1. Executive Summary

The initiation of Operation Epic Fury on February 28, 2026, by the United States and Israel marked a profound watershed moment in modern Middle Eastern geopolitics and global security architecture. Designed as a decisive, overwhelming military campaign to definitively neutralize Iran’s nuclear infrastructure and decapitate its senior political and military leadership—including the successful assassination of Supreme Leader Ali Khamenei—the operation has achieved significant, albeit narrow, tactical and kinetic objectives. However, the resulting strategic blowback has precipitated an unprecedented, cascading global crisis. Iran’s calculated transition to a multidomain retaliation strategy, most notably the effective weaponization and closure of the Strait of Hormuz, has transformed a regional military conflict into a systemic shock to the foundation of the global economy.

This comprehensive intelligence and diplomatic assessment analyzes the compounding, multifaceted effects of the 2026 Iran conflict on global perceptions of the United States. The analysis indicates that while the United States retains overwhelming conventional military supremacy and strike capability, its global soft power, diplomatic leverage, and alliance cohesion are experiencing a precipitous and potentially irreversible decline. The blockade of the Strait of Hormuz has disrupted approximately 20% of global seaborne energy trade, triggering severe inflationary shocks across global energy, petrochemical, and agricultural markets. Consequently, the United States is increasingly viewed by traditional European allies, Indo-Pacific partners, and the broader Global South not as a reliable guarantor of international stability, but as the primary architect of a disruptive conflict that places disproportionate economic and humanitarian burdens on vulnerable nations.

Furthermore, the ongoing crisis has rapidly accelerated the structural realignment of the international order. The geopolitical vacuum created by U.S. entanglement, coupled with the alienation of key European and Asian allies over economic fallout, has provided an explicit opening for systemic rivals—namely China and Russia—to consolidate their influence. By capitalizing on the global energy squeeze, capturing disrupted supply chains, and offering diplomatic alternatives, this emerging alignment is successfully positioning itself against U.S. unipolar hegemony. Concurrently, Iran has demonstrated a highly effective asymmetric warfare doctrine, leveraging proxy militias across multiple theaters, conducting aggressive cyber-enabled psychological operations, and exploiting the vulnerabilities of global commercial infrastructure to impose unacceptable costs on the U.S. and its partners. This report details the economic, diplomatic, and security dimensions of the crisis, concluding that the 2026 Iran conflict has fundamentally challenged the authority of the United States, forcing a systemic reevaluation of American strategic reach and the durability of its alliance networks in an increasingly fragmented, multipolar world.

2. The Strategic Context and the Architecture of Escalation

The roots of the current crisis are deeply embedded in the collapse of the Joint Comprehensive Plan of Action (JCPOA) and the subsequent years of oscillating U.S. policy, which vacillated between “maximum pressure” containment strategies and direct, albeit limited, military coercion.1 The immediate catalyst for the current conflagration emerged following the failure of mediated, backchannel negotiations in Oman, Rome, and Geneva throughout 2025, a diplomatic breakdown that culminated in the brief but highly destructive Twelve-Day War in June 2025.2 Assessing Iran’s strategic posture as severely weakened by years of crippling economic sanctions, destabilizing domestic unrest, and the steady degradation of its proxy networks during the preceding Israel-Hamas War, the United States and Israel calculated that overwhelming military intervention presented a highly viable mechanism to permanently neutralize Tehran’s nuclear ambitions and regional influence.2

On February 28, 2026, joint U.S. and Israeli forces launched Operation Epic Fury, executing nearly 900 precision airstrikes within the first 12 hours of the conflict.2 The strikes systematically dismantled Iranian air defenses, military infrastructure, and known nuclear sites, whilst successfully targeting the heart of the Iranian regime.2 The assassination of Supreme Leader Ali Khamenei, alongside key figures such as Ali Larijani—who had historically served as a critical backchannel negotiator with the West—was intended to precipitate rapid regime collapse or, at minimum, severe operational paralysis.2 However, the deeply entrenched institutional networks and redundant command structures of the Islamic Republic endured the initial kinetic shock. Rather than capitulating, Tehran opted for a highly calculated, multidomain punishment campaign.7

Recognizing its inherent inability to match U.S. and Israeli conventional firepower or sustain a prolonged conventional war, Tehran operationalized a strategy of asymmetric horizontal escalation. By early March 2026, Iran had executed retaliatory strikes against U.S.-linked energy infrastructure across nine Gulf Cooperation Council (GCC) states and, most consequentially, imposed a near-total blockade on commercial shipping through the Strait of Hormuz.5 This strategic pivot purposefully shifted the center of gravity from the military battlefield to the global economic system, leveraging the inherent structural vulnerabilities of interconnected supply chains to exert massive, decentralized political pressure on Washington.8

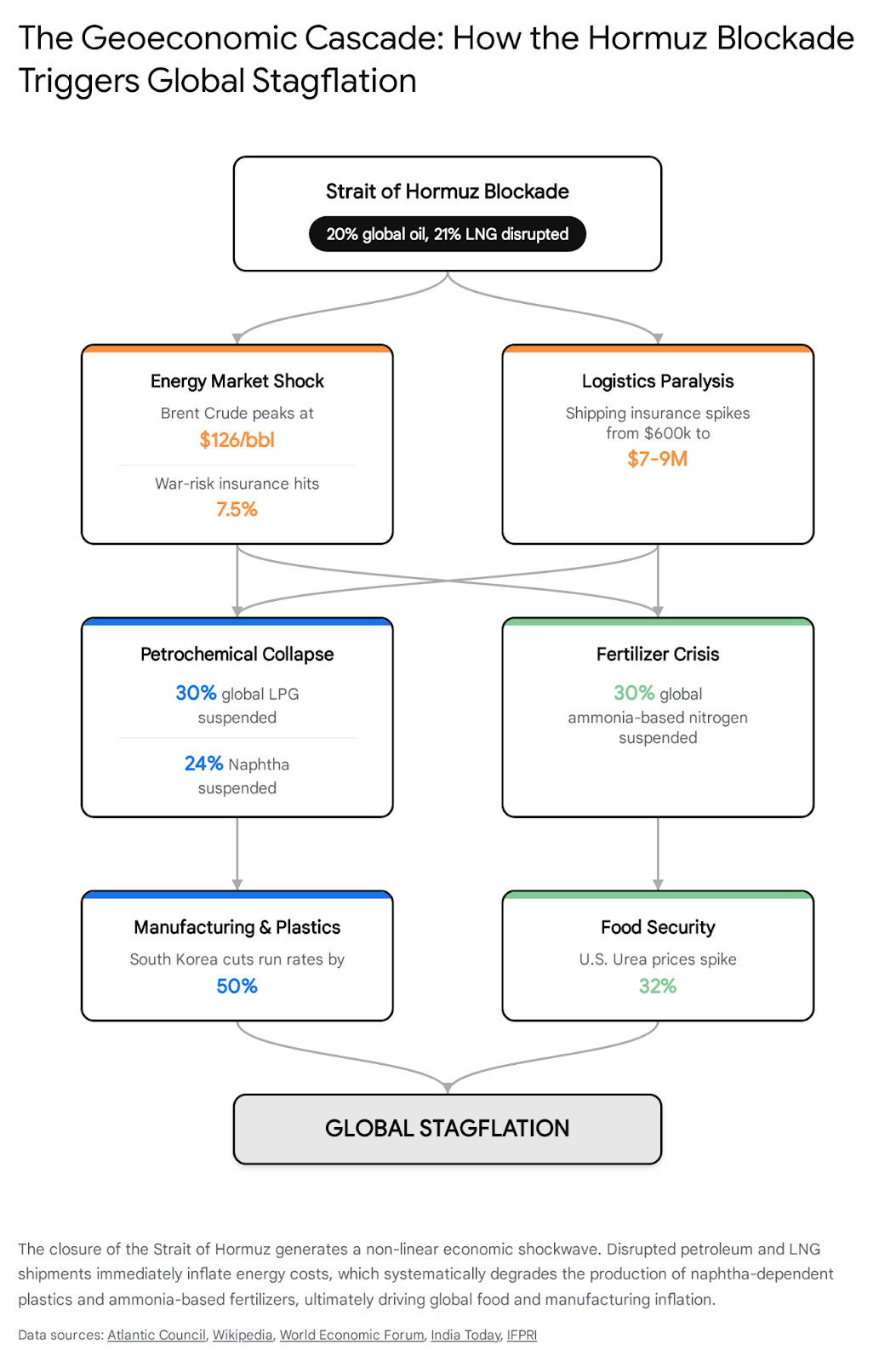

3. The Geoeconomic Cascade: The Weaponization of the Strait of Hormuz

The closure of the Strait of Hormuz represents the single most consequential supply chain disruption in modern economic history, dwarfing both the oil shocks of the 1970s and the energy realignments following the 2022 Russia-Ukraine war.9 By targeting the world’s premier maritime chokepoint, Iran has effectively removed approximately 20 million barrels per day (bpd) of petroleum liquids and 21% of global Liquefied Natural Gas (LNG) supplies from the market.12 International Energy Agency (IEA) Executive Director Fatih Birol has characterized the event as the equivalent of two historical oil crises and one gas crisis occurring simultaneously, representing a catastrophic supply disruption that markets and policymakers have yet to fully internalize.12

3.1. The Energy Core and the Weaponization of Marine Insurance

Following the initiation of hostilities and Iran’s official declaration of a maritime blockade for all “belligerent” nations, energy markets reacted with unprecedented volatility. Brent crude oil prices breached the $100 per barrel threshold within days, ultimately peaking at $126 per barrel by early March, signaling a shift from conflict-driven short-term spikes to real, enduring constraints on global supply.9 While strategic reserves were tapped—including a record 400 million barrel coordinated release coordinated by the IEA—these measures provided only temporary relief against deep structural supply constraints.12 The conflict also resulted in the loss of roughly 140 billion cubic meters (BCM) of natural gas to the global market, nearly double the volume lost to Europe during the onset of the Ukraine conflict.15

The primary mechanism of this economic disruption relies heavily on the weaponization of marine insurance, a paradigm-shifting tactic in irregular warfare that Iran refined after observing Houthi operations in the Red Sea.10 Iran achieved systemic economic disruption without needing to physically sink a vast armada of vessels. Instead, by conducting 21 confirmed kinetic attacks on merchant ships and deploying sea mines, Tehran forced the global insurance industry to radically reprice maritime risk.9 War-risk premiums skyrocketed from standard rates of 0.25% to between 3% and 7.5%.17 For a large oil tanker valued at $200–$300 million, insurance costs per voyage surged from approximately $600,000 to up to $9 million, severely degrading the profitability of the route, pushing freight costs to unsustainable levels, and causing commercial shipping to slow to a trickle.13

3.2. First-Order Industrial Impacts: Petrochemicals and Manufacturing

The energy shock rapidly metastasized into the petrochemical sector, which serves as the foundational feedstock for global plastics and manufacturing. The Middle East traditionally supplies 30% of global seaborne liquefied petroleum gas (LPG) and 24% of seaborne naphtha—both of which are absolutely vital inputs for petrochemical production.11 With these exports cut off from global markets, downstream facilities across Asia faced immediate existential threats. South Korean petrochemical producers, highly reliant on Middle Eastern naphtha, were forced to cut run rates by up to 50% within weeks of the blockade.11

In addition to direct feedstock shortages, the disruption of LNG supplies forced immediate electricity rationing in East Asian democracies, including Japan, South Korea, and Taiwan. Governments in these nations have been compelled to make difficult industrial choices, frequently prioritizing electricity for high-value semiconductor manufacturing and artificial intelligence hardware over energy-intensive petrochemical production, further exacerbating the global plastics shortage.11 This dynamic has triggered broad price increases across virtually every manufactured good. The impact is particularly acute for U.S. consumers, who utilize an average of 255 kilograms of new plastics annually, compared to the global average of 60.1 kilograms, rendering the U.S. domestic market highly vulnerable to packaging and medical supply cost inflation.11

3.3. The Agricultural Crisis: Fertilizers and Global Food Security

Perhaps the most devastating and enduring secondary effect of the Hormuz closure is its impact on global agriculture. The Strait is a vital, irreplaceable conduit for 20% to 30% of globally traded fertilizers, including urea, ammonia, phosphates, and sulfur.14 The blockade immediately suspended roughly 30% of globally traded ammonia-based nitrogen fertilizer, plunging the Northern Hemisphere into profound uncertainty ahead of the spring planting season.11

In the United States, which imports approximately half of its domestic urea, prices at the New Orleans import hub surged 32% in a single week, leaping from $516 to $683 per metric ton.11 For the Global South, the situation is increasingly catastrophic. The United Nations Food and Agriculture Organization (FAO) warned that the disruption threatens global agrifood systems by raising production costs, tightening supply, and ensuring persistent food price volatility.20 Farmers face a dire economic calculus: higher input costs for fertilizer and diesel are directly disincentivizing the planting of nitrogen-intensive crops like corn, which will inevitably lead to lower yields, higher livestock feed costs, and severe food inflation for consumers worldwide.11

In developing nations, the secondary effects are already highly visible. In Tanzania, vital shipping routes for avocado exports to the Gulf are blocked, causing immense financial strain on local horticulture.21 In Mombasa, Kenya, warehouses are overflowing with tea unable to reach markets in Pakistan and the Middle East, forcing smallholder farmers to accept prices 50% below standard rates.21 In India, the Restaurant Association of India reports that severe commercial LPG shortages have forced widespread menu shrinking, altered cooking methods, and reduced operating hours across its half-million member establishments.22

| Economic Sector | Key Metric of Disruption | Primary Global Consequence |

| Crude Oil & LNG | 20M bpd oil and 21% global LNG suspended. Brent crude peaks at $126/bbl. | Systemic energy inflation; electricity rationing in East Asia; increased war-risk insurance premiums up to 7.5%. 9 |

| Petrochemicals | 30% global seaborne LPG and 24% naphtha disrupted. | South Korean run rates cut by 50%; global plastics shortage; massive supply chain cost increases for U.S. consumers. 11 |

| Agriculture | 30% globally traded ammonia-based nitrogen fertilizer blocked. | U.S. urea prices surge 32%; lower global crop yields expected; severe supply chain bottlenecks for African agricultural exports. 11 |

4. Shifting Global Perceptions: The Decline of American Soft Power and Alliance Cohesion

The profound economic pain radiating from the Middle East has fundamentally altered the global perception of the United States. While Operation Epic Fury was framed by Washington as a necessary defensive measure designed to eliminate a persistent regional threat and curtail a critical nuclear proliferation risk, the international community increasingly views the U.S. action as a reckless strategic miscalculation that has severely endangered global welfare.23 The perception of American leadership is actively transitioning from that of a stabilizing hegemon to an unpredictable actor whose domestic political imperatives and bilateral commitments consistently supersede the economic security of its broader alliance network.24

4.1. The Fracturing of Western Alliances and the “Lonely Superpower” Narrative

The diplomatic rift between the United States and its traditional Western allies has reached historic, debilitating depths. European leaders, facing an energy model still heavily reliant on external imports and critically lacking the spare capacity that mitigated the 2022 energy crisis, are bearing the brunt of the Hormuz closure.25 Gas prices in Europe have nearly doubled, exposing the persistent fragility of the continent’s energy security and forcing uncomfortable debates regarding the continent’s ambitious climate targets versus immediate economic survival.25 Katherina Reiche’s recent public remarks highlighting that Europe may have overestimated sustainability while underestimating affordability reflect a deep, systemic anxiety spreading across European capitals.25

In response to the crisis, the European Union and the United Kingdom have explicitly prioritized diplomatic de-escalation over military solidarity with Washington. The UK offered to host an international security summit to establish a collective plan for reopening the Strait, but the agenda explicitly focused on diplomatic pressure and technical measures—such as deploying minesweeping drones—rather than joining a U.S.-led offensive naval coalition, which many Western nations rejected.27 German Defense Minister Boris Pistorius summarized the continental frustration, stating bluntly, “This is not our war, and we didn’t start it”.24 Furthermore, public reprimands between President Trump and UK Prime Minister Keir Starmer over London’s strict insistence on a “de-escalation first” approach highlight a historic low in transatlantic security cooperation.24 The United States finds itself increasingly isolated from its operational core, earning the diplomatic moniker of the “Lonely Superpower”.24

4.2. The Collapse of U.S. Soft Power: Global and Domestic Polling Metrics

The geopolitical isolation is reflected in a devastating collapse of American soft power globally. Although the 2026 Brand Finance Global Soft Power Index still ranked the United States at number one (narrowly leading China by 1.4 points with a score of 74.9), this metric captures historical momentum rather than the acute, real-time deterioration occurring since the war’s outbreak.28 More immediate public opinion metrics present a starkly different reality that is deeply concerning for U.S. strategic planners.

A landmark Politico/Public First poll released in mid-March 2026 revealed that public sentiment toward the United States has plummeted to historic lows across allied nations. In Germany, trust in American leadership cratered to a mere 24%, while in Canada, a staggering 57% of respondents now view China as a more reliable global partner than the United States.24 When a plurality of citizens in traditional allied capitals—including London and Paris—view U.S. foreign policy as a greater threat to systemic stability than the adversaries Washington claims to deter, the moral authority required to sustain unipolar leadership evaporates.24 Additional Lowy Institute polling confirms that only 25% of Australians hold confidence in the U.S. President to handle international affairs.30

Domestically, the American public exhibits deep skepticism regarding the utility and management of the conflict. An AP-NORC poll found that 59% of Americans believe U.S. military action in Iran has been excessive, and only a quarter of the public trusts the administration’s handling of foreign policy and the use of military force.31 Furthermore, the conflict is highly polarized along partisan lines. According to Pew Research and YouGov polling, 83% of Democrats and 64% of Independents believe the U.S. will suffer from the war, whereas 52% of Republicans (and 65% of MAGA-aligned Republicans) believe the U.S. will benefit.33 Despite partisan divisions regarding the justification for the war, 45% of all Americans are deeply concerned about the rising cost of gasoline, highlighting the severe domestic political vulnerabilities tied to the international energy crisis.32 A Quinnipiac University poll corroborates this, indicating that 54% of voters oppose the U.S. military action, with a vast divide between Republicans (86% support) and Democrats (92% oppose).34

| Polling Organization / Source | Demographic / Region | Key Finding on U.S. Action & Leadership (March 2026) |

| Politico / Public First | Germany (Public) | Trust in American global leadership has fallen to 24%. 24 |

| Politico / Public First | Canada (Public) | 57% view China as a more reliable global partner than the U.S. 24 |

| Lowy Institute | Australia (Public) | Only 25% hold confidence in the U.S. President’s international leadership. 30 |

| AP-NORC | U.S. (General Public) | 59% state U.S. military action in Iran has been “excessive.” 32 |

| YouGov / The Economist | U.S. (Democrats) | 83% assess that the United States will ultimately suffer from the war. 33 |

| Quinnipiac University | U.S. (Independents) | 64% oppose U.S. military action; 49% say it makes the world less safe. 34 |

4.3. The Global South and Non-Aligned Diplomatic Resistance

The sentiment in the Global South is characterized by acute frustration and a formalization of diplomatic resistance against U.S. actions. During an emergency session of the UN Security Council convened at the request of French President Emmanuel Macron, the international response was starkly divided. While U.S. Ambassador Mike Waltz aggressively defended the operation as a necessary response to long-standing security threats posed by Iran and vital for protecting maritime commerce, the broader Council issued widespread warnings regarding the risk of a catastrophic regional war.23

The Group of 77 (G77) and the Non-Aligned Movement have strongly condemned the breach of sovereignty, framing the conflict through the lens of economic imperialism. The UN adopted Resolution 2817 (2026), heavily co-sponsored by nations of the Global South, calling for an immediate halt to unauthorized military strikes, highlighting a collective conscience that sharply diverges from Washington’s narrative.35 UN experts further denounced the aggression as a flagrant violation of international law that risks setting a precedent for total impunity by military powers.36 For the nations of Africa, Latin America, and South Asia, the war is viewed not as a necessary security operation, but as a wealthy nations’ conflict whose economic fallout—particularly the fertilizer and food security crisis—is being violently outsourced to the developing world.21

5. Strategic Realignments: The Consolidation of the China-Russia-Iran Axis

As the United States expends vast military resources and invaluable diplomatic capital in the Middle East, its systemic global rivals are rapidly maneuvering to exploit the geopolitical vacuum. The conflict has provided a powerful catalyst for the consolidation of an alternative global architecture, driven primarily by China and Russia, who are effectively capitalizing on the non-aligned hedging strategies of the Global South to undermine U.S. influence.

5.1. The Operationalization of the “Axis of Autocracy”

The 2026 crisis has accelerated the practical operationalization of the so-called “Axis of Autocracy”.38 For China and Russia, the U.S. entanglement in Iran is a massive strategic windfall. Beijing and Moscow have highly coordinated their diplomatic messaging, officially condemning the U.S. military strikes, urging an immediate return to diplomacy, and warning against the “vicious cycle” of force that threatens the entire region with chaos.39 Chinese Foreign Ministry spokespersons Lin Jian and Mao Ning have repeatedly stressed that the conflict should never have begun, casting China as the responsible, stabilizing adult in the room relative to an erratic Washington.39

However, behind the public diplomatic rhetoric of restraint, Beijing and Moscow are actively securing tangible geopolitical advantages. Prior to the conflict, China, Russia, and Iran signed a trilateral strategic pact, aligning on issues of military coordination, nuclear sovereignty, and resistance to unilateral Western coercion.43 While China has carefully avoided formal defense treaty commitments that would mandate direct military intervention on Tehran’s behalf—preferring to play a long game—it has provided vital, undeniable dual-use technological support to the Iranian regime.38 Intelligence reports indicate that Chinese ports facilitated the loading of sodium perchlorate—a critical component in solid rocket fuel for ballistic missiles—onto Iranian state-owned vessels shortly after U.S. strikes began.38 Furthermore, China remains Iran’s largest trading partner, purchasing roughly 90% of Iran’s exported oil, providing the financial lifeline necessary for Tehran to sustain its war effort and proxy networks.38

Russia’s involvement is similarly calculated. U.S. intelligence indicates that Moscow is providing Iran with high-resolution satellite imagery and critical intelligence regarding the locations of American warships, aircraft, and allied assets in the region.37 Iranian Foreign Minister Abbas Araghchi has conspicuously declined to deny these reports, indicating a deep level of operational integration between Moscow and Tehran.37

5.2. Economic Windfalls for Beijing and Moscow

Economically, the crisis serves Chinese and Russian strategic interests by fundamentally restructuring global commodity markets in their favor. With the Middle Eastern petrochemical and fertilizer sectors paralyzed by the Hormuz closure, China and Russia are poised to gain immense, enduring leverage.11

China’s domestic polyvinyl chloride (PVC) industry, which relies heavily on a coal-based production process rather than the imported naphtha utilized by Western and allied Asian competitors, is completely insulated from the Hormuz shock.11 Consequently, China, which already accounts for 78% of global incremental PVC capacity additions, is moving rapidly to consolidate and dominate global capacity as its competitors are forced to shut down.11 Concurrently, Russia, as the world’s largest fertilizer exporter, alongside its close ally Belarus (a major potash producer), is massively expanding its geopolitical influence over global agricultural and food supply chains as competing Middle Eastern exports vanish from the market.11 Furthermore, Beijing is accelerating its pivot toward secure, overland energy supplies from Russia, reinvigorating projects such as the Power of Siberia 2 pipeline to permanently insulate its economy from U.S.-controlled or volatile Middle Eastern maritime routes.37

6. The Multipolar Dilemma: BRICS+ Paralysis and the Global South’s Search for Autonomy

The expanded BRICS+ coalition—comprising Brazil, Russia, India, China, South Africa, Egypt, Ethiopia, Iran, Saudi Arabia, and the UAE—finds itself deeply divided by the conflict, a situation that perfectly illustrates both the severe limits and the disruptive potential of the bloc.46

6.1. Internal Divisions and Institutional Paralysis

Iran, aggressively leveraging its recent 2024 accession to the group, actively lobbied India—the 2026 BRICS chair—to issue a unified, forceful condemnation of the U.S.-Israeli military campaign.47 However, the inclusion of Gulf states like the UAE and Saudi Arabia, both of which have been directly targeted by Iranian retaliatory strikes as part of Tehran’s horizontal escalation, has completely paralyzed the bloc’s consensus mechanisms.47 Multiple draft statements condemning the United States and Israel have been vetoed internally by the Gulf states, rendering the institution functionally mute during one of the most significant geopolitical crises of the decade.47 This silence has led to intense criticism from figures like former Indian Foreign Secretary Shivshankar Menon, who labeled the failure to condemn the attacks as “inexplicable” and damaging to the bloc’s credibility.48

6.2. India’s Balancing Act and the “Friendly Nations” Exemption

Despite the institutional paralysis of BRICS+, individual member states are aggressively pursuing strategic autonomy to protect their domestic economies. India faces profound economic and national security risks, importing 40-50% of its crude oil through the Strait of Hormuz.49 Prime Minister Narendra Modi’s government has been forced into a frantic balancing act, scrambling to tap 41 different nations to diversify energy supplies, reduce vulnerabilities, and mitigate domestic fuel inflation ahead of peak summer electricity demand.50

Tellingly, Iranian backchannel diplomacy explicitly exploited this vulnerability by granting a “friendly nations” status to India, China, Russia, Pakistan, and Iraq. Iranian Foreign Minister Abbas Araghchi announced that vessels from these nations would be permitted safe passage through the contested strait, provided they coordinated with the IRGC.52 This calculated move was explicitly designed to drive a wedge between the Global South and Western alliances, rewarding non-alignment while punishing nations that participate in U.S. sanction regimes or military coalitions.52

6.3. Secondary Shocks in Africa and Latin America

The ripple effects of the crisis are devastating emerging economies across the Global South. Sri Lanka, which imports 90% of its oil and gas through Hormuz and is still recovering from its 2022 economic collapse, witnessed an immediate 8% rise in retail fuel prices. The government was forced to declare Wednesdays a public holiday to conserve fuel and reinstituted a stringent QR code rationing system for vehicles.49

In Africa, the power vacuum created by Western distraction in the Middle East has allowed Iran to solidify its presence. Iranian diplomatic “alumni” networks in the Sahel have quickly shifted from soft-power representatives to providing vital logistical support for arms deliveries and safe houses.54 These Iranian personnel, often operating under the guise of engineering contractors, are actively integrating with elite units such as Burkina Faso’s Cobra forces, further destabilizing regions already prone to conflict and diminishing U.S. influence.54 Meanwhile, in Latin America, the U.S. has been forced to reconsider its stance on heavily sanctioned states like Venezuela, with discussions emerging regarding the potential to unlock Venezuelan crude reserves to offset Middle Eastern losses, exposing the contradictions in U.S. global energy strategy.55

7. Indo-Pacific Security: The Extreme Vulnerability of U.S. Asian Allies

The geopolitical shockwaves are perhaps felt most acutely by U.S. allies in the Indo-Pacific, who view the conflict unequivocally as an “Asian crisis” due to their overwhelming structural dependence on Middle Eastern crude.56 In 2025, the Asian continent relied on the Middle East for 59% of its total crude imports, making the Hormuz blockade an existential economic threat.57

7.1. Economic Emergencies in Seoul, Tokyo, and Manila

South Korea, facing severe shortages of the naphtha required to keep its massive industrial base functioning, shifted rapidly into “emergency mode.” President Lee Jae Myung ordered the establishment of dual economic control towers—one at the Presidential Office and another led by Prime Minister Kim Min-seok—to manage supply shocks.58 Seoul instituted drastic fuel rationing measures, including a five-day rotation system for public vehicles based on license plates, and deployed a 100 trillion won ($66.5 billion) market stabilization fund.58

The Philippines was forced to declare a formal national energy emergency, citing an “imminent danger of a critically low energy supply,” authorizing extraordinary procurement measures.27 In Japan, Prime Minister Sanae Takaichi and the Ministry of Economy, Trade, and Industry established specialized task forces to comprehensively review the nation’s entire petroleum supply chain, bracing for severe knock-on effects across the broader economy.56

7.2. U.S. Diplomatic Reassurance and Its Limits

To mitigate the escalating anxiety and prevent strategic decoupling among its Pacific partners, the U.S. State and Commerce Departments rapidly organized the Indo-Pacific Energy Security Ministerial and Business Forum in Tokyo.61 Led by figures such as U.S. Interior Secretary Doug Burgum, the summit successfully generated $57 billion across 22 deals with U.S. companies to secure alternative energy (LNG, coal, nuclear) and critical mineral supplies for Asian allies.61

However, while these long-term investments and purchase commitments signal a strong U.S. desire to maintain alliance cohesion and compete with China’s mineral dominance, they do remarkably little to resolve the immediate, acute shortages currently plaguing Asian economies.63 Regional leaders remain highly skeptical of Washington’s immediate crisis management capabilities, recognizing that the U.S. cannot physically replace 20 million bpd of oil overnight, leaving them exposed to the whims of the Iranian blockade.63

8. The Multidomain Battlespace: Proxy Activation and Cyber-Psychological Operations

Iran’s strategic response to Operation Epic Fury demonstrates a highly sophisticated, evolved understanding of modern multidomain warfare. Unable to defeat the U.S. Navy or Air Force in direct conventional combat, the Islamic Revolutionary Guard Corps (IRGC) has deployed a comprehensive “punishment campaign” designed specifically to hold civilian infrastructure, global commerce, and regional stability at constant risk until the U.S. is forced to capitulate.8

8.1. Reconstitution and Escalation of the Axis of Resistance

Despite suffering severe leadership decapitation and significant infrastructure degradation during the initial U.S.-Israeli bombardment, Iran’s decentralized proxy network—the “Axis of Resistance”—remains a formidable, resilient asymmetric threat capable of inflicting widespread damage.

- Lebanese Hezbollah: Anticipating the conflict, Israel conducted preemptive strikes on Hezbollah weapons depots, tunnel shafts, and intelligence infrastructure in southern Lebanon on February 28.64 However, Hezbollah fully entered the war on March 2, launching coordinated drone and missile attacks into northern Israel. Crucially, intelligence indicates Hezbollah may have also expanded the theater by launching a drone attack against a British airbase in Cyprus, threatening European assets directly.65

- The Houthis (Ansar Allah): Operating with a high degree of strategic autonomy, the Houthis immediately resumed attacks on U.S. and Israeli-flagged shipping in the Red Sea and Gulf of Aden within hours of Operation Epic Fury commencing, demonstrating a pre-positioned response that required no command authorization from a paralyzed Tehran.66 Intelligence assessments indicate the Houthis are now preparing to escalate horizontally by targeting Emirati or U.S. military positions in the Horn of Africa if the conflict prolongs.65

- Popular Mobilization Forces (PMF): In Iraq, Iranian-aligned militias, particularly Kataib Hezbollah—which represents Iran’s deepest structural penetration of a neighboring state—have escalated direct attacks against U.S. forces and diplomatic facilities in the Iraqi Kurdistan Region.65 They have explicitly threatened to expand operations against any regional nation that continues to host U.S. troops, utilizing extortion to fracture the GCC’s cooperation with Washington.65

8.2. Cyber Warfare and Psychological Operations

The kinetic battlefield has been tightly synchronized with an aggressive, highly disruptive Iranian cyber warfare campaign. The U.S. Department of Justice, alongside cybersecurity firms like Resecurity and Palo Alto Networks, report that the conflict immediately transitioned into a multi-domain phase involving sophisticated data wiping, DDoS attacks, and critical infrastructure sabotage.68

Iranian-aligned threat actors, notably the Ministry of Intelligence and Security (MOIS) front known as “Handala Hack,” executed destructive malware attacks against U.S. multinational medical technology firms (such as Stryker) and leaked sensitive PII of Israeli Defense Force personnel.68 In a particularly concerning psychological operation, Handala Hack claimed to have stolen 851 gigabytes of confidential data from members of the Sanzer Hasidic Jewish community, using the data to issue explicit death threats and incite real-world violence.68

Simultaneously, the “Cyber Islamic Resistance”—a pro-Iranian umbrella collective coordinating groups like RipperSec and Cyb3rDrag0nzz—launched synchronized operations targeting Israeli drone defense systems, payment infrastructure, and municipal water facilities.70 Multiple news websites and religious applications, such as the BadeSaba app, were hijacked to display anti-Western propaganda.71 These cyberattacks function primarily as psychological operations, aiming to degrade Western civilian morale, amplify narratives of Israeli and American vulnerability, and stoke domestic opposition to the war by demonstrating that no network is secure.8

| Threat Actor / Group | Domain | Primary Targets / Actions (March 2026) | Strategic Objective |

| Lebanese Hezbollah | Kinetic / Proxy | Northern Israel; suspected drone strike on British airbase in Cyprus. 64 | Horizontal escalation; threatening European assets to force diplomatic intervention. |

| The Houthis | Kinetic / Maritime | Resumed Red Sea shipping attacks; threatening Horn of Africa U.S. positions. 65 | Economic disruption; stretching U.S. naval assets across multiple theaters. |

| Kataib Hezbollah (PMF) | Kinetic / Proxy | U.S. forces in Iraq; diplomatic facilities in Kurdistan Region. 65 | Compelling U.S. withdrawal from Iraq; coercing GCC states to deny basing rights. |

| Handala Hack (MOIS) | Cyber / PsyOps | U.S. medical tech firms (Stryker); doxxing IDF personnel; Sanzer Hasidic community data theft. 68 | Psychological terror; degrading civilian morale; inciting domestic violence. |

| Cyber Islamic Resistance | Cyber / Sabotage | Drone defense systems; payment infrastructure; website defacements. 70 | Disrupting civil functionality; projecting Iranian technological reach. |

8.3. Homeland Security Implications

The prolongation of the Iran conflict presents severe and rapidly evolving threats to U.S. Homeland Security. The 2026 Annual Threat Assessment (ATA) issued by the Office of the Director of National Intelligence explicitly warns that while the U.S. geographic position and conventional military capability heavily insulate it from traditional foreign attacks, the complex, interconnected nature of the global security environment leaves the homeland highly vulnerable to asymmetric infiltration and terrorism.73

Following the assassination of Khamenei, the Department of Homeland Security significantly elevated threat advisories, anticipating retaliatory actions utilizing Iran’s sophisticated global proxy infrastructure.75 The intelligence community notes that Iran maintains a robust, proven capability for covert operations; over the past five years, 157 cases of Iranian foreign operations were recorded globally, with 27 targeting the United States directly, including the 2024 plot to assassinate President Trump by IRGC asset Farhad Shakeri.75 Iran’s operational methodology increasingly relies on criminal surrogates, such as drug traffickers and organized crime syndicates, to maintain plausible deniability while conducting assassinations and sabotage on Western soil.75

Furthermore, a highly concerning demographic shift has been observed regarding domestic radicalization. Intelligence reports flag that teenage extremists, systematically indoctrinated through social media ecosystems deliberately engineered to provide religious justification for violence, were responsible for a significant portion of U.S.-based plotting in recent years.76 The State Department has issued urgent Worldwide Cautions, advising American citizens overseas of acute risks, particularly in the Middle East, as U.S. diplomatic and commercial facilities face an elevated threat matrix from decentralized Iranian-aligned actors.15

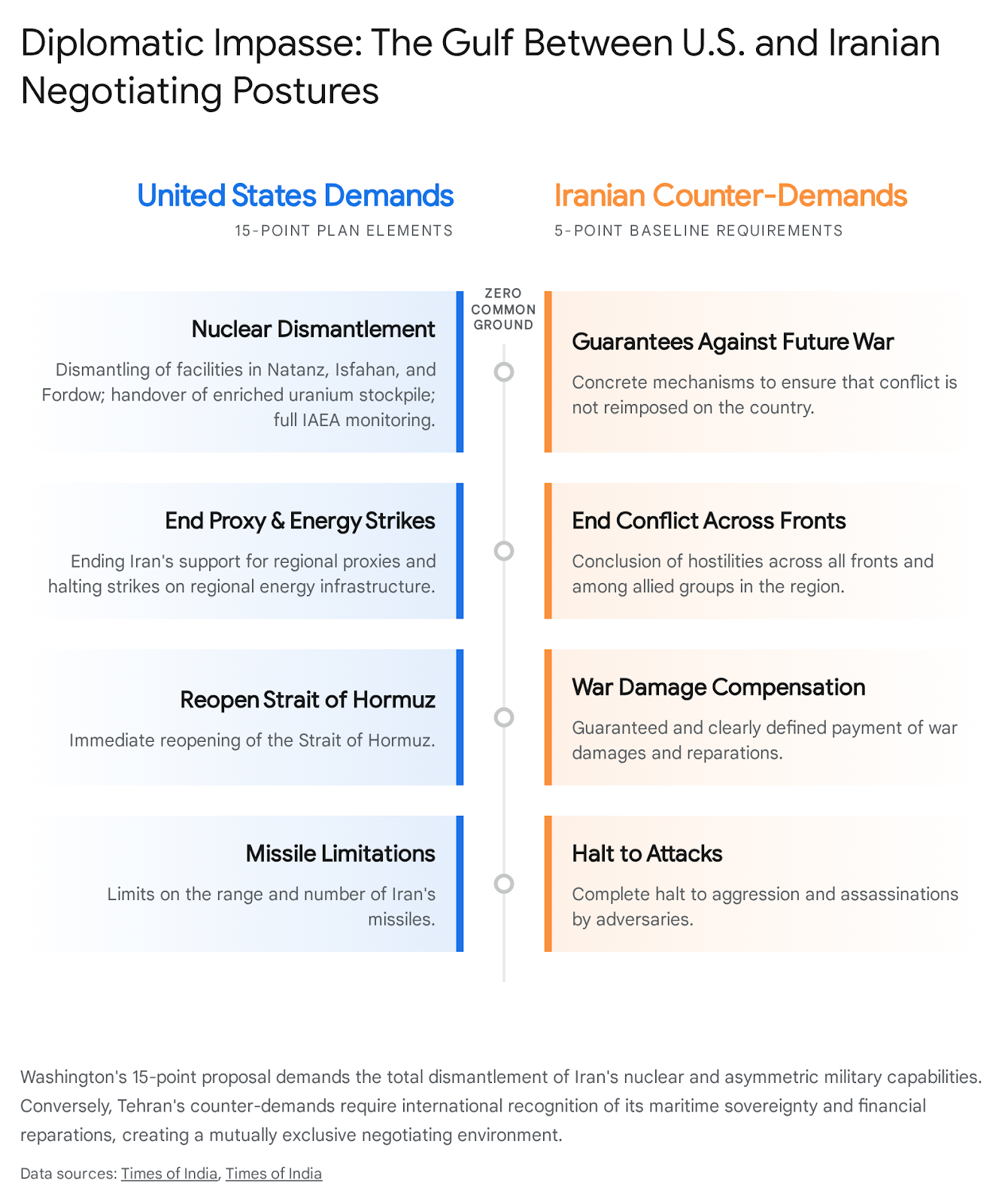

9. Diplomatic Paralysis: The U.S. 15-Point Plan and Iranian Resistance

Facing a rapidly deteriorating global economic landscape, plummeting domestic approval ratings, and mounting diplomatic isolation from traditional allies, the Trump administration initiated a frantic diplomatic push to establish an “offramp” to the conflict.77 Leveraging intermediaries in Pakistan and Oman—building upon the failed talks of 2025—the U.S. State Department, led by figures such as Special Envoy Steve Witkoff and Jared Kushner, delivered a comprehensive 15-point ceasefire and peace proposal to Tehran in mid-March.3

9.1. Structural Components of the 15-Point Proposal

The U.S. framework is highly ambitious, attempting to bundle total nuclear disarmament, regional security guarantees, and maritime freedom into a single, indivisible package.78 Based heavily on negotiation frameworks previously floated in May 2025, the core demands reflect maximalist U.S. strategic objectives that require near-total capitulation from Tehran.82 The plan demands an immediate 30-day ceasefire, the complete dismantling of nuclear facilities at Natanz, Isfahan, and Fordow, and a permanent commitment never to develop nuclear weapons, alongside handing over the entire stockpile of 60% enriched uranium to the IAEA.83 Furthermore, it demands the complete cessation of funding to regional proxies, limits on ballistic missiles, and the immediate reopening of the Strait of Hormuz.83 In exchange, the U.S. offers full sanctions relief, an end to the UN snapback mechanism, and civilian nuclear assistance at Bushehr.77

9.2. Iran’s 5-Point Counter-Demand

Unsurprisingly, Iranian officials view the proposal with deep skepticism, perceiving it as a reiteration of demands that violate Iranian sovereignty, particularly following the highly provocative assassination of their Supreme Leader.80 Through intermediaries, Iran categorically rejected the 15-point plan and countered with its own 5-point demand structure. Tehran requires a complete halt to U.S. and Israeli “aggression and assassinations,” concrete mechanisms to prevent future wars, guaranteed payment of war damages and reparations, the conclusion of hostilities across all proxy fronts, and crucially, international recognition of Iranian sovereignty over the Strait of Hormuz.3

| Key Domain | United States Demands (The 15-Point Plan) | Iranian Counter-Demands (The 5-Point Plan) |

| Hostilities | Immediate 30-day ceasefire to finalize the agreement. | Complete halt to U.S./Israeli “aggression and assassinations.” |

| Nuclear Infrastructure | Dismantle Natanz, Isfahan, and Fordow facilities; permanent commitment to no nuclear weapons. | Not explicitly addressed in the 5-point counter; historically rejected. |

| Uranium Stockpile | Hand over all 60% enriched uranium to the IAEA; no domestic enrichment allowed. | No concessions offered on enrichment or IAEA oversight. |

| Regional Proxies | End all funding, directing, and arming of proxy forces (Axis of Resistance). | Any agreement must include the conclusion of hostilities across all fronts/allies. |

| Maritime Security | Reopen the Strait of Hormuz as a free, unblocked maritime corridor. | International recognition of Iranian sovereignty over the Strait of Hormuz. |

| Missile Program | Limit range and quantity of ballistic missiles; restrict to self-defense only. | Establish concrete guarantees to prevent future wars against Iran. |

| Concessions / Relief | Full lifting of U.S./UN sanctions; remove “snapback” threat; aid for civilian nuclear power at Bushehr. | Guaranteed and clearly defined payment of war damages and reparations by the U.S. and Israel. |

9.3. The Failure of Backchannel Diplomacy and Public Messaging

The prospect of the 15-point plan succeeding remains exceptionally low. The targeted killings of key moderating figures, such as Ali Larijani—who possessed the diplomatic acumen to navigate complex backchannel negotiations with Europe and Moscow—have heavily empowered hardliners within the IRGC, fundamentally disincentivizing dialogue and ensuring a posture of deep defiance.6 The history of the U.S. breaching diplomatic good faith, notably breaking off the Oman talks in 2025 to launch the Twelve-Day War, has convinced Tehran that negotiations are merely a calculated ruse to pause conflict while the U.S. repositions military assets.4

From an information warfare perspective, the U.S. public diplomacy campaign surrounding the peace plan appears designed as much to sow internal paranoia within Iran’s fractured, hiding leadership as it is to secure an actual agreement. By publicly claiming that a “top person” in Tehran had reached out to Washington, President Trump aimed to generate mutual suspicion among surviving Iranian commanders regarding potential backchannel defections.86 However, this psychological warfare tactic, combined with domestic controversies regarding military commanders allegedly invoking “biblical end-times prophecies” to justify the war, has only further eroded the credibility of the U.S. diplomatic effort on the world stage.87

10. Strategic Conclusions

The 2026 Iran War, triggered by Operation Epic Fury, stands as a critical inflection point in 21st-century geopolitics. The United States successfully demonstrated its unparalleled conventional strike capabilities by degrading Iran’s nuclear infrastructure and decapitating its senior leadership. However, the strategic efficacy of military primacy has been entirely subverted by Iran’s highly effective asymmetric response. By closing the Strait of Hormuz and weaponizing the marine insurance industry, Iran transferred the immense costs of the conflict directly onto the populations of U.S. allies and the vulnerable nations of the Global South.

Consequently, the global perception of the United States has shifted dramatically. Rather than projecting strength and enforcing international order, Washington’s actions have inadvertently projected systemic instability, precipitating a catastrophic global economic shock characterized by energy shortages, manufacturing disruptions, and a burgeoning agricultural crisis. This geoeconomic blowback has severely fractured Western consensus, isolated the U.S. diplomatic corps, paralyzed multilateral institutions like BRICS+, and provided a generational opportunity for China and Russia to consolidate an alternative, anti-Western international architecture. Moving forward, the paramount strategic challenge for the United States is no longer simply managing the military threat posed by Tehran, but rather salvaging its credibility, soft power, and leadership role in a world that increasingly views American military unilateralism as a direct liability to global economic survival.

Please share the link on Facebook, Forums, with colleagues, etc. Your support is much appreciated and if you have any feedback, please email us in**@*********ps.com. If you’d like to request a report or order a reprint, please click here for the corresponding page to open in new tab.

Sources Used

- The Iran War and American Foreign Policy, accessed March 26, 2026, https://www.orfonline.org/expert-speak/the-iran-war-and-american-foreign-policy

- 2026 Iran War | Explained, United States, Israel, Strait of Hormuz, Map, & Conflict, accessed March 26, 2026, https://www.britannica.com/event/2026-Iran-War

- 2025–2026 Iran–United States negotiations – Wikipedia, accessed March 26, 2026, https://en.wikipedia.org/wiki/2025%E2%80%932026_Iran%E2%80%93United_States_negotiations

- How the Trump Administration’s Iran Strategy Backfired: A Breach of Diplomatic Trust, accessed March 26, 2026, https://www.jurist.org/commentary/2026/03/how-the-trump-administrations-iran-strategy-backfired-a-breach-of-diplomatic-trust/

- The Fault Lines Of A New Middle East: The 2025-2026 US-Israel-Iran War And The Reordering Of Regional Geopolitics – Analysis, accessed March 26, 2026, https://www.eurasiareview.com/23032026-the-fault-lines-of-a-new-middle-east-the-2025-2026-us-israel-iran-war-and-the-reordering-of-regional-geopolitics-analysis/

- Why Iran does not appear ready to give in, despite heavy losses, accessed March 26, 2026, https://www.washingtonpost.com/world/2026/03/22/iran-war-talks-trump-strikes-hormuz/

- After the strike: The danger of war in Iran – Brookings Institution, accessed March 26, 2026, https://www.brookings.edu/articles/after-the-strike-the-danger-of-war-in-iran/

- Iran’s Next Move: How to Counter Tehran’s Multidomain Punishment Campaign, accessed March 26, 2026, https://www.csis.org/analysis/irans-next-move-how-counter-tehrans-multidomain-punishment-campaign

- 2026 Strait of Hormuz crisis – Wikipedia, accessed March 26, 2026, https://en.wikipedia.org/wiki/2026_Strait_of_Hormuz_crisis

- The Insurance Weapon: How Commercial Risk Logic Became an Irregular Warfare Tool at Hormuz, accessed March 26, 2026, https://irregularwarfare.org/articles/insurance-weapon-irregular-warfare-hormuz/

- The Strait of Hormuz crisis will ripple across plastics and food supply …, accessed March 26, 2026, https://www.atlanticcouncil.org/blogs/energysource/the-strait-of-hormuz-crisis-will-ripple-across-plastics-and-food-supply-chains-helping-beijing-and-moscow-hurting-americans/

- Discover this week’s must-read finance stories, accessed March 26, 2026, https://www.weforum.org/stories/2026/03/energy-shock-shakes-markets/

- Hormuz is a trailer. Malacca is China’s real nightmare — and India knows it, accessed March 26, 2026, https://timesofindia.indiatimes.com/world/rest-of-world/hormuz-is-a-trailer-malacca-is-chinas-real-nightmare-and-india-knows-it/articleshow/129802348.cms

- The Iran war: Potential food security impacts | IFPRI, accessed March 26, 2026, https://www.ifpri.org/blog/the-iran-war-potential-food-security-impacts/

- US warns Americans worldwide to show ‘increased caution’ – as it happened, accessed March 26, 2026, https://www.theguardian.com/world/live/2026/mar/22/middle-east-crisis-live-iran-war-trump-ultimatum-major-attack-strait-of-hormuz-open-israel-hit-tehran-retaliation

- Chokepoint: How the War with Iran Threatens Global Food Security – CSIS, accessed March 26, 2026, https://www.csis.org/analysis/chokepoint-how-war-iran-threatens-global-food-security

- Rs 18 crore toll, Iran nod: Why crossing Strait of Hormuz is not so straight, accessed March 26, 2026, https://www.indiatoday.in/world/story/iran-war-strait-of-hormuz-countries-oil-ships-safe-passage-toll-losses-2886784-2026-03-25

- How Iran Blocking the Strait of Hormuz Affects the U.S., accessed March 26, 2026, https://www.factcheck.org/2026/03/how-iran-blocking-the-strait-of-hormuz-affects-the-u-s/

- Black Sea Shockwaves: Ukraine War Still Impacts Global South, accessed March 26, 2026, https://www.thecairoreview.com/essays/black-sea-shockwaves/

- US-Israel war on Iran may increase food prices worldwide: UN, accessed March 26, 2026, https://www.dawn.com/news/1985059

- Energy shock talk grabs headlines but the Iran war is also driving the world towards a food crisis | Heather Stewart, accessed March 26, 2026, https://www.theguardian.com/business/2026/mar/22/energy-shock-iran-war-also-driving-world-towards-food-crisis

- How the Iran war has sent shocks rippling across the globe, accessed March 26, 2026, https://www.theguardian.com/world/2026/mar/20/iran-war-shocks-across-globe-effects-key-takeaways

- UN Security Council Meets in Emergency Session on Crisis in the Middle East, accessed March 26, 2026, https://betterworldcampaign.org/peace-and-security/un-security-council-convenes-emergency-session-on-crisis-in-the-middle-east

- The Lonely Superpower: Trump’s Iran War and the End of American Consent, accessed March 26, 2026, https://moderndiplomacy.eu/2026/03/22/the-lonely-superpower-trumps-iran-war-and-the-end-of-american-consent/

- Energy Shock Forces Europe to Rethink Climate Ambitions – Modern Diplomacy, accessed March 26, 2026, https://moderndiplomacy.eu/2026/03/26/energy-shock-forces-europe-to-rethink-climate-ambitions/

- European leaders debate ETS while the energy crisis burns elsewhere, accessed March 26, 2026, https://www.epc.eu/publication/european-leaders-debate-ets-while-the-energy-crisis-burns-elsewhere/

- Governments Declare Emergency Energy Policies in Response to …, accessed March 26, 2026, https://www.cfr.org/articles/governments-declare-emergency-energy-policies-in-response-to-iran-war

- Ranked: The World’s Most Powerful Countries by Soft Power in 2026 – Visual Capitalist, accessed March 26, 2026, https://www.visualcapitalist.com/ranked-the-worlds-most-powerful-countries-by-soft-power-in-2026/

- Global Soft Power Index 2026 – Brandirectory, accessed March 26, 2026, https://static.brandirectory.com/reports/brand-finance-soft-power-index-2026-digital.pdf

- Poll 2025, accessed March 26, 2026, https://poll.lowyinstitute.org/files/lowyinsitutepoll-2025.pdf

- Most say the United States’ recent military actions against Iran have gone too far, accessed March 26, 2026, https://apnorc.org/projects/most-say-the-united-states-recent-military-actions-against-iran-have-gone-too-far/

- Poll shows most Americans feel war against Iran has gone too far, accessed March 26, 2026, https://www.pbs.org/newshour/nation/poll-shows-most-americans-feel-war-against-iran-has-gone-too-far

- Nearly all Americans say the conflict with Iran is raising gas prices, but few expect Trump to back down – YouGov, accessed March 26, 2026, https://yougov.com/en-us/articles/54392-nearly-all-americans-say-conflict-with-iran-is-raising-gas-prices-few-expect-donald-trump-to-back-down-march-20-23-2026-economist-yougov-poll

- More Voters Think War With Iran Will Make The World Less Safe, Quinnipiac University National Poll Finds; Healthcare Costs Top List Of Financial Concerns For Voters, accessed March 26, 2026, https://poll.qu.edu/poll-release?releaseid=3953

- Security Council Adopts Resolution 2817 (2026) Condemning Iran’s ‘Egregious Attacks’ against Neighbours as Middle East Violence Rapidly Escalates, accessed March 26, 2026, https://press.un.org/en/2026/sc16315.doc.htm

- UN experts denounce aggression on Iran and Lebanon, warn of devastating regional escalation | OHCHR, accessed March 26, 2026, https://www.ohchr.org/en/press-releases/2026/03/un-experts-denounce-aggression-iran-and-lebanon-warn-devastating-regional

- Iran War Unravels U.S. Strategy and Strengthens Russia China Axis, accessed March 26, 2026, https://toda.org/global-outlook/2026/iran-war-unravels-us-strategy-and-strengthens-russia-china-axis.html

- China-Iran Fact Sheet: A Short Primer on the Relationship, accessed March 26, 2026, https://www.uscc.gov/sites/default/files/2026-03/China-Iran_Fact_Sheet_A_Short_Primer_on_the_Relationship.pdf

- ‘Vicious Cycle’: China Issues Big Warning As Hormuz Crisis Deepens | US-Israel War On Iran, accessed March 26, 2026, https://timesofindia.indiatimes.com/videos/international/vicious-cycle-china-issues-big-warning-as-hormuz-crisis-deepens-us-israel-war-on-iran/videoshow/129752953.cms

- Russia, China urge diplomacy amid Gulf tensions, accessed March 26, 2026, https://dailytimes.com.pk/1467688/russia-china-urge-diplomacy-amid-gulf-tensions/

- Russia, China warn of Strait of Hormuz blockade and regional conflict risks, accessed March 26, 2026, https://www.jpost.com/international/article-890870

- Foreign Ministry Spokesperson Mao Ning’s Regular Press Conference on March 2, 2026_Ministry of Foreign Affairs of the People’s Republic of China, accessed March 26, 2026, https://www.fmprc.gov.cn/mfa_eng/xw/fyrbt/202603/t20260302_11867202.html

- Iran, China and Russia sign trilateral strategic pact – Middle East Monitor, accessed March 26, 2026, https://www.middleeastmonitor.com/20260129-iran-china-and-russia-sign-trilateral-strategic-pact/

- China is playing the long game over Iran | Chatham House – International Affairs Think Tank, accessed March 26, 2026, https://www.chathamhouse.org/2026/02/china-playing-long-game-over-iran

- China-Iran Fact Sheet: A Short Primer on the Relationship | U.S., accessed March 26, 2026, https://www.uscc.gov/research/china-iran-fact-sheet-short-primer-relationship

- US-Israel-Iran war: Congress presses Centre to use its leverage as BRICS+ chair, accessed March 26, 2026, https://www.nationalheraldindia.com/national/us-israel-iran-war-congress-presses-centre-to-fast-track-brics-summit

- Iran war shows limits of Brics as India pushed to choose sides – The Business Times, accessed March 26, 2026, https://www.businesstimes.com.sg/international/iran-war-shows-limits-brics-india-pushed-choose-sides

- A house divided — BRICS members at odds over Iran war – Daily Maverick, accessed March 26, 2026, https://www.dailymaverick.co.za/article/2026-03-11-a-house-divided-brics-members-at-odds-over-iran-war/

- From Hormuz to South Asia: The Energy Crisis Unfolding at Home, accessed March 26, 2026, https://moderndiplomacy.eu/2026/03/26/from-hormuz-to-south-asia-the-energy-crisis-unfolding-at-home/

- India taps 41 nations for energy amid Hormuz tensions, PM Modi says – Gulf News, accessed March 26, 2026, https://gulfnews.com/world/asia/india/india-taps-41-nations-for-energy-amid-hormuz-tensions-1.500483489

- Disruptions in Strait of Hormuz ‘unacceptable’: India’s Modi – Anadolu Ajansı, accessed March 26, 2026, https://www.aa.com.tr/en/asia-pacific/disruptions-in-strait-of-hormuz-unacceptable-india-s-modi/3875809

- India among ‘friendly nations’ listed by Iran for big Strait of Hormuz reprieve | India News, accessed March 26, 2026, https://www.hindustantimes.com/india-news/india-among-friendly-nations-listed-by-iran-for-big-strait-of-hormuz-reprieve-101774492480438.html

- South Korean ships can go through Strait of Hormuz after coordination with Iran, envoy tells Seoul, accessed March 26, 2026, https://www.aa.com.tr/en/energy/general/south-korean-ships-can-go-through-strait-of-hormuz-after-coordination-with-iran-envoy-tells-seoul/55866

- Africa in Iran’s Broader Geopolitical Strategy, accessed March 26, 2026, https://hornreview.org/2026/03/23/africa-in-irans-broader-geopolitical-strategy/

- DeBriefed 9 January 2026: US to exit global climate treaty; Venezuelan oil ‘uncertainty’; ‘Hardest truth’ for Africa’s energy transition – Carbon Brief, accessed March 26, 2026, https://www.carbonbrief.org/debriefed-9-january-2026-us-to-exit-global-climate-treaty-venezuelan-oil-uncertainty-hardest-truth-for-africas-energy-transition/

- Asia braces for worst-case energy scenarios as Iran war drags on, accessed March 26, 2026, https://www.japantimes.co.jp/news/2026/03/26/asia-pacific/asia-energy-scenarios-iran-war/

- Asia scrambles to confront energy crisis unleashed by Iran war – with no end in sight, accessed March 26, 2026, https://www.theguardian.com/world/2026/mar/12/asia-energy-crisis-iran-war

- South Korea launches emergency economic teams amid Middle East crisis, accessed March 26, 2026, https://www.aa.com.tr/en/asia-pacific/south-korea-launches-emergency-economic-teams-amid-middle-east-crisis/3878077

- South Korea Enters Emergency Mode as Energy Crisis Intensifies, accessed March 26, 2026, https://impakter.com/south-korea-enters-emergency-mode-as-middle-east-crisis-bites/

- What Are the Implications of the Iran Conflict for Japan? – CSIS, accessed March 26, 2026, https://www.csis.org/analysis/what-are-implications-iran-conflict-japan

- Asia Set to Pledge $30 Billion in Energy, Mineral Deals With US, accessed March 26, 2026, https://www.energyconnects.com/news/gas-lng/2026/march/asia-set-to-pledge-30-billion-in-energy-mineral-deals-with-us/

- US and Japan Organize Indo-Pacific Forum To Alleviate Energy Crisis, accessed March 26, 2026, https://bowergroupasia.com/us-and-japan-organize-indo-pacific-forum-to-alleviate-energy-crisis/

- Behind China’s Measured Response to the Middle East Conflict, accessed March 26, 2026, https://globalaffairs.org/commentary/analysis/behind-chinas-measured-response-middle-east-conflict

- Middle East Special Issue: March 2026 – ACLED, accessed March 26, 2026, https://acleddata.com/update/middle-east-special-issue-march-2026

- Iran Update Evening Special Report, March 2, 2026 | ISW, accessed March 26, 2026, https://understandingwar.org/research/middle-east/iran-update-evening-special-report-march-2-2026/

- We Bombed the Wrong Target Iran’s Proxy Network Strategy – Irregular Warfare Initiative, accessed March 26, 2026, https://irregularwarfare.org/articles/iran-proxy-network-strategy/

- G7 statement on support to partners in the Middle East. (21.03.26) – France Diplomatie, accessed March 26, 2026, https://www.diplomatie.gouv.fr/en/country-files/iran/news/article/g7-statement-on-support-to-partners-in-the-middle-east-21-03-26

- Justice Department Disrupts Iranian Cyber Enabled Psychological Operations, accessed March 26, 2026, https://www.justice.gov/opa/pr/justice-department-disrupts-iranian-cyber-enabled-psychological-operations

- Resecurity warns that Iran war enters multi-domain phase as cyber and kinetic operations converge, accessed March 26, 2026, https://industrialcyber.co/critical-infrastructure/resecurity-warns-that-iran-war-enters-multi-domain-phase-as-cyber-and-kinetic-operations-converge/

- Threat Brief: March 2026 Escalation of Cyber Risk Related to Iran, accessed March 26, 2026, https://unit42.paloaltonetworks.com/iranian-cyberattacks-2026/

- Cyber impact of conflict in the Middle East, and other cybersecurity news, accessed March 26, 2026, https://www.weforum.org/stories/2026/03/cyber-impact-conflict-middle-east-other-cybersecurity-news-march-2026/

- Iran’s Strategic Communications in the Campaign: Intimidation, Deterrence, and Resilience, accessed March 26, 2026, https://www.inss.org.il/publication/roaring-lion-media/

- 2026 Annual Threat Assessment of the U.S. Intelligence Community – ODNI, accessed March 26, 2026, https://www.dni.gov/files/ODNI/documents/assessments/ATA-2026-Unclassified-Report.pdf

- DNI Gabbard Releases 2026 Annual Threat Assessment of the U.S. Intelligence Community, accessed March 26, 2026, https://www.dni.gov/index.php/newsroom/press-releases/press-releases-2026/4142-pr-03-26

- How the Iran Conflict Could Drive a New Wave of Terrorism in the West, accessed March 26, 2026, https://www.visionofhumanity.org/how-the-iran-conflict-could-drive-a-new-wave-of-terrorism-in-the-west/

- 16,000 missiles, a vengeful Iran, and an AI race America cannot afford to lose: 2026 threat assessment, explained, accessed March 26, 2026, https://timesofindia.indiatimes.com/world/us/16000-missiles-a-vengeful-iran-and-an-ai-race-america-cannot-afford-to-lose-2026-threat-assessment-explained/articleshow/129670507.cms

- ‘They cannot have a nuclear weapon’: US pushes 15-point plan to end Iran war, sent via Pakistan, accessed March 26, 2026, https://timesofindia.indiatimes.com/world/us/they-cannot-have-a-nuclear-weapon-us-pushes-15-point-plan-to-end-iran-war-sent-via-pakistan/articleshow/129789762.cms

- Trump’s peace plan, Iran’s counter: What’s the endgame? Where things stand in Week 4 of Middle East war, accessed March 26, 2026, https://timesofindia.indiatimes.com/world/middle-east/trumps-peace-plan-irans-counter-whats-the-endgame-where-things-stand-in-week-4-of-middle-east-war/articleshow/129792894.cms

- US sent Iran 15-point plan aimed at ending the Middle East war – Al Arabiya, accessed March 26, 2026, https://english.alarabiya.net/News/united-states/2026/03/25/us-has-sent-iran-a-15point-plan-to-end-the-war-in-the-middle-east-report

- US 15-point plan reaches Tehran as Iran publicly scoffs at diplomacy, accessed March 26, 2026, https://www.iranintl.com/en/202603254350

- U.S. sent Iran 15-point plan aimed at month-long ceasefire: Israeli media – Xinhua, accessed March 26, 2026, https://english.news.cn/20260325/0383eb08ad97467d9017170c5973a7db/c.html

- Trump’s rehashed 15-point Iran plan unlikely to appease Tehran, accessed March 26, 2026, https://www.theguardian.com/world/2026/mar/24/trumps-rehashed-15-point-iran-plan-unlikely-to-appease-tehran

- What’s inside Trump’s 15-point plan to end war with Iran?, accessed March 26, 2026, https://timesofindia.indiatimes.com/world/us/whats-inside-trumps-15-point-plan-to-end-war-with-iran/articleshow/129802951.cms

- US sends 15-point plan to Iran: Nuclear rollback, Hormuz access on table; what else is at stake, accessed March 26, 2026, https://www.businesstoday.in/world/story/us-sends-15-point-plan-to-iran-nuclear-rollback-hormuz-access-on-table-what-else-is-at-stake-522188-2026-03-25

- ‘Trump will not dictate end of war’: Iran dismisses US’ 15-point de-escalation proposal, counters with its own 5 demands, accessed March 26, 2026, https://timesofindia.indiatimes.com/world/middle-east/trump-will-not-dictate-end-of-war-iran-rejects-us-15-point-plan-counters-with-its-own-5-demands/articleshow/129804889.cms

- Weaponizing ambiguity: how US shadow diplomacy may be fracturing Iran regime, accessed March 26, 2026, https://www.iranintl.com/en/202603234812

- Brownley and Colleagues Request Investigation into Alleged Reports that Military Leaders Claim War in Iran Part of Biblical End-Times Prophecies, accessed March 26, 2026, https://juliabrownley.house.gov/brownley-and-colleagues-request-investigation-into-alleged-reports-that-military-leaders-claim-war-in-iran-part-of-biblical-end-times-prophecies/