals-rare-earth-elements-and-challenges-ahead-united-states

- Midstream Processing in Rare Earths: Tech & Economics – Discovery Alert, accessed April 14, 2026, https://discoveryalert.com.au/rare-earth-processing-economics-challenges-2026/

- Can the U.S. Reduce Its Reliance on Imported Rare Earth Elements? | Econofact, accessed April 14, 2026, https://econofact.org/can-the-u-s-reduce-its-reliance-on-imported-rare-earth-elements

- CHINA’S RARE EARTH SUBSIDIES AND STRUCTURAL ADVANTAGES, accessed April 14, 2026, https://thoriumenergyalliance.com/resource/chinas-rare-earth-subsidies-and-structural-advantages/

- Predatory Pricing: How the Chinese Communist Party Manipulates Global Mineral Prices To Maintain Its Dominance – Small Wars Journal, accessed April 14, 2026, https://smallwarsjournal.com/2026/01/12/predatory-pricing-how-the-chinese-communist-party-manipulates-global-mineral-prices-to-maintain-its-dominance/

- Atlantic Council – Mapping China’s strategy for rare earths dominance, accessed April 14, 2026, https://www.atlanticcouncil.org/wp-content/uploads/2025/06/Mapping-Chinas-strategy-for-rare-earths-dominance.pdf

- Of Chinese Behemoths: What China’s Rare Earths Dominance Means for the US, accessed April 14, 2026, https://www.bakerinstitute.org/research/chinese-behemoths-what-chinas-rare-earths-dominance-means-us

- Critical Minerals Ministerial Introduces New International … – CSIS, accessed April 14, 2026, https://www.csis.org/analysis/critical-minerals-ministerial-introduces-new-international-cooperation-strategy

- China Imposes Extraterritorial Export Control Measures Over Rare Earth Items – Jones Day, accessed April 14, 2026, https://www.jonesday.com/en/insights/2025/10/china-imposes-extraterritorial-export-control-measures-over-rare-earth-items

- Ministry of Commerce Notice 2025 No. 61: Announcement of the Decision to Implement Controls on Exports of Rare Earth-Related Items to Foreign Countries | Center for Security and Emerging Technology – CSET, accessed April 14, 2026, https://cset.georgetown.edu/publication/mofcom-notice-2025-61/

- PRC Announces New Export Controls on Rare Earth and Battery Materials and Technology, accessed April 14, 2026, https://www.mayerbrown.com/en/insights/publications/2025/10/prc-announces-new-export-controls-on-rare-earth-and-battery-materials-and-technology

- China imposes extraterritorial jurisdiction and a 50% Rule for export controls on rare earth elements and other items | White & Case LLP, accessed April 14, 2026, https://www.whitecase.com/insight-alert/china-imposes-extraterritorial-jurisdiction-and-50-rule-export-controls-rare-earth

- American Rare Earths Find Comes up Short | Chicago Council on Global Affairs, accessed April 14, 2026, https://globalaffairs.org/commentary/blogs/american-rare-earths-find-comes-short

- Greenland, Rare Earths, and Arctic Security – CSIS, accessed April 14, 2026, https://www.csis.org/analysis/greenland-rare-earths-and-arctic-security

- Greenland’s critical minerals require patient statecraft – Atlantic Council, accessed April 14, 2026, https://www.atlanticcouncil.org/dispatches/greenlands-critical-minerals-require-patient-statecraft/

- Kvanefjeld – Wikipedia, accessed April 14, 2026, https://en.wikipedia.org/wiki/Kvanefjeld

- Greenland’s Rare Earths – Deep Dive into What Lies Beneath – Strategic Metals Invest, accessed April 14, 2026, https://strategicmetalsinvest.com/greenland-rare-earths-deep-dive-2025/

- U.S. Push for Greenland’s Minerals Faces Harsh Arctic Realities – e360-Yale, accessed April 14, 2026, https://e360.yale.edu/features/greenland-critical-minerals

- The Truth Behind Greenland and Iceland’s Confusing Names [ID2027] – YouTube, accessed April 14, 2026, https://www.youtube.com/watch?v=ZvmFRuPhAf8

- What are the misconceptions about Greenland’s resources and why is its development so challenging? – Quora, accessed April 14, 2026, https://www.quora.com/What-are-the-misconceptions-about-Greenlands-resources-and-why-is-its-development-so-challenging

- The Mineral Industry of Iceland in 2019 – USGS Publications Warehouse, accessed April 14, 2026, https://pubs.usgs.gov/myb/vol3/2019/myb3-2019-iceland.pdf

- How Greenland’s Rare Earth Reserves Compare to the Rest of the World : r/Infographics – Reddit, accessed April 14, 2026, https://www.reddit.com/r/Infographics/comments/1qhnt94/how_greenlands_rare_earth_reserves_compare_to_the/

- St-Georges explores unique geothermal-derived metals opportunity – YouTube, accessed April 14, 2026, https://www.youtube.com/watch?v=4cgutp1xrY0

- Defense Production Act (DPA) Title III Rare Earth Element (REE) Separation and Processing Project Statement of Objectives (SOO) – Grants.gov, accessed April 14, 2026, https://apply07.grants.gov/grantsws/rest/opportunity/att/download/292954

- U.S. Expands Critical Minerals Financing and Bilateral Partnerships Under Trump, accessed April 14, 2026, https://www.bhfs.com/insight/u-s-expands-critical-minerals-financing-and-bilateral-partnerships-under-trump/

- Unpacking the DoD and MP Materials Critical Minerals Partnership, accessed April 14, 2026, https://fas.org/publication/unpacking-dod-and-mp-partnership/

- 2026 Critical Minerals Ministerial – U.S. Mission to The African Union, accessed April 14, 2026, https://usau.usmission.gov/2026-critical-minerals-ministerial/

- Impacts of the One Big Beautiful Bill Act on the Mining Sector – CSIS, accessed April 14, 2026, https://www.csis.org/analysis/impacts-one-big-beautiful-act-mining-sector

- Q&A | The Debate over the 45X Tax Credit and Critical Minerals Mining – Center on Global Energy Policy at Columbia University SIPA | CGEP %, accessed April 14, 2026, https://www.energypolicy.columbia.edu/qa-the-debate-over-the-45x-tax-credit-and-critical-minerals-mining/

- Why Can’t We be Friends? Friendshoring the REE Supply Chain – USITC, accessed April 14, 2026, https://www.usitc.gov/sites/default/files/publications/332/executive_briefings/ebot_friendshoring_ree.pdf

- Special Report: Top 10 Themes for 2026 – Sprott, accessed April 14, 2026, https://sprott.com/insights/top-10-themes-for-2026/

- Top 10 Energy Issues for 2026: What to Watch and Why It Matters | ArentFox Schiff, accessed April 14, 2026, https://www.afslaw.com/perspectives/energy-cleantech-counsel/top-10-energy-issues-2026-what-watch-and-why-it-matters

- Securing defense critical minerals: Challenges and U.S. strategic responses in an evolving geopolitical landscape – Taylor & Francis, accessed April 14, 2026, https://www.tandfonline.com/doi/full/10.1080/01495933.2025.2456427

- Rare Earth Permanent Magnet Alternatives – Innovate UK Business Connect, accessed April 14, 2026, https://iuk-business-connect.org.uk/wp-content/uploads/2025/07/IUK-Climate-REE-Alternatives-Report-TW-D4-compressed.pdf

- Alternatives to rare-earth magnets, accessed April 14, 2026, https://suprememagnets.com/blogs/articles/whats-happening-in-the-world-of-magnets

- Niron Magnetics and Stellantis Partner to Pioneer Rare-Earth-Free Electric Motor Innovation, accessed April 14, 2026, https://www.nironmagnetics.com/news/niron-magnetics-and-stellantis-partner-to-pioneer-rare-earth-free-electric-motor-innovation

- Niron Magnetics CEO: Five Steps to U.S. Permanent Magnet Dominance – NAM, accessed April 14, 2026, https://nam.org/niron-magnetics-ceo-five-steps-to-u-s-permanent-magnet-dominance-35252/

- REE Bio-mining – Barstow Research Team, accessed April 14, 2026, https://barstow.bee.cornell.edu/research/ree-bio-mining/

- Urban Biomining of Rare Earth Elements: Current Status and Future Opportunities – PMC, accessed April 14, 2026, https://pmc.ncbi.nlm.nih.gov/articles/PMC12828617/

- Biotechnological Solutions for Critical Mineral Recovery from Unconventional Feedstocks – Publications, accessed April 14, 2026, https://docs.nrel.gov/docs/fy25osti/96534.pdf

- Rare Earth Elements Recovery Using Selective Membranes via Extraction and Rejection, accessed April 14, 2026, https://www.mdpi.com/2077-0375/12/1/80

- Chelation-Assisted Electrodialysis for REE Extraction – Discovery Alert, accessed April 14, 2026, https://discoveryalert.com.au/ion-transport-advanced-mineral-processing-2025/

- Clean energy supply chains of the future need a circular economy | World Economic Forum, accessed April 14, 2026, https://www.weforum.org/stories/2026/01/circular-economy-clean-energy-supply-chain-critical-minerals/

- The Strategic Future of Rare Earth Elements (REEs) in 2026 | by Artiscribe | Medium, accessed April 14, 2026, https://medium.com/@Artiscribe/the-strategic-future-of-rare-earth-elements-rees-in-2026-6147a17f4e3b

- Leapfrogging China’s Critical Minerals Dominance – Council on Foreign Relations, accessed April 14, 2026, https://www.cfr.org/reports/leapfrogging-chinas-critical-minerals-dominance

- Recovery of Rare Earth Elements and Critical Materials from Coal and Coal Byproducts – Department of Energy, accessed April 14, 2026, https://www.energy.gov/sites/default/files/2022-05/Report%20to%20Congress%20on%20Recovery%20of%20Rare%20Earth%20Elements%20and%20Critical%20Minerals%20from%20Coal%20and%20Coal%20By-Products.pdf

- Framework for Securing American Critical Mineral Supply Chains – Bipartisan Policy Center, accessed April 14, 2026, https://bipartisanpolicy.org/explainer/us-critical-mineral-supply-framework/