1. Executive Summary

During the reporting period of May 9 through May 15, 2026, the global deployment, development, and strategic integration of military drones and autonomous vehicles experienced profound doctrinal shifts and kinetic escalations across the air, land, sea, and space domains. The overarching strategic environment is increasingly defined by the democratization of autonomous capabilities, which continues to aggressively compress the operational decision-making cycles of conventional military forces. This compression is forcing a systemic transition away from expensive, legacy interception platforms toward decentralized architectures defined by affordable, precise mass and software-defined resilience.

In the kinetic theater, the absolute saturation of contested airspace with unmanned aerial systems remains the defining characteristic of modern high-intensity conflict, most visibly demonstrated in the ongoing Russia-Ukraine war. Both belligerent nations executed massive, deep-penetration strikes against critical energy infrastructure, military logistics nodes, and naval basing facilities during this period. The utilization of complex drone swarms to penetrate integrated air defense systems has transitioned from an experimental tactic to foundational operational doctrine. Concurrently, the proliferation of sophisticated autonomous systems has demonstrably eroded the traditional geographic sanctuary of the continental United States, as evidenced by retrospective intelligence reporting confirming coordinated drone swarm incursions over strategic nuclear bomber facilities within the domestic interior. Furthermore, the operational integration of unmanned surface vessels and subsurface architectures continues to redefine maritime power projection, with active shadowing engagements observed in the Pacific and devastating autonomous strikes executed in the Caspian Sea.

Tactically, the transition from aerial dominance to ground-based autonomous maneuver is accelerating at an unprecedented rate. The historic procurement mandate by the Ukrainian Ministry of Defense for 25,000 unmanned ground vehicles highlights an urgent strategic necessity to fully automate frontline logistics, casualty evacuation, and complex combat engineering tasks amid severe infantry attrition rates. This massive scale-up of ground robotics is mirrored by concurrent NATO exercises on the Eastern Flank, which have critically exposed the vulnerabilities of commercial satellite communication dependencies when operating under dense forest canopies and active electromagnetic interference.

In the space domain, military doctrines are undergoing a fundamental and rapid pivot from the deployment of static orbital assets toward aggressive “orbital warfare” postures. This new operational framework is characterized by the procurement of highly maneuverable, refuelable space vehicles capable of executing rendezvous and proximity operations. Simultaneously, the tactical edge is being redefined by the integration of commercial satellite imagery directly into the command networks of special operations forces, drastically reducing the sensor-to-shooter latency. The paramount lesson observed across all operational domains this week is that defensive architectures must now align symmetrically with the economic cost curve of offensive autonomous swarms, driving the rapid procurement of artificial intelligence-guided kinetic interceptors, decentralized mesh networks, and non-kinetic electronic warfare capabilities.

2. Combined Master Ledger: Events, Developments, and Lessons Learned

To ensure comprehensive operational visibility and strict adherence to temporal tracking protocols, the following master matrix synthesizes all noteworthy kinetic events, new product developments, and strategic lessons learned during the trailing seven days. The data is sorted strictly chronologically by date, and subsequently ordered alphabetically by the primary country involved in the action or announcement.

| Date | Primary Country | Category | Domain | Description of Activity |

| May 9 | Israel | Event | Air | The Israeli Air Force executed three precision drone strikes targeting vehicles located south of Beirut, resulting in four fatalities. This action marked a significant kinetic escalation following the formalized April 17 ceasefire agreement.1 |

| May 9 | Lebanon | Event | Air | Hezbollah forces launched explosive one-way attack drones into northern Israel. One system penetrated airspace near the border town of Misgav Am, wounding three soldiers and demonstrating persistent cross-border strike capabilities.1 |

| May 9 | Russia | Event | Air | Russian military forces flagrantly violated a temporary May 9-11 ceasefire by initiating approximately 10,000 drone sorties and widespread artillery bombardments against Ukrainian positions, aimed at exhausting interceptor stockpiles.2 |

| May 11 | Russia | Event | Land | Russian ground units achieved localized tactical advances near the settlements of Pazeno, Kalenyky, and Riznykivka. These advances were heavily predicated on slow infiltration tactics supported by continuous overhead drone surveillance.2 |

| May 11 | Ukraine | Development | Air | Defense technology firm Mobilicom officially launched the SkyHopper Tactical platform, engineered to provide resilient, cyber-protected command and control for drone swarms operating in highly contested electromagnetic environments.3 |

| May 11 | United States | Development | Land | At the Xponential 2026 autonomous systems conference in Detroit, defense contractors showcased an armed robotic quadruped that is scheduled to undergo rigorous operational evaluations by U.S. special operations units.4 |

| May 11 | United States | Lesson | Multi | The LANPAC 2026 conference commenced, emphasizing the strategic necessity of integrating artificial intelligence and machine learning for decision superiority, and detailing the “Fortress Chain” concept for Indo-Pacific deterrence.5 |

| May 12 | Latvia | Lesson | Land | NATO’s Crystal Arrow 2026 exercise commenced in the Sēlija training area, representing the first large-scale, brigade-level testing of hundreds of unmanned ground vehicles to validate logistics automation on the Eastern Flank.6 |

| May 12 | Russia | Event | Land | Russian forces recorded minor tactical advances near the settlement of Zakitne in the Donbas region. Operations were characterized by the establishment of drone-dominated “gray zones” that preclude traditional armored maneuvers.2 |

| May 12 | Ukraine | Development | Air | Domestic defense manufacturer Reactive Drone announced a comprehensive capability upgrade for the Kazhan unmanned aerial vehicle, significantly enhancing the platform with multi-channel communication systems to resist jamming.8 |

| May 12 | United States | Development | Land | Navigation technology firm TERN formally announced the expansion of its proprietary platform, enabling autonomous off-road vehicles to maintain continuous turn-by-turn guidance in GPS-denied environments without cellular links.9 |

| May 13 | Latvia | Lesson | Land | Multinational operators participating in NATO’s Crystal Arrow exercise reported severe signal degradation for UGVs relying on commercial Starlink terminals beneath dense forest canopies, exposing critical vulnerabilities in C2 networks.6 |

| May 13 | United States | Development | Air | Innoviz Technologies (INVZ) launched an advanced development program for on-sensor perception algorithms, optimizing its InnovizTwo LiDAR hardware to process point-cloud data locally for next-generation autonomous platforms.10 |

| May 13 | United States | Lesson | Air | The conclusion of Operation Clear Horizon in Florida exposed critical weaknesses in U.S. counter-drone defenses against Ukraine-style infiltration tactics, forcing the Pentagon to radically shift doctrine toward affordable kinetic interceptors.11 |

| May 14 | Russia | Event | Air | Russian forces unleashed the heaviest concentrated drone assault of the war against Ukraine, launching over 1,560 loitering munitions and 56 missiles over a 48-hour period, resulting in severe civilian infrastructure damage in Kyiv.12 |

| May 14 | Ukraine | Development | Space | Ukrainian defense conglomerate Fire Point announced ambitious plans to deploy dozens of military satellites by 2027. The constellation aims to reduce dependence on Western intelligence and enable autonomous deep-strike “kill zones”.14 |

| May 14 | United States | Lesson | Space | The Pentagon initiated operational testing of the SkyFi web-based platform. This integration seeks to transform commercial satellite architectures into tactical infrastructure, delivering real-time geospatial intelligence to Special Operations Forces.15 |

| May 14 | United States | Development | Multi | The annual SOF Week 2026 conference officially opened its exhibition hall in Tampa, Florida, serving as the premier venue for unveiling new tactical autonomy platforms, counter-UAS systems, and edge-computing artificial intelligence solutions.16 |

| May 15 | Russia | Event | Sea | Ukrainian unmanned long-range systems successfully penetrated Russian airspace to strike the Kaspiysk naval base in the Caspian Sea, inflicting heavy damage on a small missile boat and a minesweeper of the Caspian Flotilla.17 |

| May 15 | Ukraine | Event | Air | Ukrainian Unmanned Systems Forces launched a complex deep strike against the Ryazan oil refinery (17 million ton annual capacity) southeast of Moscow, continuing a highly effective campaign to degrade Russian military fuel logistics.19 |

| May 15 | United States | Development | Air | The Defense Advanced Research Projects Agency (DARPA) closed its Request for Information regarding the development of autonomous deployment containers to support sustained Group 1-3 drone constellation operations in GPS-denied environments.21 |

| May 15 | United States | Development | Space | SpaceX successfully launched the CRS-34 mission utilizing a Falcon 9 rocket. The autonomous Cargo Dragon spacecraft delivered approximately 6,500 pounds of vital supplies and scientific hardware to the International Space Station.22 |

| May 15 | United States | Lesson | Land | The U.S. Army’s Capability Program Executive Office for Mission Autonomy (CPE Mission Autonomy) formally detailed its doctrinal shift from acquiring bespoke platforms to developing open-architecture “packages of capability” for ground robots.24 |

3. Global Situation Log: Kinetic Events and Combat Operations

The integration of unmanned and autonomous systems into active combat operations during the mid-May reporting period demonstrated a marked increase in operational range, payload capacity, and target discrimination. Across multiple theaters, the tactical geometry of engagements is being rapidly redrawn by the deployment of loitering munitions and deep-strike platforms that bypass traditional lines of contact.

The Middle East Theater: Precision Strikes and Strategic Depletion

Operations in the Middle East during this period highlighted the dual utility of drones for both surgical assassination and strategic air defense depletion. On May 9, 2026, despite the formalization of a ceasefire agreement that went into effect on April 17, the Israeli Air Force executed three precision drone strikes targeting moving vehicles located south of Beirut.1 These kinetic engagements resulted in four confirmed fatalities. The utilization of unmanned aerial systems to conduct targeted strikes deep within Lebanese territory indicates an operational imperative by the Israeli military to maintain persistent, high-altitude overhead surveillance and execute immediate-action kinetic strikes against high-value targets, regardless of nominal diplomatic pauses in ground hostilities.

Simultaneously, Hezbollah forces demonstrated a persistent capacity to project unmanned power across the border. Hezbollah operators launched a series of explosive one-way attack drones into northern Israel. One such drone successfully penetrated Israeli defensive radar networks and struck near the border town of Misgav Am, severely wounding three Israeli soldiers.1 A secondary drone strike targeted an Israeli military vehicle within Lebanese territory.1 These actions confirm that non-state and quasi-state actors retain significant localized launch capabilities, utilizing low-flying, low-radar-cross-section loitering munitions to systematically bypass conventional air defense architectures.

In the broader regional context, earlier assessments confirmed that Houthi forces in Yemen have expanded their unmanned operations beyond maritime shipping disruption. Following the initiation of direct hostilities between the United States, Israel, and Iran, Houthi forces launched complex attack packages featuring multiple unmanned aerial vehicles, anti-ship cruise missiles, and anti-ship ballistic missiles toward Israeli and allied targets.25 While the U.S. military’s Central Command successfully intercepted massive waves of these one-way attack drones over the Red Sea using carrier-based fighter jets and guided-missile destroyers, the Houthi strategy aligns with broader asymmetric doctrines: utilizing inexpensive, mass-produced drones to force technologically superior adversaries to expend highly sophisticated, multi-million-dollar interceptor missiles in defense.25

The Eastern European Theater: The War of Autonomous Attrition

The Russia-Ukraine conflict remains the global epicenter for autonomous warfare innovation and large-scale drone deployments. The reporting period witnessed unprecedented volumes of unmanned aerial attacks, confirming that both belligerents view autonomous deep strikes as the primary mechanism for strategic degradation.

Despite a recognized ceasefire window intended to span from May 9 to May 11, the Russian Federation initiated a massive wave of unmanned aerial sorties. According to Ukrainian intelligence and Western open-source assessments, the Russian military executed nearly 10,000 drone flights during this brief three-day period.2 This overwhelming saturation tactic served a critical dual purpose: it maintained continuous intelligence, surveillance, and reconnaissance coverage over the highly contested frontline “gray zones,” and it systematically depleted Ukrainian surface-to-air interceptor stockpiles. The sheer volume of these sorties underscores Russia’s rapidly maturing domestic mass-production capabilities regarding cheap, attritable airframes and their willingness to expend them at staggering rates.

Leveraging the continuous overhead drone coverage established during the initial wave, Russian ground forces successfully executed localized advances near the settlements of Pazeno, Kalenyky, Riznykivka, and Zakitne.2 Battlefield reporting clearly indicates that the absolute saturation of airspace effectively blinded Ukrainian defensive reconnaissance efforts, allowing Russian infantry units to utilize slow, methodical infiltration tactics. The operational environment in the Donbas region has been completely transformed; traditional massed armor formations have been rendered largely obsolete by persistent drone surveillance. Consequently, both forces are forced into disaggregated, small-unit maneuvers, heavily reliant on autonomous overhead support to detect enemy positions before committing human assets to direct fire engagements.2

The aerial bombardment culminated on May 14, when the Russian military unleashed the heaviest concentrated drone assault recorded in the conflict to date. Over a 48-hour window, Moscow launched an excess of 1,560 attack drones and 56 cruise and ballistic missiles against Ukrainian urban centers, with the capital city of Kyiv serving as the primary target vector.12 The assault complex involved successive waves of Iranian-designed Shahed/Geran-2 loitering munitions explicitly intended to overwhelm the tracking algorithms and exhaust the interceptor magazines of Western-supplied Patriot and NASAMS air defense batteries. Debris from intercepted drones and direct terminal impacts caused severe structural damage across twenty distinct locations in the Kyiv region, resulting in numerous civilian casualties and the complete structural collapse of a nine-story residential building.12

In immediate, calculated retaliation for the strategic strikes on Kyiv, Ukrainian Unmanned Systems Forces launched a highly sophisticated, multi-vector deep strike campaign against critical Russian military and energy infrastructure on May 15. The most strategically significant target was the Ryazan Oil Refinery, operated by Rosneft and located approximately 180 kilometers southeast of Moscow—and over 450 kilometers from the Ukrainian border. Ukrainian autonomous drones successfully penetrated dense Russian air defense rings and impacted the facility, igniting a massive, multi-point fire.19 The Ryazan facility possesses an immense annual processing capacity of 17 million tons and serves as a critical logistics node for producing aviation fuel and diesel required by the Russian military machine.31 This strike continues a systematic, long-term Ukrainian campaign to surgically degrade Russian hydrocarbon revenue and battlefield fuel logistics.

Simultaneously on May 15, Ukrainian long-range drones achieved a monumental feat of autonomous navigation by striking the Kaspiysk naval base situated deep within the Caspian Sea.17 The strike successfully impacted and heavily damaged a small missile boat and a minesweeper belonging to the Russian Caspian Flotilla.17 This flotilla has historically been utilized as an untouchable safe haven from which the Russian Navy launches Kalibr cruise missiles into Ukrainian territory. The ability of Ukrainian drones to bypass extensive electronic warfare networks and layered air defense systems across hundreds of kilometers of hostile territory to strike the Caspian Sea represents a fundamental leap in their strategic reach and autonomous targeting capabilities.18

The Pacific Theater: Maritime Surveillance and Shadowing

While large-scale kinetic engagements dominated Eastern Europe, the Pacific theater witnessed continuous, high-stakes surveillance operations utilizing unmanned systems. Retrospective reporting highlighted a significant encounter involving the United States’ deployment of autonomous unmanned surface vessels. The Seasats Quickfish (also designated Lightfish) USV, a solar-powered autonomous platform, recently completed an extensive transit of more than 7,500 miles across the Pacific Ocean.35

During its operational deployment, the USV experienced an “unexpected encounter” with a Chinese People’s Liberation Army Navy (PLAN) aircraft carrier group. According to executive statements from Seasats, a Chinese destroyer aggressively altered its course to intercept the autonomous vessel, shadowing the drone “very closely” for a duration of twenty minutes.36 While passing within several miles of commercial traffic is common in the open ocean, the deliberate, close-proximity shadowing by a major surface combatant underscores the intense scrutiny and tactical friction surrounding the deployment of uncrewed surveillance assets in highly contested maritime corridors. This incident highlights the growing necessity for autonomous maritime systems to possess advanced hazard avoidance algorithms and resilient data-link protections when operating in proximity to near-peer naval forces.

4. Product Developments, Platform Reveals, and Capability Upgrades

The technological arms race driving the evolution of unmanned systems has demonstrably shifted focus away from basic platform kinematics—such as raw speed and maximum range—toward software resilience, autonomous perception at the edge, and the economics of attritable mass. The product developments and capability upgrades announced during the mid-May reporting period highlight a concerted effort by the global defense industrial base to field systems capable of operating in highly contested environments entirely devoid of standard Global Positioning System (GPS) signals and traditional radio-frequency communication links.

Breakthroughs in Edge Autonomy and Navigation

A critical theme emerging from product reveals is the push to move processing power directly to the sensor level, eliminating the latency and vulnerability associated with cloud-based computing or centralized command links. On May 13, Innoviz Technologies announced a major advanced development program focusing on on-sensor perception algorithms for its InnovizTwo LiDAR hardware suite.10 This software-hardware integration is explicitly designed to allow autonomous military and commercial vehicles to process massive point-cloud data arrays locally at the physical sensor level. By reducing the computational load on the vehicle’s central processing unit, the system achieves the microsecond reaction times necessary for autonomous obstacle avoidance and target classification in chaotic, contested environments.10

Similarly, on May 12, navigation technology firm TERN announced a major capability upgrade, formally expanding its proprietary navigation architecture into off-road and highly austere environments. The software platform allows autonomous ground vehicles to maintain continuous, precise turn-by-turn guidance on unpaved trails, dense woodland routes, and complex terrain entirely independent of GPS, cellular connectivity, or external camera telemetry feeds.9 The system functions by recalibrating its internal positioning in real-time as physical terrain conditions and traction dynamics shift. This offers a critical, immediate solution for military UGVs operating under the heavy enemy electronic jamming canopies that render standard satellite navigation useless.9

SOF Week 2026: The Nexus of Tactical Innovation

The annual SOF Week conference, hosted by the Global SOF Foundation and the U.S. Special Operations Command in Tampa, Florida, served as the premier venue for unveiling new tactical autonomy platforms during the week of May 14-15. The exhibition floor was dominated by technologies emphasizing affordable mass, attritable architectures, and accelerated procurement cycles.16

Textron Systems utilized the event to unveil the RIPSAW M1 UGV technology demonstrator, a ruggedized autonomous platform optimized for advanced littoral and amphibious combat missions.8 Concurrently, defense contractor AEVEX showcased a comprehensive portfolio that merged autonomous systems with forward-deployed manufacturing. AEVEX displayed the Mako Lite unmanned surface vehicle while prominently featuring its ForgeX additive manufacturing capability.39 This demonstration emphasized a critical new logistical concept: the ability for special operations units to 3D-print, assemble, and deploy attritable drone airframes directly at the tactical edge, bypassing highly vulnerable global supply chains.39

Software and communication resilience were equally prominent. Latent AI demonstrated its edge-computing artificial intelligence platforms, which are designed to operate natively on tactical UAVs and ground systems without requiring cloud connectivity. Their systems enable fully autonomous operations in GPS-denied and electromagnetically contested environments.40 On May 11, Mobilicom officially launched the SkyHopper Tactical platform, a system engineered to provide end-to-end secured communications and AI-driven cybersecurity for tactical drone missions.3 Possessing stringent “FCC Trusted Drone” status, the hardware focuses on mobility, rapid deployment, and extreme resilience against signal spoofing and malicious intrusion attempts.3 Furthermore, Emesent showcased its SLAM-based LiDAR mapping systems integrated with Teledyne FLIR defense drones, designed to generate real-time 3D visualizations of GPS-denied environments, such as subterranean tunnel complexes or dense urban interiors.41

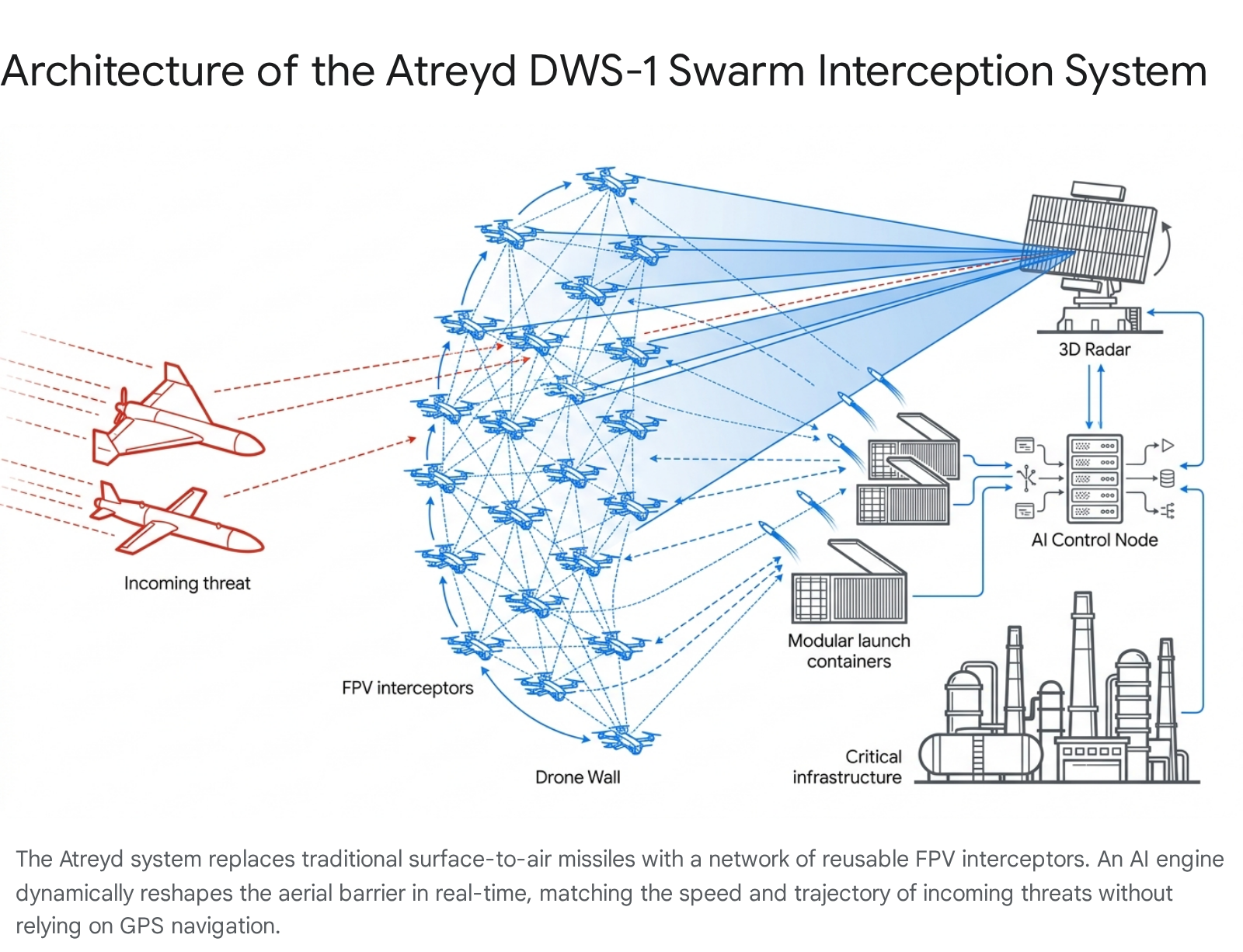

The Operationalization of the “Drone Wall”

Perhaps the most structurally significant product development of the reporting period was the operational deployment of the European-designed Atreyd “Drone Wall” system (DWS-1). Following extensive closed testing, the French startup officially shipped its first complete DWS-1 unit to Ukraine for its inaugural combat deployment, where it will initially be tasked with protecting critical energy infrastructure from Russian loitering munitions.42

The Atreyd system represents a profound paradigm shift in the mechanics of air defense. Instead of relying on the launch of extraordinarily expensive kinetic missiles, the DWS-1 utilizes early-warning 3D radar to detect incoming threats. Upon detection, an artificial intelligence control node automatically triggers the launch of up to 100 heavily armed First-Person View (FPV) interceptor drones from modular ground containers.42

The swarm forms an intelligent, physical aerial barrier. Managed by the AI node, the system continuously and dynamically adjusts the swarm’s formation to match the altitude, speed, and trajectory of incoming glide bombs or attack drones.42 Crucially, the DWS-1 architecture holds a pre-loaded, highly detailed 3D map of its assigned operational environment. This allows the swarm to function flawlessly in completely GPS-denied environments while operating under the heavy electronic warfare blanket typical of the Ukrainian theater.42 While a single human operator retains a manual override kill switch to satisfy rules of engagement, the system is fundamentally designed to identify, engage, and physically intercept targets entirely autonomously.46 Drones that do not detonate during an engagement can be recovered and reused, further driving down the cost per interception.43

Advances in Space-Based Autonomy and Logistics

The drive toward autonomy is extending rapidly into the orbital domain. On May 14, Ukrainian defense conglomerate Fire Point announced the successful launch of two proprietary military satellites earlier this year, outlining an aggressive roadmap to scale the constellation to “dozens” of satellites by 2027.14 This initiative is explicitly designed to reduce Kyiv’s reliance on the United States and commercial Western providers for critical targeting telemetry. Fire Point’s chief designer indicated that this indigenous, autonomous satellite architecture will seamlessly data-link with their expanding production of long-range kamikaze drones. Theoretically, this closed-loop architecture will enable Ukraine to establish independent, autonomous “kill zones” as far away as 200 kilometers inside hostile foreign territory without requiring external intelligence cueing.14

Concurrently, the U.S. Defense Advanced Research Projects Agency (DARPA) closed its Request for Information regarding the development of autonomous drone constellations on May 15.21 Operating through its Tactical Technology Office, DARPA is aggressively pursuing engineering solutions to overcome the severe endurance, payload, and power limitations of current Group 1-3 drones. The agency is seeking conceptual technologies for entirely “autonomous storage containers” capable of self-positioning in GPS-denied environments without human assistance.21 These advanced containers would serve as forward-deployed, automated hubs capable of recovering, physically recharging, and relaunching drone swarms continuously across multiple days, solving the primary logistical bottleneck that currently prevents persistent swarm constellation operations.21

In the realm of orbital logistics, SpaceX successfully executed the CRS-34 mission for NASA on May 15. A Falcon 9 rocket launched from Space Launch Complex 40 at Cape Canaveral Space Force Station, carrying the Cargo Dragon spacecraft. The highly autonomous resupply vehicle successfully delivered 6,500 pounds of vital hardware, science experiments, and crew provisions to the International Space Station, subsequently performing a fully automated rendezvous and docking sequence.22 The routine nature of these autonomous orbital docking procedures serves as the foundational technology baseline for the military’s upcoming shift toward on-orbit satellite refueling and maneuver warfare.

5. Strategic, Operational, and Tactical Lessons Learned

The rapid iteration of unmanned systems in active combat zones and high-fidelity testing environments has generated a wealth of empirical data over the trailing seven days. This data is forcing Western militaries to radically and painfully adapt their operational doctrines. The following lessons highlight the severe friction between legacy military paradigms and the fast-paced realities of algorithmic warfare.

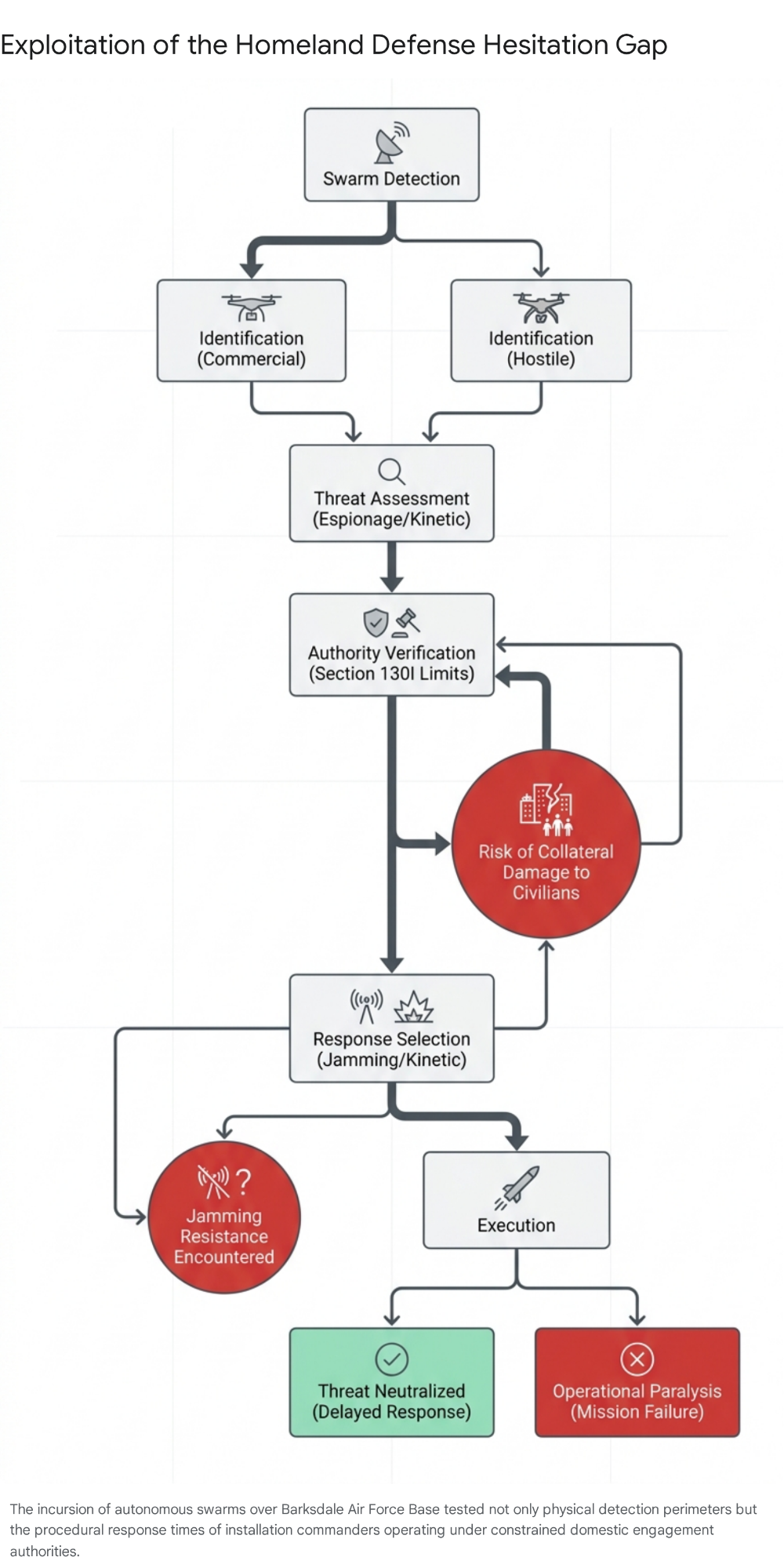

Lesson 1: The Erosion of Strategic Sanctuary and the “Hesitation Gap”

Declassified internal briefings obtained and widely analyzed during this reporting period revealed a highly concerning sequence of events that occurred earlier in the year at Barksdale Air Force Base in Louisiana.47 Between March 9 and March 15, 2026, multiple waves of 12 to 15 sophisticated drones repeatedly swarmed the installation. The drones loitered for hours over highly sensitive areas, including the flight line housing the U.S. Air Force’s B-52 long-range nuclear bombers.47 Base security forces noted that the UAS platforms displayed non-commercial signal characteristics, utilized advanced long-range control links, and demonstrated significant resistance to standard electronic jamming countermeasures.47 The base was forced to issue a base-wide shelter-in-place order during the initial incursions.47

The strategic lesson derived from the Barksdale incursions is that the traditional geographic sanctuary of the continental United States—shielded by two oceans—has been effectively nullified by the proliferation of long-range, autonomous systems.48 Adversaries, operating through gray-zone proxies or utilizing advanced commercial technology, now possess the capability to project non-kinetic, uncrewed power deep into the homeland. More critically, the event exposed the operational paralysis caused by the “hesitation gap.” The drones were likely testing the security response timelines of the installation. Because the drones were operating in domestic airspace, military commanders faced immense bureaucratic and legal friction regarding engagement authorities, compounded by the severe risk of collateral damage if kinetic defeat mechanisms were utilized over a populated area or near nuclear assets.

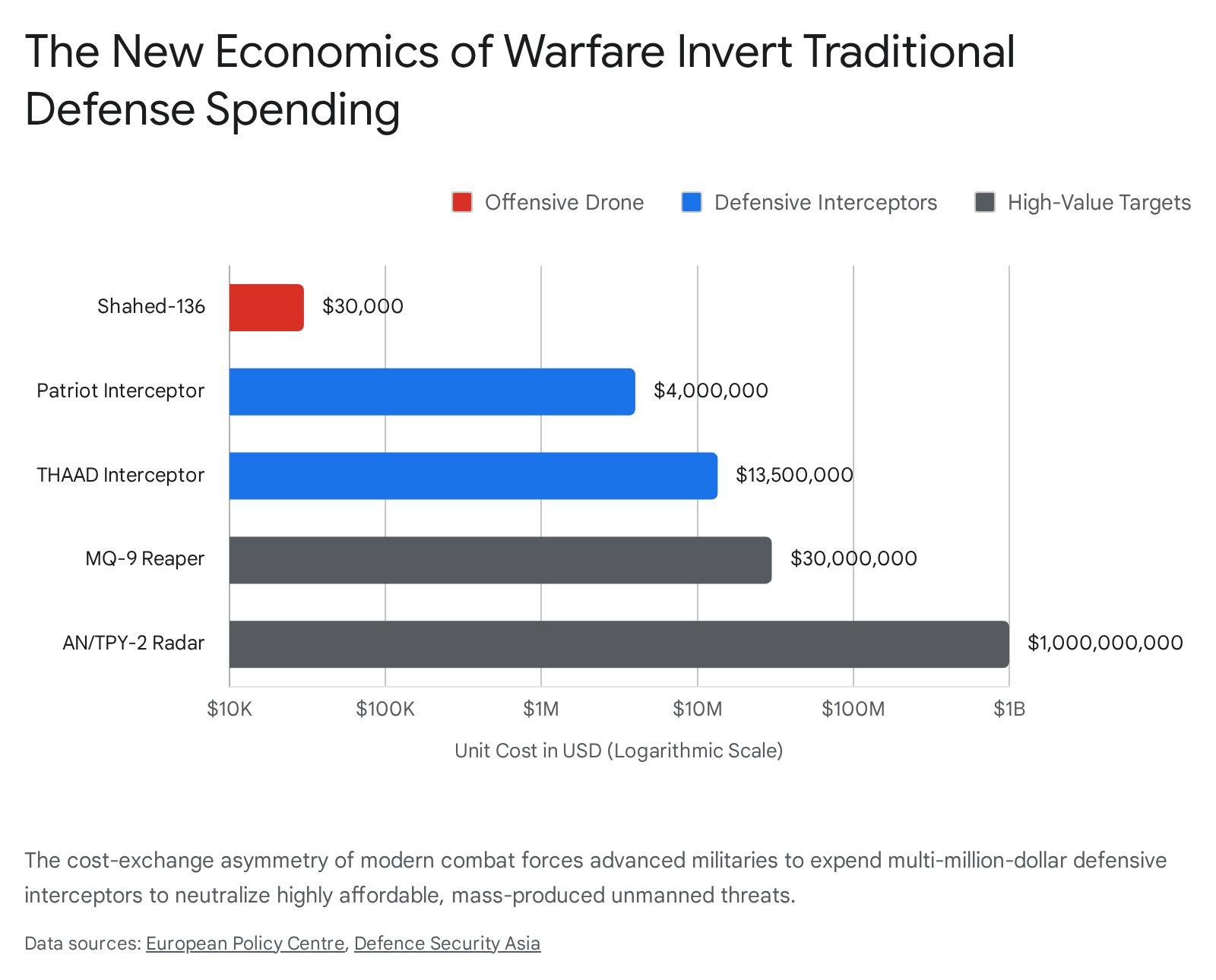

Lesson 2: Reversing the Economic Cost Curve of Air Defense

The necessity of addressing the “hesitation gap” and the threat of massed swarms was the focal point of Operation Clear Horizon, a massive counter-drone exercise recently concluded at Eglin Air Force Base in Florida by the Joint Interagency Task Force 401 (JIATF-401).11 During the exercise, special operations teams playing the role of the adversary utilized advanced, Ukraine-style tactics—deploying Group 1 and Group 3 drones utilizing LTE cellular links, directional antennas, and fiber-optic command wires to evade detection.11

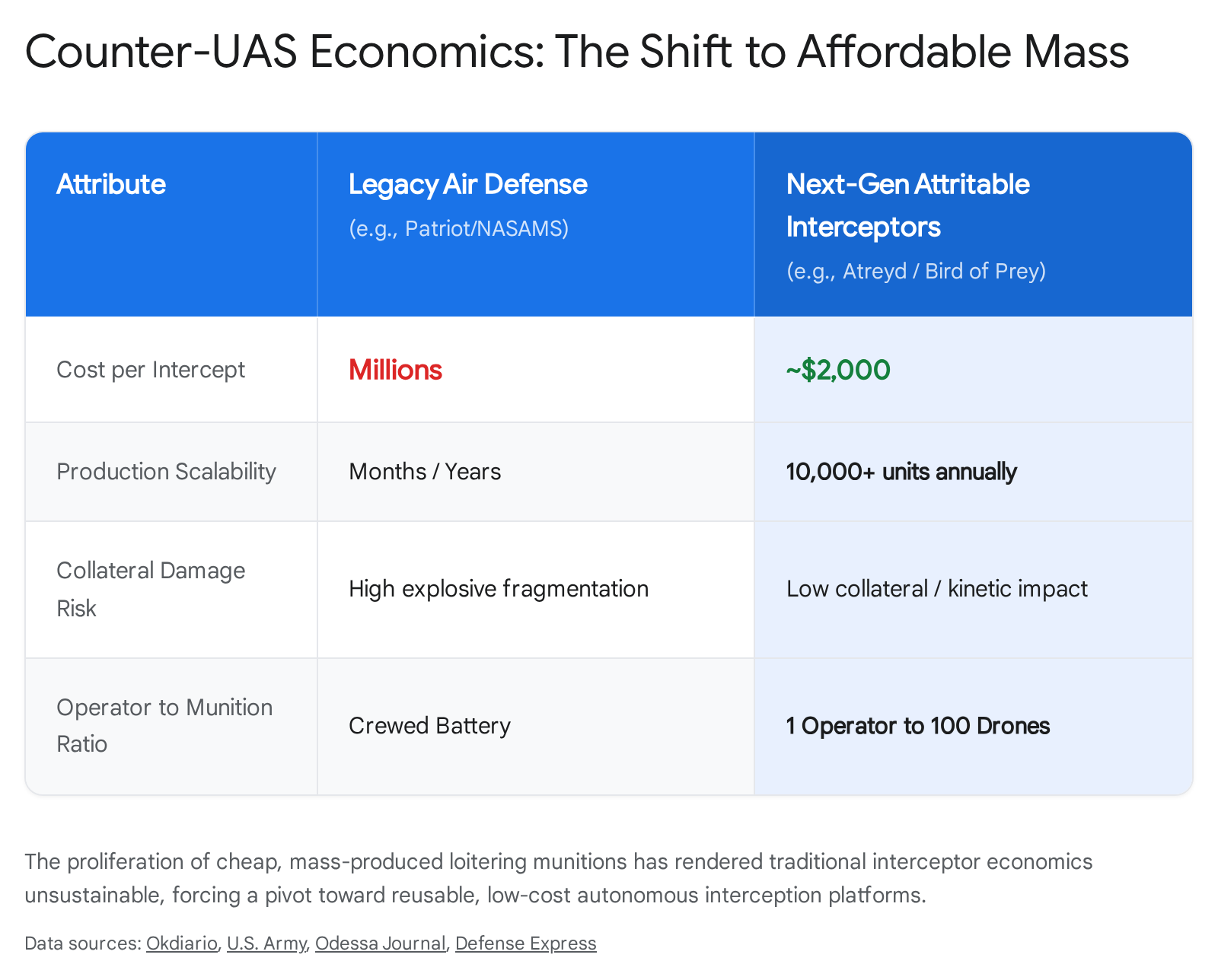

The exercise ruthlessly exposed what military logisticians term the “fly with a laptop” problem. Modern battlefield drones have entirely outpaced traditional, multi-million-dollar air defense assumptions. The U.S. military realized that attempting to defeat $10,000 kamikaze swarms with highly complex, expensive interceptor missiles (such as the Patriot or SM-2) is mathematically and economically unsustainable in a prolonged conflict. During the evaluation of 67 different counter-drone systems, commanders noted that the resulting data was inconsistent, leaving the Pentagon without a clear answer on the most effective defensive tools.11

This realization is driving a rapid, forced shift in strategic procurement toward “Affordable Precise Mass.” Defense acquisitions are aggressively pivoting toward systems like the aforementioned Atreyd Drone Wall, the European-developed Airbus “Bird of Prey,” and Frankenburg Technologies’ Mark I interceptor missile. These next-generation systems are explicitly designed to be manufactured at a massive scale of over 10,000 units annually, costing only a few thousand dollars each. This paradigm shift finally aligns the economics of the defensive architecture with the cheap economics of the offensive swarm threat.11 Furthermore, these smaller, kinetic-impact or low-explosive interceptors address the requirement for “low collateral defeat” options, which are vital for defending domestic infrastructure and civilian populations.11

[Image: Comparative matrix detailing the economic and operational asymmetry between legacy air defense systems and next-generation attritable interceptors.]

Lesson 3: Commercial Space Vulnerabilities in Complex Terrain

From May 5 to May 15, NATO’s Task Force X conducted the Crystal Arrow 2026 exercise in the densely forested Sēlija training area of Latvia. The exercise was historically significant, marking the first large-scale, multinational, brigade-level testing of hundreds of Unmanned Ground Vehicles (UGVs) on the Eastern Flank.6 Participating platforms included the Ukrainian-made Simba UGV, known for its extreme durability and 300-kilogram payload capacity, and the Latvian-made Natrix UGV. Both platforms were utilized heavily for simulated frontline logistics, resupply, and casualty evacuation missions.6

The primary operational lesson derived from the exercise was the severe vulnerability of commercial satellite communications (specifically Starlink networks) when operating in complex woodland environments. Operators reported that beneath the thick, dense canopy of Baltic pine forests, the direct line-of-sight required for high-speed satellite connectivity degraded rapidly.6 This physical interference resulted in frequent loss of control over the robotic platforms. This environmental friction exposes a critical, foundational flaw in current Western UGV doctrine: a reliance on space-based commercial architectures creates a single point of failure in theaters where clear skies are not guaranteed. Consequently, operators were forced to default to medium-range radio linkages and physical fiber-optic cables to maintain control.7 The exercise unequivocally proved the immediate requirement for resilient, multi-modal terrestrial mesh networks that do not rely exclusively on vertical satellite links for ground autonomy to function effectively in European theaters. Furthermore, experts observing the exercise concluded that while the hardware is highly durable, current fully autonomous navigation algorithms remain “nascent” and unready for the messy, unstructured environment of near-peer combat, mandating that a human-in-the-loop remains necessary for the foreseeable future.6

Lesson 4: Software-Defined Forces and Autonomous Frontline Logistics

Speaking at the joint Xponential/MDEX conference in Detroit on May 15, Brig. Gen. Anthony Gibbs provided profound insights into the newly established U.S. Army Capability Program Executive Office for Mission Autonomy (CPE Mission Autonomy).24 The overarching lesson delivered to the defense industrial base is that military autonomy can no longer be procured as an intrinsic, locked feature of an individual vehicle. Instead, the U.S. Army is transitioning completely to acquiring software-defined “packages of capability.”

Rather than buying a specific robotic truck, the Army intends to procure an open-architecture autonomy package that can be modularly integrated across various existing platforms to perform combat engineering, automated fires, or sustained logistics. The ultimate goal is to allow battlefield commanders to task these autonomous systems much like they would a human formation—issuing a broad commander’s intent and allowing the algorithmic “system of systems” to autonomously plan, execute, and dynamically adjust to the shifting terrain and enemy postures.24 A mandatory requirement for future defense contractors is the total abandonment of proprietary interfaces in favor of open Application Programming Interfaces (APIs). This ensures that new sensor payloads, EW countermeasures, and weapons systems can be onboarded and integrated into the fleet in a matter of days, keeping pace with software iteration cycles rather than decades-long hardware acquisition timelines.24

This doctrinal shift toward modular autonomy is currently being validated in the most extreme environment possible. During the reporting period, the Ukrainian Ministry of Defense provided a stark validation of the utility of ground robotics by announcing the procurement of 25,000 UGVs in the first half of 2026—double the total volume procured in the entirety of 2025.51 The strategic objective is to entirely automate 100% of frontline logistics by mid-year.

This monumental shift is a direct, urgent response to the mathematically unsustainable infantry casualty rates suffered during standard resupply and casualty evacuation missions across the gray zones. As one Ukrainian commander grimly noted regarding the shift, “Robots do not bleed”.54 Companies such as ARX Robotics, which is heavily supplying the modular GEREON platform to the Ukrainian armed forces, are enabling military units to push critical supplies and ammunition into heavily contested areas without exposing human soldiers to the lethal combination of FPV drone strikes and pre-sighted artillery fire.51 The overarching lesson for global militaries is clear: logistics, rather than direct kinetic combat engagements, is the most mature, immediate, and high-impact use-case for the mass deployment of ground autonomy.

Lesson 5: The Dawn of Orbital Warfare and Maneuverability

In the space domain, the U.S. Space Force has officially recognized the imperative of “orbital warfare,” marking a definitive end to the era of static space operations. Historically, highly expensive military communications and reconnaissance satellites were placed into static Geosynchronous (GEO) orbits; once fueled and positioned, they remained highly predictable, stationary targets. During recent symposiums, senior leadership including Gen. Chance Saltzman and Gen. Stephen Whiting confirmed a rapid doctrinal pivot toward dynamic maneuverability.55

Under the 15-year “Objective Force” roadmap, the Space Force is aggressively investing in refuelable “space tugs” and commercial satellite platforms capable of executing dynamic maneuvers on command.56 The ability to execute rendezvous and proximity operations (RPO)—the capability to safely approach, closely inspect, or actively shadow an adversary spacecraft—is now a core operational requirement.58 This paradigm shift necessitates the integration of advanced autonomous real-time coordination algorithms, as satellites must receive tasking, interpret the complex orbital threat environment, and execute precision maneuvers without waiting for the highly latency-prone command cycle from terrestrial ground stations.58

Defense contractors are already aligning with this shift; firms like Lockheed Martin and BAE Systems are heavily investing in platforms like the NGSD Vanguard and Sentinel, which feature shared avionics and are explicitly designed for autonomous orbital warfare.58 Consequently, the space domain is definitively transitioning from an architecture of large, expendable, static monoliths to highly resilient, hybrid military-commercial fleets capable of executing both offensive and defensive kinetic maneuvers in orbit.57

Further compressing the decision cycle in space operations, the Pentagon has moved to directly connect commercial space assets to the tactical edge. The ongoing testing of the SkyFi platform by U.S. Special Operations Command (SOCOM) aims to provide ground operators in hostile environments with direct, real-time access to commercial satellite imagery.15 By bypassing the traditional, sluggish intelligence dissemination processes of federal satellites, special operations forces can instantly access up-to-date geospatial intelligence, dramatically increasing mission success rates and survivability when operating against highly mobile adversary targets.15 Furthermore, the integration of platforms like NOVI Space’s GENIE constellation, which brings artificial intelligence processing directly onto the satellite (edge computing in orbit), ensures that vast amounts of raw data are interpreted in space, beaming down only the actionable intelligence required by the warfighter.60

6. Strategic Outlook

The cumulative data and events documented between May 9 and May 15, 2026, confirm without ambiguity that the fundamental character of warfare has altered. Across the air, land, sea, and space domains, the operational advantage has decisively and permanently shifted toward the actor capable of deploying the most adaptable, attritable, and autonomous mass. The successful long-range strikes by Ukraine into the Russian interior, the continued paralysis caused by domestic swarm incursions over U.S. installations, and the rapid fielding of AI-guided drone walls all point toward a future where algorithmic speed dictates battlefield supremacy.

Military organizations and defense industrial bases that fail to immediately adopt open-architecture software models, secure fully independent and multi-modal telemetry networks, and aggressively automate their frontline logistical tails will find themselves economically exhausted by the cost of interception and operationally outmaneuvered by adversaries leveraging the cheap, precise mass of autonomous systems.

Please share the link on Facebook, Forums, with colleagues, etc. Your support is much appreciated and if you have any feedback, please email us in**@*********ps.com. If you’d like to request a report or order a reprint, please click here for the corresponding page to open in new tab.

Sources Used

- Israeli drone strikes kill 4 near Beirut as southern airstrikes kill at least 13, accessed May 16, 2026, https://www.pbs.org/newshour/world/israeli-drone-strikes-kill-4-near-beirut-as-southern-airstrikes-kill-at-least-13

- Russia in Review, May 8–15, 2026, accessed May 16, 2026, https://www.russiamatters.org/news/russia-review/russia-review-may-8-15-2026

- Mobilicom to Engage with Defense and Special Operations Stakeholders at SOF Week 2026, accessed May 16, 2026, https://www.stocktitan.net/news/MOB/mobilicom-to-engage-with-defense-and-special-operations-stakeholders-7qhf8luutywn.html

- SOF Week 2026 Opportunities – Military Embedded Systems, accessed May 16, 2026, https://militaryembedded.com/pages/sof-week-opportunities

- US Military Prepares for the Next War: AI, Swarm Drones & The Indo-Pacific | LANPAC 2026, accessed May 16, 2026, https://www.youtube.com/watch?v=LEl-4w_7qZM

- Ukraine UGV ‘Simba’ rolls out of the shadows in NATO Baltic …, accessed May 16, 2026, https://breakingdefense.com/2026/05/ukraine-ugv-simba-rolls-out-of-the-shadows-in-nato-baltic-exercise/

- In Latvia, military robots roll across a new communication challenge: woodlands, accessed May 16, 2026, https://breakingdefense.com/2026/05/in-latvia-military-robots-roll-across-a-new-communication-challenge-woodlands/

- SOF Week 2026 | May 18-21 2026 | Tampa, Florida – Unmanned Systems Technology, accessed May 16, 2026, https://www.unmannedsystemstechnology.com/events/sof-week/

- Veteran-Built Navigation System Keeps Working When GPS Fails – Military.com, accessed May 16, 2026, https://www.military.com/veteran-built-navigation-system-keeps-working-when-gps-fails

- Innoviz tests LiDAR software to shift self-driving ‘brains’ into sensors, accessed May 16, 2026, https://www.stocktitan.net/news/INVZ/innoviz-technologies-announces-advanced-development-program-z7wtj4yhxmig.html

- The Pentagon copied a Ukrainian-style drone attack in Florida, and …, accessed May 16, 2026, https://okdiario.com/techy/en/the-pentagon-copied-a-ukrainian-style-drone-attack-in-florida-and-the-test-exposed-a-weakness-no-single-weapon-can-fix/4157/

- Ukraine attacks Russia with drones after suffering three days of massive strikes, accessed May 16, 2026, https://www.theguardian.com/world/2026/may/15/ukraine-attacks-russia-with-drones-after-suffering-three-days-of-strikes

- Russia unleashes heaviest wartime drone assault on Ukraine, hits Kyiv, accessed May 16, 2026, https://www.bworldonline.com/world/2026/05/14/749682/russia-unleashes-heaviest-wartime-drone-assault-on-ukraine-hits-kyiv/

- Ukrainian defence giant launches satellites, targets global expansion – Caliber.Az, accessed May 16, 2026, https://caliber.az/en/post/ukrainian-defence-giant-launches-satellites-targets-global-expansion

- The Pentagon Is Transforming U.S. Commercial Satellites Into Tactical Battlefield Infrastructure – FDD, accessed May 16, 2026, https://www.fdd.org/analysis/2026/05/14/the-pentagon-is-transforming-u-s-commercial-satellites-into-tactical-battlefield-infrastructure/

- SOF Week 2026 Returns to Tampa as Acquisition Speed Becomes the Industry Test, accessed May 16, 2026, https://insideunmannedsystems.com/sof-week-2026-returns-to-tampa-as-acquisition-speed-becomes-the-industry-test/

- Ukraine reports strikes on Russian naval vessels in Caspian Sea – Caliber.Az, accessed May 16, 2026, https://caliber.az/en/post/ukraine-reports-strikes-on-russian-naval-vessels-in-caspian-sea

- Ukraine strikes Russian Caspian Fleet base deep inside Russia, home to missile-capable ships used in Kalibr strikes – General Staff – Euromaidan Press, accessed May 16, 2026, https://euromaidanpress.com/2026/05/15/ukraine-strikes-russian-caspian-fleet-base/

- Ukraine’s Refinery Strikes Put New Pressure on Russia’s Oil War Economy, accessed May 16, 2026, https://eutoday.net/ukraines-refinery-strikes-put-new-pressure-on-russias-oil-war-economy/

- Ukrainian Drones Kill 4 and Set Ryazan Oil Refinery Ablaze, accessed May 16, 2026, https://www.themoscowtimes.com/2026/05/15/ukrainian-drones-kill-4-and-set-ryazan-oil-refinery-ablaze-a92760

- Advancing Autonomous Drone Constellations for the US Military – sUAS News, accessed May 16, 2026, https://www.suasnews.com/2026/05/advancing-autonomous-drone-constellations-for-the-us-military/

- Watch Live SpaceX CRS-34 Dragon Launch to ISS + Booster Landing | Falcon 9 from Cape Canaveral – YouTube, accessed May 16, 2026, https://www.youtube.com/watch?v=k-4hSskD4I0

- Falcon 9 – CRS SpX-34 – SLC-40 – Cape Canaveral SFS – May 15, 2026 – YouTube, accessed May 16, 2026, https://www.youtube.com/watch?v=RdCYRAj6PMI

- Army’s autonomy office looks beyond drone, robot platforms to …, accessed May 16, 2026, https://breakingdefense.com/2026/05/armys-autonomy-office-looks-beyond-drone-robot-platforms-to-packages-of-capability/

- The Houthis Strike Israel, Join the Regional Fray – Sana’a Center For Strategic Studies, accessed May 16, 2026, https://sanaacenter.org/publications/perspectives-and-analyses/26703

- Houthis Launch Barrage of Missiles, Drones in Red Sea Attack – TIME, accessed May 16, 2026, https://time.com/6553746/houthis-missiles-launch-drones/

- 3 commercial ships hit by missiles in Houthi attack in Red Sea, US warship downs 3 drones, accessed May 16, 2026, https://apnews.com/article/red-sea-houthi-yemen-ships-attack-israel-hamas-war-gaza-strip-716770f0a780160e9abed98d3c48fbde

- US military says 18 Houthi attack drones, anti-ship missiles shot down over Red Sea, accessed May 16, 2026, https://www.youtube.com/watch?v=y46qbLFAlVY

- Russia strikes across Ukraine leave 7 dead, dozens injured, accessed May 16, 2026, https://www.pbs.org/newshour/world/russia-strikes-across-ukraine-leave-7-dead-dozens-injured

- Massive fire erupts at Russia’s Ryazan oil refinery as Ukrainian drone blitz hits multiple targets, oblasts, accessed May 16, 2026, https://kyivindependent.com/ukrainian-drones-reportedly-strike-oil-refinery-military-airfield-in-multiple-russian-regions/

- Ukraine Strikes Major Russian Refinery, Warships, Ammo Depots, accessed May 16, 2026, https://www.kyivpost.com/post/76227

- General Staff confirms strikes on oil refinery in Ryazan, Russian warships in Kaspiysk, accessed May 16, 2026, https://www.ukrinform.net/rubric-ato/4123762-general-staff-confirms-strikes-on-oil-refinery-in-ryazan-russian-warships-in-kaspiysk.html

- Ukraine hits Russia’s Ryazan oil refinery again – video | Ukrainska Pravda, accessed May 16, 2026, https://www.pravda.com.ua/eng/news/2026/05/15/8034829/

- Russo-Ukrainian war, day 1542: Day of Mourning for 24 in Kyiv. Odradne raises the flag again. 205 Mariupol defenders come home., accessed May 16, 2026, https://euromaidanpress.com/2026/05/15/russo-ukrainian-war-day-1542/

- Seasats Quickfish USV Completes Continuous Eight-Day Sea Trial – PR Newswire, accessed May 16, 2026, https://www.prnewswire.com/news-releases/seasats-quickfish-usv-completes-continuous-eight-day-sea-trial-302715566.html

- Photos Show US Sea Drone’s Encounter With Chinese Aircraft Carrier Group – Newsweek, accessed May 16, 2026, https://www.newsweek.com/us-sea-drone-encounter-chinese-aircraft-carrier-group-2113999

- USV maker Seasats says drone came within meters of Chinese warship during Pacific transit – Breaking Defense, accessed May 16, 2026, https://breakingdefense.com/2025/08/usv-maker-seasats-says-drone-came-within-meters-of-chinese-warship-during-pacific-transit/

- Japan Military UAV and Drone Technology Market, Highlighting, accessed May 16, 2026, https://www.openpr.com/news/4512795/japan-military-uav-and-drone-technology-market-highlighting

- AEVEX Showcasing Autonomous Systems, Launched Effects, Unmanned Platforms, and Additive Manufacturing Capabilities at SOF Week 2026, accessed May 16, 2026, https://aevex.com/aevex-showcasing-autonomous-systems-launched-effects-unmanned-platforms-and-additive-manufacturing-capabilities-at-sof-week-2026/

- What to expect at SOF Week 2026: Bringing autonomous UAS to the tactical edge – Latent AI, accessed May 16, 2026, https://latentai.com/blog/what-to-expect-at-sof-week-2026-bringing-autonomous-uas-to-the-tactical-edge/

- SOF Week 2026 – Emesent, accessed May 16, 2026, https://www.emesent.com/event-detail/sof-week-2026

- A French startup will deploy a “drone wall” in Ukraine to protect against bombs and drones, accessed May 16, 2026, https://odessa-journal.com/a-french-startup-will-deploy-a-drone-wall-in-ukraine-to-protect-against-bombs-and-drones

- Against Shaheds and KABs: Ukraine to Be the First in the World to Test Whether One Operator Can Control 100 Drones | Defense Express, accessed May 16, 2026, https://en.defence-ua.com/weapon_and_tech/against_shaheds_and_kabs_ukraine_to_be_the_first_in_the_world_to_test_whether_one_operator_can_control_100_drones-16465.html

- One Operator, 100 Drones: Ukraine First to Deploy AI-Controlled Drone Wall in Combat, accessed May 16, 2026, https://united24media.com/latest-news/one-operator-100-drones-ukraine-first-to-deploy-ai-controlled-drone-wall-in-combat-13373

- Next-generation Counter-Drone Systems: the Forward Edge of Air Defence – New Geopolitics Research Network, accessed May 16, 2026, https://www.newgeopolitics.org/2025/11/26/next-generation-counter-drone-systems-the-forward-edge-of-air-defence/

- Ukraine deploys world’s first AI drone wall against Russia – Aerospace Global News, accessed May 16, 2026, https://aerospaceglobalnews.com/news/ukraine-ai-guided-drone-wall-russia/

- Unauthorized Drone Swarms Reportedly Fly Over US Base In Louisiana | AllSides, accessed May 16, 2026, https://www.allsides.com/story/defense-and-security-several-drone-swarms-reportedly-fly-over-us-base-louisiana

- The Barksdale Incursion: The End of Strategic Sanctuary – Modern Diplomacy, accessed May 16, 2026, https://moderndiplomacy.eu/2026/04/21/the-barksdale-incursion-the-end-of-strategic-sanctuary/

- Mar 9-15, 2026: Multiple waves of 12-15 sophisticated drones swarmed Barksdale AFB. Lights on, resistant to jamming, loitering for hours. Base called them unauthorized & illegal—likely testing security responses.” Many see it as a foreign probe (China/Russia/Iran axis) showing: we can reach – Reddit, accessed May 16, 2026, https://www.reddit.com/r/AirForce/comments/1s5boo1/mar_915_2026_multiple_waves_of_1215_sophisticated/

- FACT CHECK: Barksdale Drone Incursion – Air Force Global Strike Command, accessed May 16, 2026, https://www.afgsc.af.mil/News/Article-Display/Article/4448052/fact-check-barksdale-drone-incursion/

- European UGV maker sends hundreds more ground robots to Ukraine – The Defence Blog, accessed May 16, 2026, https://defence-blog.com/european-ugv-maker-sends-hundreds-more-ground-robots-to-ukraine/

- Why The US Can’t Adopt Ukraine’s Innovative Approach To Unmanned Warfare Systems, accessed May 16, 2026, https://www.techdirt.com/2026/05/15/why-the-us-cant-adopt-ukraines-innovative-approach-to-unmanned-warfare-systems/

- Ukraine aims to deploy 25000 UGVs for frontline logistics – The Jerusalem Post, accessed May 16, 2026, https://www.jpost.com/defense-and-tech/article-893608

- Ukraine’s robot army will be crucial in 2026 but drones can’t replace infantry, accessed May 16, 2026, https://www.atlanticcouncil.org/blogs/ukrainealert/ukraines-robot-army-will-be-crucial-in-2026-but-drones-cant-replace-infantry/

- Industry awaits Space Force guidance on maneuverable satellite refueling, accessed May 16, 2026, https://aerospaceamerica.aiaa.org/industry-awaits-space-force-guidance-on-maneuverable-satellite-refueling/

- Shifting gears: Space Force moves to embrace space mobility for orbital warfare, accessed May 16, 2026, https://breakingdefense.com/2026/04/shifting-gears-space-force-moves-to-embrace-space-mobility-for-orbital-warfare/

- Space Force Plans 2026 Competition for Commercial Satellites That Can Maneuver, accessed May 16, 2026, https://www.airandspaceforces.com/space-force-2026-competition-maneuverable-commercial-satellites/

- The Pentagon’s Shift to Maneuverable Satellites Is Reshaping Who Wins Defense Space Contracts – Copernical, accessed May 16, 2026, https://www.copernical.com/news-public/item/57491-2026-04-15-11-55-16

- Space Force refines ‘orbital warfare’ maneuvers with new prototype – Task & Purpose, accessed May 16, 2026, https://taskandpurpose.com/news/space-force-orbital-warfare-training-satellite/

- The Promise of smart satellites – Apogee Magazine, accessed May 16, 2026, https://apogee-magazine.com/features/the-promise-of-smart-satellites/